How Czech companies are weathering the global geopolitical storms

- 3 July 2025

- Czech Republic

What are leading companies saying about the current financial landscape, and what are their biggest challenges? In our ongoing series, we're asking them. And today, we're looking at how Czech firms are adapting to an ever-changing and unpredictable landscape

Unpredictability is the new predictable

You don't need us to tell you that global events, notably since the pandemic, are running at a frantic pace. From the Russia-Ukraine war, the Middle East crisis, global tensions with China, and what many see as the retreat of globalisation. How are firms coping and adapting? It's an area of special interest for our Chief Economist, Marieke Blom, who's examining what business leaders are saying.

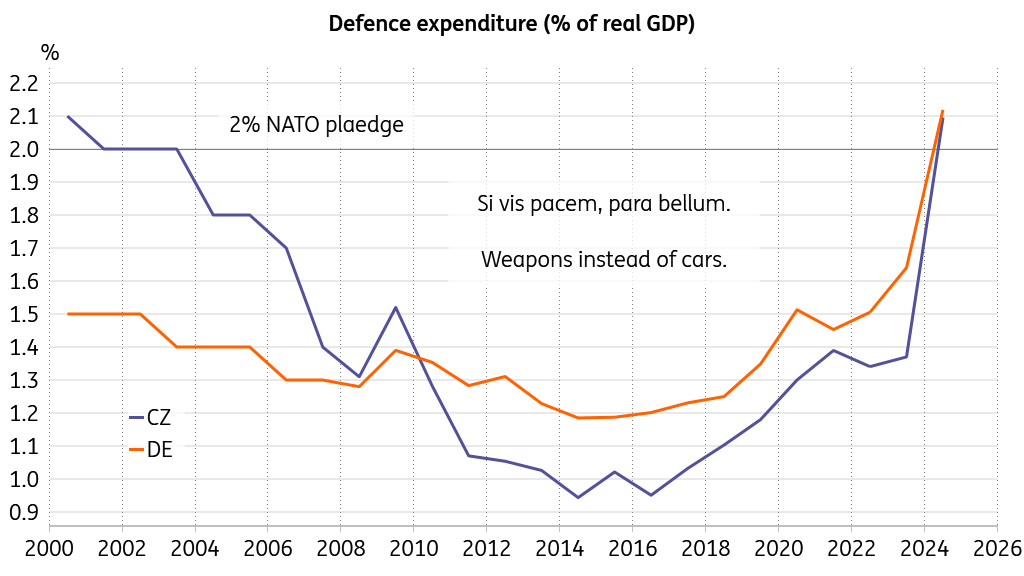

And I'm focusing on what Czech firms generally identify as the most prominent issues when looking ahead, especially from a medium-term perspective, and whether there are any common strategies for dealing with the rapidly changing conditions and heightened uncertainty. And all this comes at a time when European countries, in particular, are having to fund far higher defence costs, which could hit consumers hard.

Europe must boost its defence capabilities

The economic underperformance of European trading partners, high energy prices with no viable remedy, a lack of alternatives in strategic materials, the dumping of Chinese imports, a mounting regulatory burden, and geopolitical uncertainty hampering expansion abroad are among the most prominent medium-term risks as perceived by Czech businesses. Understanding various scenarios, employing more sophisticated hedging strategies, or being more vocal about the need for adjustments and agility are some of the approaches chosen to respond to the increasingly antagonistic global environment.

