- Opinion by Padhraic Garvey, CFA

Japan and South Korea: Big moves, big opportunity

- 16 January

- Rates

Here we arbitrage the recent and projected movements for Japanese and South Korean rates relative to US rates in a cross-currency framework. We find that prior convergence of rates, together with divergence in the respective Asian currencies versus their forwards against the US dollar, presents an opportunity

We see Japan and Korea as the inverse to China on rates arbitrage

Last week, we published an analysis comparing Chinese and US rates, noting that current interest‑rate differentials tend to favour China relative to the US. It’s here. When we look at Japan and South Korea, however, the rate environment and currency backdrop are quite different, leading to a contrast with the China-US comparison.

Min Joo, our Seoul-based economist, sets the scene for both. It's here for Japan, and here for South Korea. On South Korea, the key inputs are an on-hold Bank of Korea (BoK) and KRW weakness (perhaps to 1500 vs USD), ultimately giving way to KRW strength (to 1450 vs USD). And for Japan, key inputs include the Bank of Japan (BoJ) on hold for the first half of 2026 before resuming hikes in the second half, ongoing upward pressure on Japanese market rates, and on USD/JPY, where the 150 area is the next big target to the downside for 2026 (and 145 by the end of 2027). See more on that here; our FX strategist's hot-off-the-press FX Talking publication.

We strategise these views, together with an overlay of some notable moves in both markets over the past few weeks. Bottom line: there is a case for short tenor negative carry plays, or taking profit on existing positive carry holdings. Let's take them one at a time.

Note that "positive carry" is where we receive the higher rate and pay the lower rate, and negative carry is the opposite.

For Japan, dominating factors remain JPY weakness and rates convergence

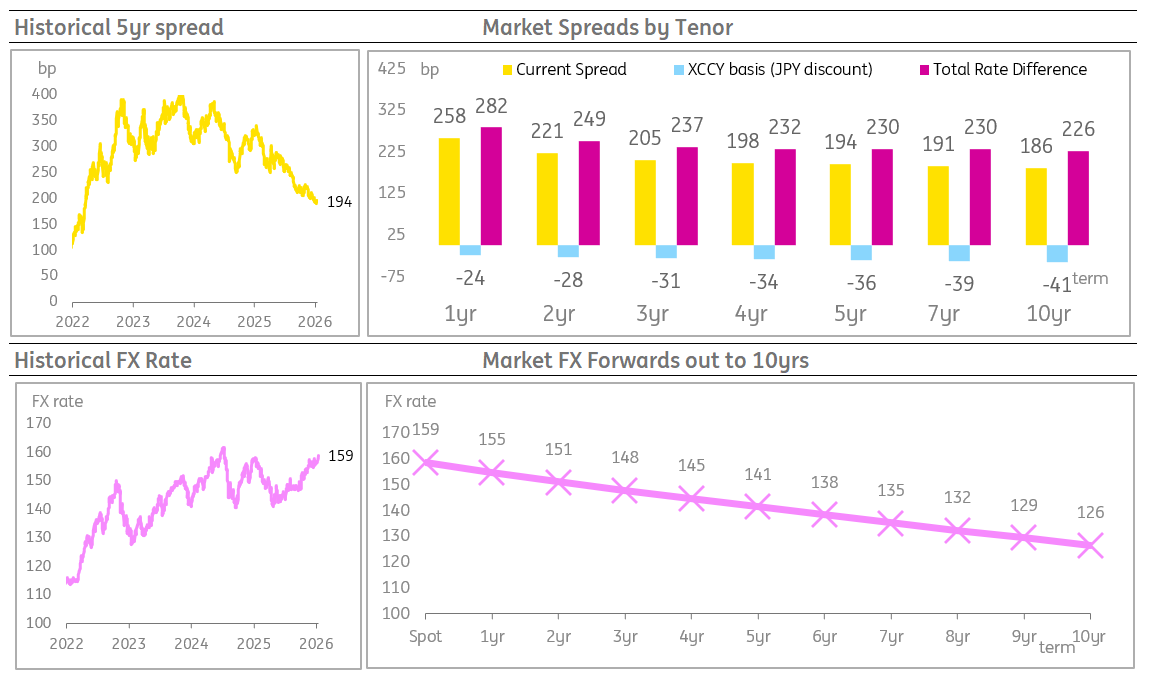

A glance at the chart below shows two big moves. First, a convergence process for spreads. Spreads are still wide, e.g. the 5yr spread is at 194bp, but that's practically half what it was (upper charts). Second, there has been quite a dramatic weakness in the Japanese yen (lower charts). In addition, the cross-currency basis discount on the JPY (which acts to stretch the all-in spread) is well below prior extremes.

All of these generate a positive mark-to-market for existing positive carry positions; certainly the ones set nine months ago, but generally in the past two or three years, especially if set with USD/JPY FX rate at below 150. Why? Because the positive carry play is long the all-in spread (benefits if it tightens), and long USD/JPY (benefits if JPY weakens).

