Rates Spark: How a Ukraine peace deal could lower rates

- 25 November 2025

- Rates Spark

Intuitively, a deal with Russia would help euro rates higher, but falling gas futures are already pushing down the curve through lower inflation expectations. Tensions with Russia are likely to stay, which means risk sentiment should remain fragile

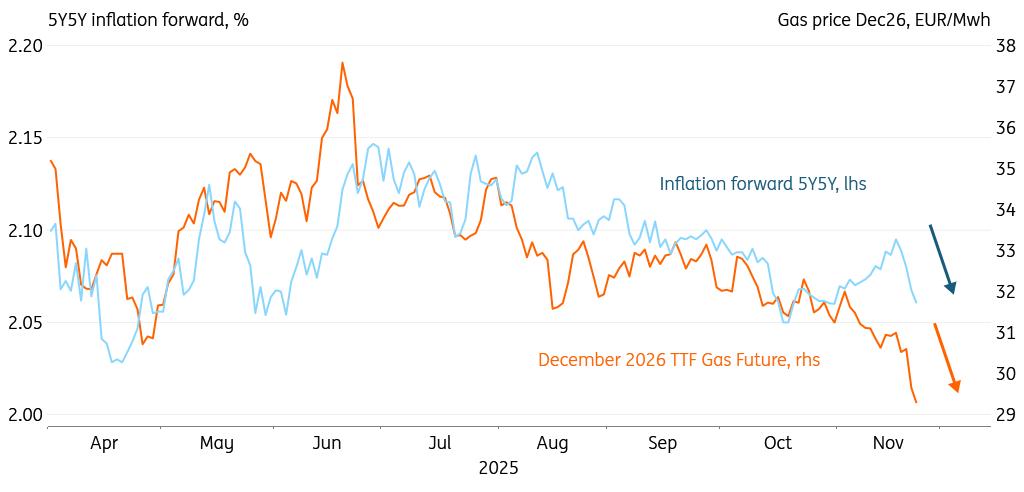

Hopes of a Ukraine peace deal are pulling down EUR inflation swaps

At first glance, a potential end to the Russia-Ukraine conflict is not impacting euro rates, but beneath the surface, we see more movement. Gas futures for December 2026 have fallen sharply in recent days, reflecting hopes that energy prices could ease on the back of a deal. In response, long-term inflation expectations fell lower again, with the 5y5y inflation swap back to around 2.05%, close to the 2% target. With downside inflation risks still well on investors' minds, we see further downside potential for rates if gas prices ease further amid prospects of a deal.

Despite lower inflation expectations, nominal yields, however, have held their ground, pushing real rates to new highs. The 5y5y implied real rate is now at 1.1%, which is the highest level since 2022. A rising real rate is a sign of a better growth outlook and positive risk sentiment. But at the same time, Bund yields are still well below the swap rate, indicating the demand for safe assets remains strong, and risk sentiment is still fragile. We are therefore hesitant to see real rates rise much more from here. Also, even if a peace deal is struck, the tensions with Russia are unlikely to disappear overnight.

Falling gas futures for December 2026 are helping to lower inflation expectations

Tuesday’s events and market views

From the US, we could start seeing a catch-up in data releases after the end of the government shutdown. We expect retail sales and PPI for September, but both are unlikely to be market-moving, especially since we already have the CPI number for that month. The consumer confidence numbers are likely to show some softness after Friday's weak University of Michigan measure. Lastly, we have pending home sales for October, which consensus sees rising by 0.5% month-on-month.

For supply, we have the Netherlands with 30Y DSLs for €2bn. The UK will auction 5Y Gilts for £4.5bn. Italy has a 2Y BTP, a 6Y BTPei and a 13Y BTPei totalling €4.5bn and Germany has €4bn of 5Y Bobls for auction. From the US we have a 5Y Note and a 2Y FRN for a total of $98bn.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more