Rates – turning Japanese, I really think so

- 30 January

- Rates

We don't often spotlight Asia here, but this month we're all about Japan. What's happening there has important echoes for core markets in the West. The dominant impulse is upward pressure on market rates (dramatic in Japan of late), but at the same time, an ongoing evolution toward normal rates (and curves). This remains a thing in both the eurozone and the US

Pressure for higher rates in Japan is an important relative value driver

There has been quite a theme of consternation in Japan of late. It has crescendoed over the past week amid talk of imminent Bank of Japan intervention to secure a turnaround for the super-weak Japanese yen (JPY). The backstory here involves maintaining exceptionally low official rates. Last week, the Bank of Japan (BoJ) left the official rate unchanged at 0.75%. In prior weeks, though, the 30yr JGB yield almost touched 4%. The markets have clearly decided that the BoJ is lagging in its rate-hike game, and the weakness of JPY tells a similar story (a recent note here shows how this presents an opportunity).

The wider core rates environment is sitting up and paying attention to all of this – and for good reason. First, what's happening in Japan represents a clear swing from the prior zero-rate environment to a more normal rates environment. We noted almost a year ago that rate pressure to the upside was a thing (it's here). We also held out 2% as a viable neutral rate for the BoJ to aim for, eventually. The 10yr JGB yield shot above that level in the past few weeks, and remains on a medium-term journey higher. And why not? Japanese inflation is currently in the 2.5-3% territory.

Apart from the move away from deflation, there have been a few important landmarks along the way that point to upward pressure on Japanese rates. First, inflation has become a thing in most core markets, including the eurozone (the ECB is already at its neutral rate of 2%). Second, the BoJ ended its policy of yield curve control in March 2024 (although the market reaction was initially muted by ongoing BoJ support buying). Third, wide rate differentials with other core centres were clearly proving detrimental to the JPY, suggesting the differentials were too high (Japanese rates too low).

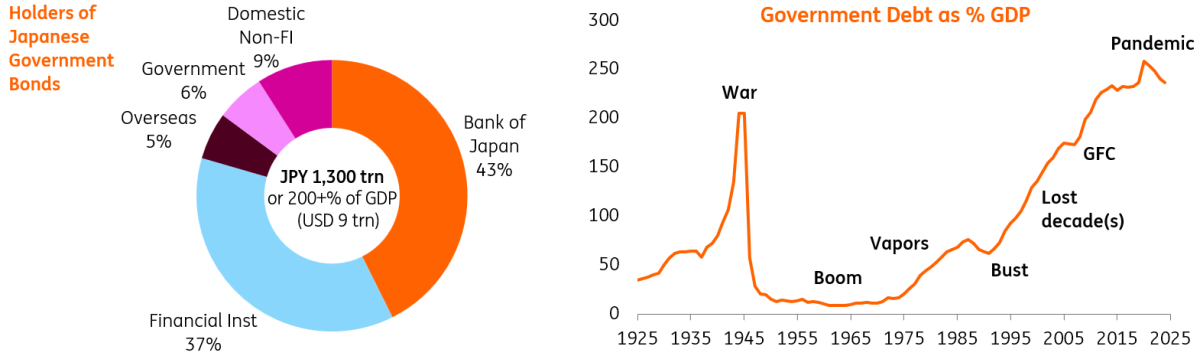

And, while not front and centre as an immediate issue, we can't ignore the inconvenient truth of Japan's mammoth debt/GDP ratio. While about half of Japanese Government Bonds (JGBs) are held by the official sector, and foreign ownership is low, there is still a massive debt obligation outstanding. This means two key outcomes. First, the classic low-rate funding currency of recent decades may still be with us, but now at much higher and rising funding rates. Second, this impacts US and eurozone rates from a relative-value perspective, pressuring them higher from below.

Holders of JGBs and the build of debt

Latest data for September 2025

As normal as you like in the eurozone and the US

Our rates outlook for 2026 (here) centres on a theme of chaos, but also one of normality for rates. The noise out of Japan pushes in the same direction, as we see the BoJ eventually getting to 2% (perhaps not in the current cycle). In the eurozone, the ECB is already at its neutral deposit rate of 2%. And the 10yr Euribor rate is close to the 3% area, with an almost 100bp curve.

In the US, the Federal Reserve has a 3% handle on its funds rate, and the market discount has it ending in the 3-3.5% range. Again, a picture of neutrality. The same holds for the 10yr Treasury yield at or about 4.2% – also not too deviant from neutral versus long-run averages.

Our twist on this is the identification of an upward bias to longer tenor rates, both in the US and eurozone (and Japan), with inflation and fiscal circumstances as drivers (explained more fully in the aforementioned rates outlook for 2026).

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Europe’s Arnold moment – why strategy over spectacle matters

- This bundle contains 15 Articles