Russia key rate preview: long-term guidance matters

- 31 January 2020

- Russia

We believe the Russian key rate will remain unchanged on 7 February, as the central bank will take time to consider implications of upcoming fiscal easing and the Coronavirus outbreak. The key focus, as usual, is longer-term guidance, which should contain a response to claims that Russian rates are “too high”

Now is probably not the best time to cut the rate

The market seems divided on the expected outcome of the 7 February monetary policy meeting, with around half of analysts (and perhaps a bigger portion of traders) expecting a cut, mainly citing the current slowdown of the CPI rate in Russia, which according to preliminary weekly data dropped to 2.5% year on year as of 27 January. We agree that the Russian key rate has scope for reduction and indeed, Russian CPI is likely to see rapid a deceleration from 3.0% YoY in December 2019 to 2.4% YoY in January 2020. However, this is unlikely to be a strong argument in favour of a cut in the key rate, which we see staying at 6.25% on Friday. We see the following arguments in favour of the wait-and-see approach at the upcoming monetary policy meeting:

- Current slowdown in CPI stems from the high base effect created by the VAT rate hike, which took place at the beginning of last year. Following a forecast drop to 2.0-2.5% YoY in 1Q20, CPI should return to 3.5-4.0% YoY by year-end 2020.

- CPI composition suggests that food seems to be the sole disinflationary component, reacting to non-monetary factors – and the recent recovery in global agriculture product prices is now a risk factor. January CPI composition will be released on 6 February, just one day ahead of the monetary policy meeting.

- Consumer sentiment index in January 2019 was reported at 95 points, 9 points higher than a year ago, suggesting a lack of demand-driven constraints to CPI growth.

- Recent government reshuffle and new social policy measures with an estimated budget expenditure of 0.5-1.0% of GDP per annum creates potential for an acceleration of consumption and overall GDP growth above the potential 1.0-1.5% rate, which may create additional inflationary risks. On the positive side, Finance Minister Siluanov, despite his formal demotion from the first deputy PM status, will still report directly to the prime minister, which lowers the likelihood of material easing in fiscal policy. Still, the updated budget draft, which would shed light on the actual scale of easing, is expected to be released by 11 February.

- Coronavirus outbreak in China has negatively affected global markets, contributing to 3% RUB depreciation year-to-date. ING analysts do not exclude further pressure of the epidemic story on the Chinese GDP, CNY, oil&metals prices, as well as EM/commodity currencies – reinforcing our cautious take on RUB, which was initially based on local fundamental factors.

- The invesment community may require some reassurance in the central bank's independence following the appointment of Andrei Belousov as first deputy PM responsible for the financial and economic block of the government. In September 2018, at the time of significant market turbulence, Mr Belousov, who was holding the position of top economic aide to the president, publically warned Bank of Russia that an increase in the key rate would be 'highly undesirable'. The central bank made the hike anyway, sending a strong message of independence. This time, a cut in the key rate following a cautious guidance from the previous meeting and at times of market turmoil, could potentially lead to questions whether it is justified by economic reality or is a sign of a shift in the central bank's priorities.

Long-term guidance matters: CBR's 2-3% real rate approach is becoming an uphill struggle

Regardless of whether the Central Bank of Russia will cut the rate on 7 February or not, which can really go either way, the key question relevant for the markets is the scope for further cuts after all the dust related to the government reshuffle and Coronavirus is settled. The public discussion on the adequacy of the Russian rates has been ongoing for a while now, and the views on the central bank's approach have been polarized. While most market economists (ourselves included) praised the central bank for being prudent and for pushing the government to boost growth thorough structural/institutional measures, a number of state officials and representatives of the business community criticized it for keeping the rates inadequately high for scholastic reasons.

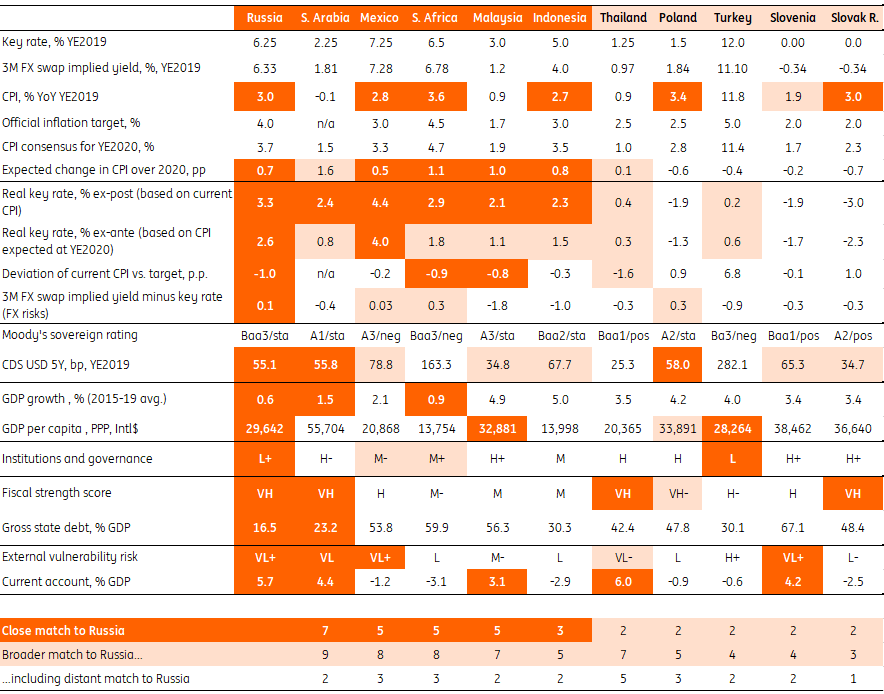

Looking at this matter from a cross-country perspective (Figure 1 below, all data is as of year-end 2019), we have the following observations:

