Rates Spark: Watch inflation expectations drift higher

- 29 May

- Rates

Softer US data eases rate pressure, but inflation risks persist. Because even with a deal in sight, oil prices are unlikely to fall much more. Meanwhile, we see that euro inflation swaps are rising over time, more than the correlation with oil would imply. But with the ECB stressing downside growth risks, we don't see an aggressive hiking cycle as likely

Softer US macro data should increasingly see more attention

Even though the focus remains on oil for now, softer US macro data can also alleviate some of the upward pressure on US rates. The core PCE deflator came in lower than expected on Thursday, while first-quarter GDP growth was revised downwards. But this doesn’t change the broader picture of inflation continuing to rise as the price shock permeates through the economy, and second-round price pressures remain a considerable risk. And even if a final deal were to be struck, we don’t think oil prices will have much room to ease lower in the near term after the latest drop.

For US rates to make a material stretch lower, we should see a more dovish pivot from the Fed, something that could already materialise later this year. Yesterday’s weak disposable income figures highlighted the deteriorating outlook for US consumers, which should become more of a drag going forward. For now, markets are more focused on the positive news stories. However, a potential deal between the US and Iran is in sight, while US equities are consistently hitting new highs.

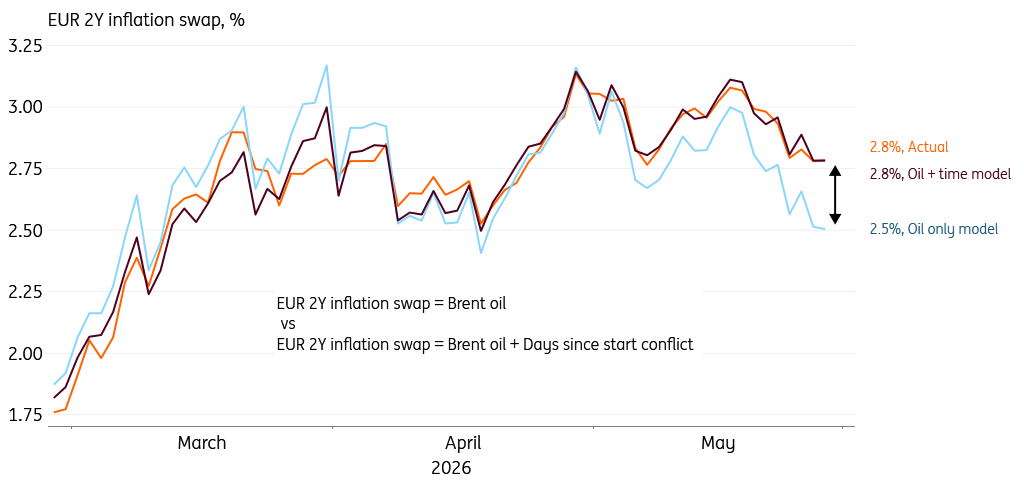

All else equal, euro inflation swaps are drifting higher

We’ve started to notice that euro inflation swaps are slowly drifting higher over time, even when accounting for oil price moves. At first sight, the linear correlation between oil prices and inflation swaps seems to hold firmly since the start of the conflict. But a model with just oil as the independent variable fails to capture the still elevated levels of inflation swaps of late, even as oil prices have come down again. The fit improves significantly when we add a time dimension to the regression. For every day since the start of the conflict, the 2Y inflation swap has been drifting higher by around 1bp. (For robustness, we also tested this setup using differenced data and got similar results.)

Our model suggests that two-year inflation expectations can increase by 30bp for every month the conflict lingers, even if oil prices stay at current levels. This means rates can drift higher, too. But also for Europe, growth dynamics will be important to watch. As the ECB highlighted in its April minutes, risks to the growth outlook are to the downside and have intensified since March. We therefore don’t think the ECB will fight this supply shock at the cost of worsening an economic downturn.

A simple model suggests a c.1bp increase in 2Y EUR inflation swaps for every day the conflict lingers

Friday’s events and market view.

The focus will likely remain on updates about a potential deal between the US and Iran. In terms of data, we have French, Spanish, German and Italian inflation figures, which will all be closely watched for the pass-through of higher oil prices. We also have a number of central bank speakers lined up, including Bank of England Governor Andrew Bailey and the ECB's Madis Muller.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more