The most pressing medium-term hurdles for Czech firms

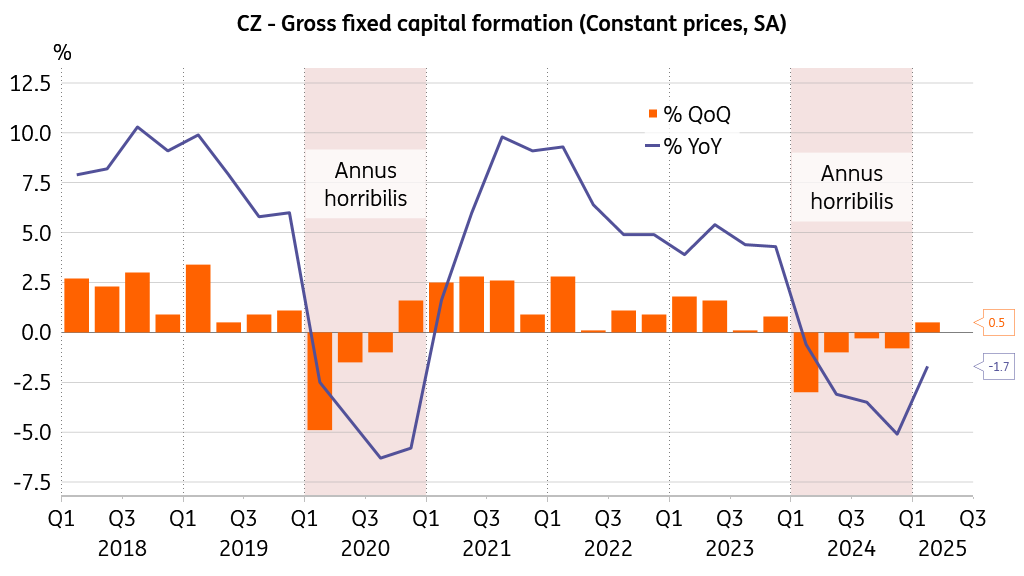

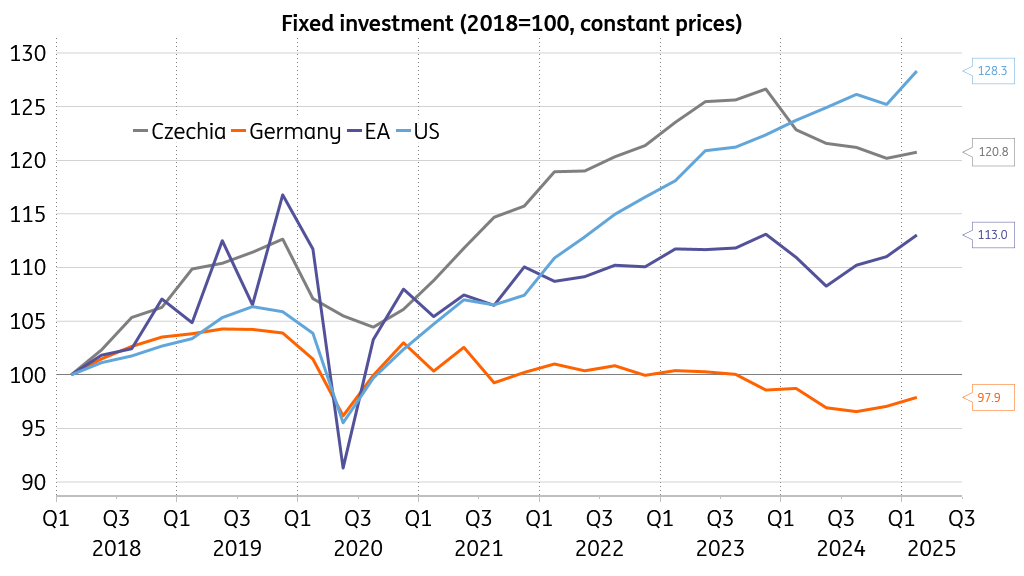

Fixed investment in the Czech Republic remains dormant, declining 1.7% annually in the first quarter of this year. In fact, the year's quarterly declines throughout 2024 brought the level of fixed investment roughly back to figures observed by mid-2022. So what's stopping Czech firms from undertaking bolder investment decisions? While most pressing issues are, of course, linked to the economic, social, and political landscape, a lack of clarity about Czech industry's role and prospects, along with the dismal outlook for European competitiveness, also play a significant role.