- Russia is not unique in having a high positive real rate, as it belongs to a group of countries (Saudi Arabia, Mexico, Malaysia, South Africa, Indonesia) which have a) CPI higher than in developed markets; b) volatile CPI trajectory and expectations of higher CPI in 12 months (unlike in DM and CEE), which somewhat lowers the importance of current CPI being below the official target; c) uncertainties regarding the FX rate on various (mostly foreign/domestic policy-related) country-specific risks; d) relatively weak institutions and governance, which partially contribute to mid to lower-middle income country group membership, weak economic growth trend, as well as generally higher CPI and FX risk perception relative to DM; and e) low amount of debt to service, meaning the ability to afford high interest rates from the perspective of state debt management.

- Russia’s rates tend to be one the highest among peers: a) Russia’s ex-post (based on current CPI) real key rate of 3.3% is the second highest among peers after Mexico, which is running bigger foreign and domestic policy risks and has a much weaker current account and therefore requires a highly positive real rate to support FX; b) Russia’s ex-ante (based on CPI expected in 12 months) real key rate of 2.6% is significantly higher than that of peers (other than Mexico), which is in the range of 0.8-1.6%; and c) Russian GDP growth trend is weaker than that of most of its closest peers while having the lowest FX risks (and little interest in significantly stronger FX)

Based on this peer comparison, Russia's nominal key rate has some downside potential, at least the 25 bp cut we expect to take place at some point in 2020, and potentially some further cuts would not be unjustified, however much will depend on the trajectory of CPI expectations. So far Russia has been running a long cycle of below-expected CPI prints, though that has been a result of favourable agriculture price environment and fiscal tightening. The prospects of the former are unclear, while the unwinding of fiscal policy is evident. By now the Russian budget has accumulated a backlog of spending in the amount of 1.0% of GDP, which is likely to be used to finance new social policy commitments of around 0.3-0.5% of GDP. In addition to direct spending some additional investments from the fiscal savings fund of around 0.3% of GDP may follow. In view of this, we see little chance the CBR will easily abandon its 4% CPI target and 2-3% real key rate approach soon, however the market discussion will definitely continue.

We see the following watch factors that may affect the big debate on rates and will probably find their way into the central bank communication:

- Budget policy approach: so far at least a moderate easing appears likely, updated budget draft is expected in the next few days

- Current CPI trajectory: slowdown in 1Q20 is inevitable on the high base effect (1Q19 saw reaction to VAT hike), but composition will matter – if it’s just food, then there will be evidence of a strong reversal in CPI after 1Q20

- CPI expectations, which are volatile: there was a deterioration in corporate and households’ CPI expectations in December 2019, followed by a subsiding in January. Meanwhile, if the Coronavirus outbreak hampers the delivery of affordable consumer products from China (AliExpress etc), lower competition on the local market combined with social support measures by the government may add to inflationary risks

- FX fundamentals: 2019 balance of payments has pointed at a strong acceleration of imports; households’ and corporate appetite for FX assets accumulation remains unclear, while the scope for further active portfolio inflows into OFZ after rallying 2019 is also unclear.

Figure 1. Russia is not unique in having high rates, but how high is too high?

Overall, we believe the Russian key rate has scope for reduction but the upcoming meeting is probably not the best time to cut, as the CPI picture is distorted by the high base effect, the recent government reshuffle means fiscal easing, the scale of which is yet to be determined, markets have been hit by Coronavirus, and investors may need reassurance that the pro-growth shift in the Cabinet does not affect the central bank’s inflation targeting priorities. The upcoming release of CPI composition for January, updated budget draft, and newsflow on the Coronavirus outbreak could be the key near-term watch factors, which may affect both the key rate decision and the medium-term guidance.

Regardless of whether the CBR will cut the rate on 7 February or not, the key question is the scope for further cuts after all the dust related to government reshuffle and coronavirus is settled. Based on a peer comparison, Russia is not unique in having high positive real rates, however at this point it seems a bit too high relative to the level of risks it is running. As a result, we are expecting the CBR to somehow address the market debate on the sustainability of the current monatary policy stance in the longer term, and believe the nominal key rate has some downside potential, at least the 25 bp cut we expect to take place at some point in 2020. The likelihood of further cuts is not nil, however much will depend on the trajectory of CPI expectations. So far Russia has been running a long cycle of below-expected CPI prints, though that has been a result of favourable agriculture price environment and fiscal tightening. The prospects of the former are unclear, while the unwinding of fiscal policy is evident.

In view of this, we see little chance the CBR will easily abandon its 4% CPI target and 2-3% real key rate approach soon, however the market discussion will definitely continue.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more