Rate spreads from JPY into SOFR

Charts below show the USD/JPY FX profile

Given all of that, there is logic to setting an offsetting negative carry play. That could either knock out an existing positive carry play. Or it could be set outright with a view to benefiting from a very cheap entry point for the JPY, as the negative carry play benefits from JPY appreciation. We think USD/JPY can get back to 150 (and very likely lower). That's a greater JPY appreciation than discounted in the forwards out to 2yrs.

If not quite convinced, look at a weakening to 160 for USD/JPY as a trigger point, a level that our FX strategists identify as a likely entry point for Bank of Japan intervention (to strengthen JPY).

For players preferring to look to set a positive carry play, then we'd suggest a bias towards longer tenors. In the 10yr, for example, the all-in spread is 226bp. And the breakeven FX rate is 126.

So, provided USD/JPY does not appreciate to this level, the spread lock-in dominates, and the play generates all-in positive alpha. We'd view that as a positive reward versus risk. The trade also benefits as Japanese longer-tenor market rates rise (as it tightens the spread to SOFR rates).

Moreover, should USD/JPY just hold at about here in the long term (say over 5-10 years), then the positive carry is picked up without any FX movement cost.

For South Korea, the Scott Bessent angle on USD/KRW cannot be ignored

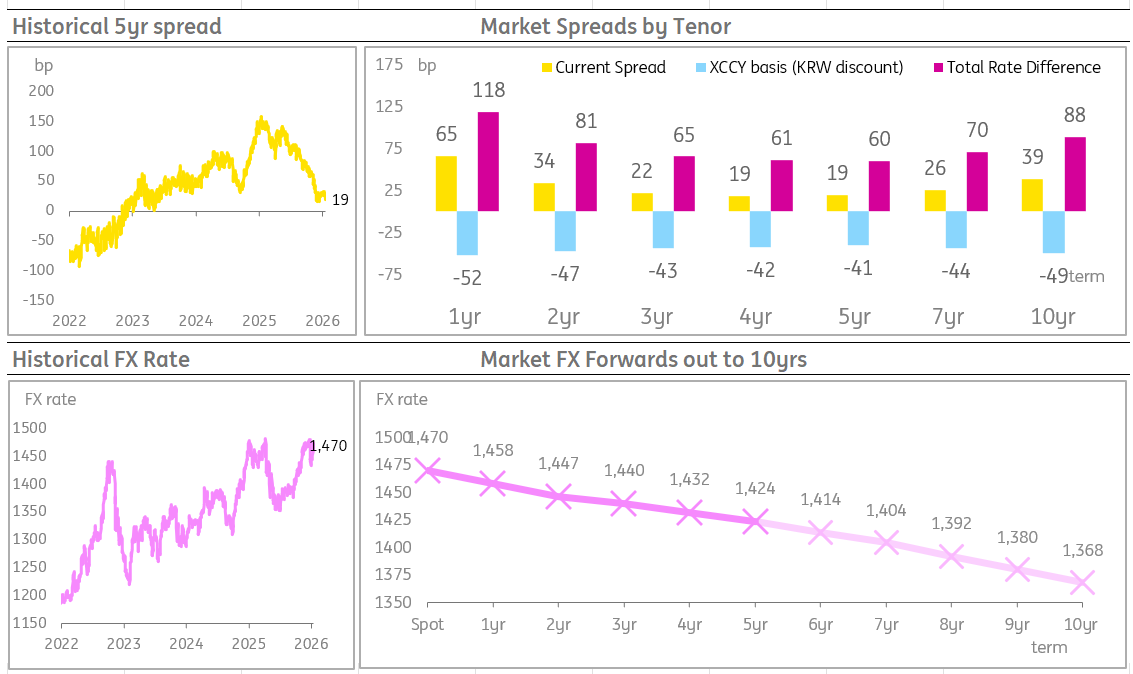

It's more nuanced, but we have a similar view of South Korea. The rearview mirror shows that long-positive carry plays (receive SOFR on the US leg) set in the summer of 2025 are in the money, as there has been a material tightening in spreads (including a tighter basis), and a marked depreciation in the KRW vs USD.

It's similar for the same plays set through most of 2024 – they are also in the money, but more on the weakening of the KRW than on spread movements (charts below).

Rate spreads from KRW into SOFR

Charts below show the USD/KRW FX profile

Just because there has been a positive mark-to-market does not mean we are primed for a reversal. But here's where the US Treasury Secretary comes in, where sometimes a prod can be enough for a change in tack. The KRW has been resisting the pull of the forward FX rate profile, mostly on dominant KRW outflows. But as noted above, we think that USD/KRW can ultimately turn and trend back down to the 1450 area.

True, before that, we have a call for attack on 1500. Fading that move would be a great area from which to set the negative carry play, or take profit on existing positive carry plays that are comfortably in profit. This is a short tenor play, preferably a 1yr play, or longest for 2 years.

For longer tenors, we're still quite enamoured with the positive carry play. For two reasons. First it picks up the still generous negative basis attached to the KRW leg. And second, the forward FX breakeven profile is very tolerable, for example, with our estimated 10yr forward rate implied at 1368 for USD/KRW. That would be quite the rally in the KRW, and the positive carry play works best if it is not realised. We like this from a risk/reward perspective.

Finally, for a fuller explanation of how we arbitrage in the cross-currency environment, please see the second half of the aforementioned piece on China versus the US – it's here.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more