Here are some of our key observations:

Another awful year for Czech investment

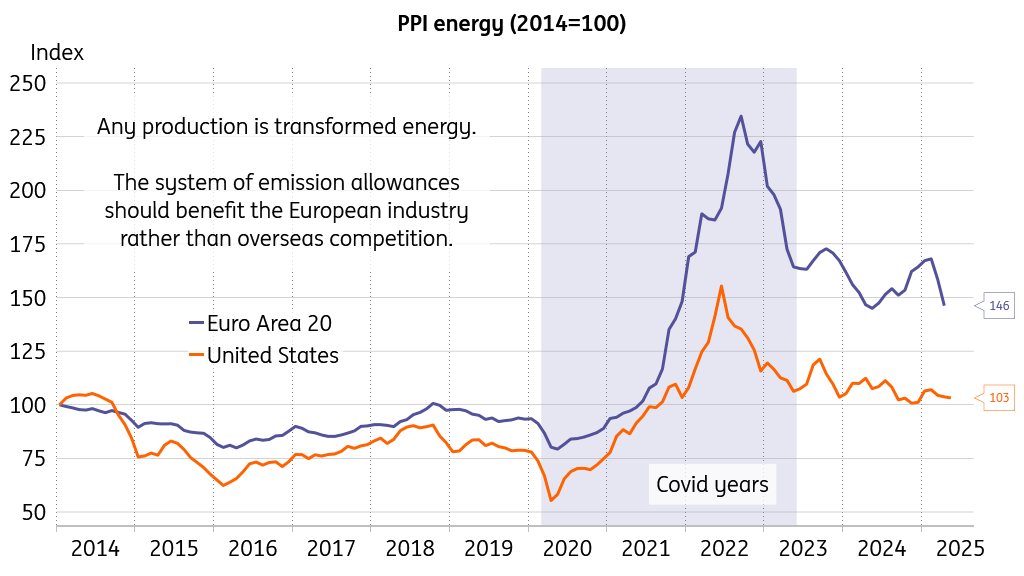

A European energy strategy is lacking

Europe lacks a viable energy strategy, with current energy prices providing a significant disadvantage compared to other countries with industry-focused energy policies. That said, the recent blackout in Spain likely demonstrates that increasing the share of renewables has its limits, especially if the transmission grid is not fundamentally strengthened. High energy prices for the industry are partially subject to the elevated price of emission allowances for businesses. Some Czech retail firms with European outreach are concerned that emission allowances for households could dampen their spending appetite once introduced or even in advance.

Energy-intensive industries are struggling

Energy-intensive industries are struggling and relocating from Europe. However, these often overlap with a renewed concept of strategic industries, such as metallurgy, chemicals, and generally heavy industries. The arms industry cannot continue to produce without steel. It would be challenging to build the dream ecosystem for microchip production without having domestically developed and produced advanced chemicals. We could go on for other segments of manufacturing, but none will prosper and invest without the prospect of a stable supply of energy and strategic raw materials at affordable prices.

Uncertainty about future energy prices is a drag

Significant internal trade barriers

The EU continues to face significant internal trade barriers, the impact of which is estimated to be equivalent to more than 40% of tariffs on goods. At the same time, precisely the free movement of goods and labour, together with the pan-European provision of services, constitutes one of the main leitmotifs of the Union. Presenting a diagnosis of the high internal barriers, which have not been addressed for several decades, is undoubtedly a somewhat outdated novelty. Still, the difficulties and persistently burdensome administration associated with introducing new goods for intra-European export are already a classic obstacle that Czech exporters must tackle.

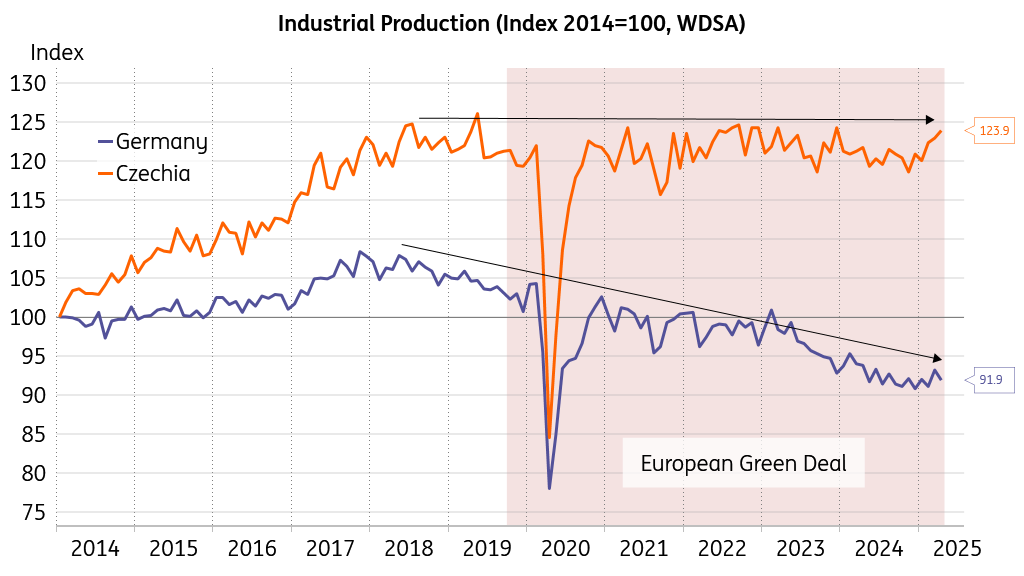

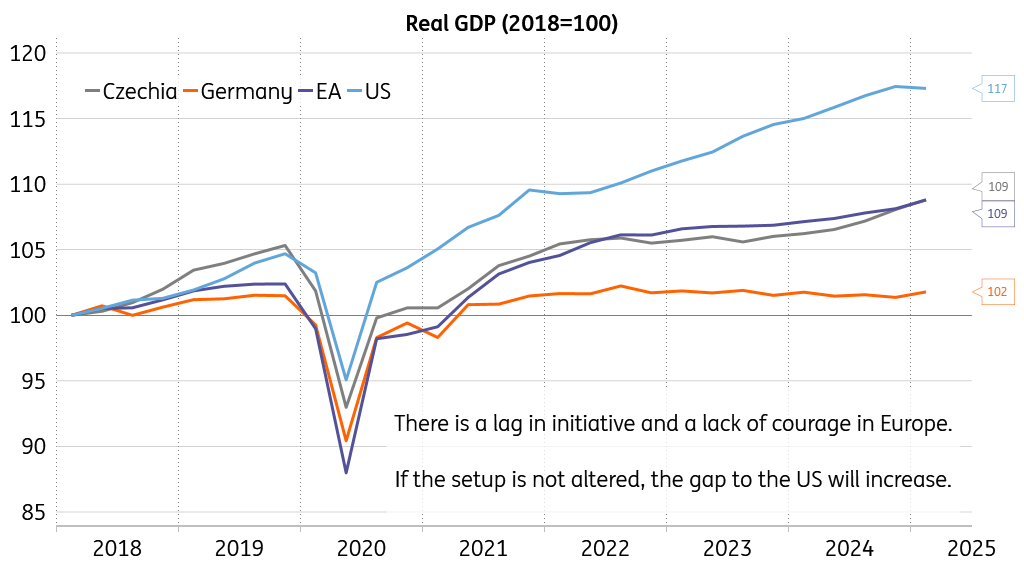

Czechia's most important European trading partners are not thriving economically, and the outlook is uncertain. Take the example of real GDP measured in purchasing power parity, i.e., the output of the economy adjusted for price and other regional differences, which is also suitable for comparing structurally differing entities. This statistic has risen by 27% for China, 19% for India, and 10% for the US in the five years to the latest measurement in 2023. Meanwhile, for European countries such as France, Germany, and Czechia, it has risen by no more than a meagre 3% in the same five-year period. Throw in the industry's reluctance to invest in Europe due to excessive regulation, prohibitively high energy prices, and other comparative disadvantages, and the outlook is not much rosier.

Industrial production has had it rough in recent years

An unlevel playing field

European leaders typically refer to the nearly half a billion consumers whose power they are willing to employ in establishing fair trading conditions for the continent. That said, the US and Chinese efforts to redesign the global trade landscape have been intensifying for almost a decade. There are undeniable government subsidies for Chinese production, which is at the same time more environmentally burdensome compared to the European one. However, there is still little action in the direction of setting fair conditions for European producers, who are facing dumping prices from Chinese companies that can bring their prices down to, or even below, the level of material costs. Czech manufacturers mention this topic across the board.

The ongoing US tariff negotiations, the most substantial reshuffling of the global trade landscape in decades, and the induced threat of trade wars concern Czech firms mainly due to their indirect impacts, which include dampening global demand, heightened uncertainty that may postpone investment plans, and potential disruptions to global supply chains. The same holds for more general geopolitical tensions, such as the escalation in the Middle East crisis, which makes the outlook for foreign exchange and the trajectory of interest rates less predictable.

The mitigation strategies

What can be the right attitude that would allow for an appropriate way forward in the volatile and competitive environment of today's world? There is a broad consensus that such a readiness encompasses three key things:

- a strong economic base that generates sufficient resources and enables maintaining some buffers,

- an ability to react promptly and decisively to emerging situations,

- a willingness to take the initiative and turn bold intentions into reality.

In the increasingly complex world, with the Pax Americana not guaranteed and Europe not enjoying unconditional protection from its larger brother, Czech firms feel the intense impact of previously adopted policies and prior decisions on both European and domestic levels. There is a general sense that firms should pay more attention and be more active at the very beginning when it comes to shaping the policies that affect their business. Such an adjustment in attitudes makes some umbrella organisations, such as the Czech Chamber of Commerce, more agile and vocal, especially in these times when the Czech industrial base faces protracted headwinds.

Czech businesses are more likely to opt for various hedging strategies during uncertain times, primarily in the areas of exchange rates and interest rates. Given the cost of hedging, CFOs are more inclined to explore even more sophisticated setups for shielding themselves against unexpected fluctuations at an acceptable price. Many production firms have gained experience with supply chain disruptions that directly affect their operations, leading to a tendency to maintain a buffer inventory of critical inputs and diversify their suppliers.

As mentioned, it has become difficult or impossible to diversify into European-made products in certain areas, such as the chemical and pharmaceutical segments.

Today's investment is tomorrow's economic growth

The decision-makers in Czech companies are also more likely to discuss alternative scenarios and are more oriented towards understanding the Czech economic story within the global context. Consequently, there is nowadays a greater appetite for an elaborate story about what might happen in the US or China, rather than just in Germany. Such a development is closely tied to the gradual decoupling of the Czech economy from the underperforming German one, while there is increased interest in exploring investment opportunities in the US.

Advantageous energy prices, less burdensome regulation, and swifter processes in matters such as building permits are the main pros, while uncharted waters and potential shortages of a skilled labour force are the cons when thinking about US investment strategies.

Europe needs more initiative and action on a global scale

In recent decades, the old continent was not accustomed to fighting for its interests and a place in the sun, being shielded by the willingness of the US to carry the burden of keeping trade routes open and the lack of excitement about dodging the fare. However, times have changed drastically, and Europe's attitude must adjust accordingly.

The first rule of any organism is 'adapt'! The Czech industrial base is uncertain about the level of general support and the future position of European industry in conditions of cut-throat global competition, with a greater push to advance national interests worldwide.

The gap with the US is getting more potent

If others do not take you seriously, the overall situation is beyond your control, or in fact beyond your reach. It is then from the realm of dreams to hope for achieving favourable or at least reasonable terms for Europe-based firms on the global chessboard in the long term. The EU's diplomacy is not backed by adequate military power, yet it is also incapable of exploiting economic levers such as access to its consumers. Mostly, it is hardly capable of formulating adequate observations and bold proposals addressing current world events that would match the pulse of the times. Kaja Kallas's speech on the situation in the Middle East was disarming in this sense: it would have been hardly possible to make more banal statements in a six-minute-long performance.

Yet again, formulating clear statements on global matters and proposing bold strategies promptly to safeguard Europe's position in a dynamic world would reassure investors that it is the preferred place to be. Some review of core goals and adequate means could make a significant contribution to the old continent's readiness to respond effectively to the challenges of the twenty-first century. These are likely to only grow in number, become increasingly complex, and require the art of translating courage and determination into reality.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more