Pathway to net zero: Tackling emissions in construction

If construction companies want to be climate neutral by 2050, they need a comprehensive plan that looks beyond their own operations to the entire value chain, which is a major emitter of greenhouse gases. This ambitious goal demands diverse measures to address both direct and indirect emissions. It's not yet clear how committed the industry will be

The construction value chain contributes significantly to total greenhouse gas emissions, yet the portion directly attributable to construction companies is relatively small. Despite this, many larger European construction firms have set emissions targets, albeit with wide variations. Achieving their ambitious 2050 goals will require significant efforts, including the electrification of equipment and vehicles.

The size of CO2 emissions in construction

At least a 55% reduction in greenhouse gases by 2030

Despite ongoing discussions about sustainability, construction companies are becoming increasingly engaged with these efforts. They must comply with the Paris Climate Agreement. Also, the Green Deal has been adopted in the European Union, with EU member states agreeing to cut CO2 emissions by at least 55% by 2030 compared to 1990 levels. By 2050, the EU wants to be climate neutral, which means that no net greenhouse gases will be emitted.

Low direct emissions in construction

Construction companies have relatively low direct emissions (scope 1, see box) of greenhouse gases. Of the total EU emissions, only 1.7% is directly attributable to construction. This largely consists of emissions from construction vehicles and passenger cars and trucks under their own management.

Only small proportion of CO2 emissions is directly caused by construction

Indication direct share of total EU CO2 emissions, 2022

But many more emissions in the entire chain

If construction companies want to be climate neutral by 2050, they need to look beyond just reducing emissions from their own operations. The vast majority (more than 90% of total EU emissions) of greenhouse gas emissions from construction activities take place in the value chain, at suppliers (upstream) and clients (downstream) for example via the production of steel and concrete and from users of buildings built by them through heating and lighting (scope 3).

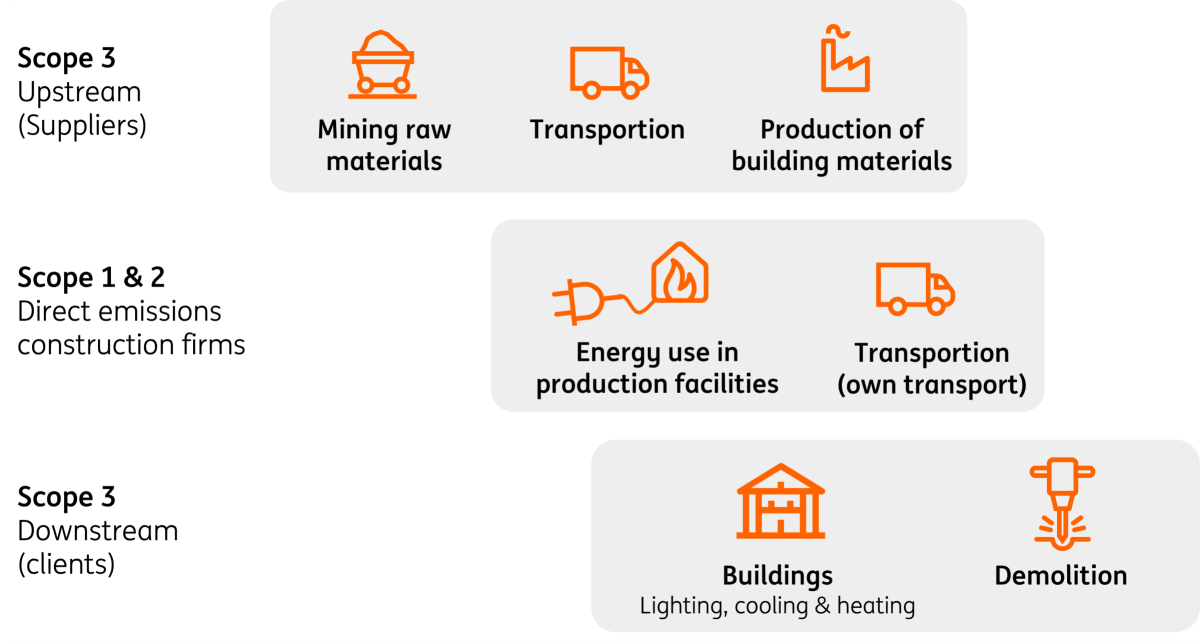

What is scope 1, 2 and 3?

Activities that generate emissions are typically grouped into three streams:

Scope 1 concerns the direct emissions of the company itself. This includes the gas consumption to heat its own buildings, diesel consumption of its own construction equipment and its own vehicle fleet;

Scope 2 concerns the company's indirect emissions, such as the purchase of electricity for the head office and use of electricity on the construction site;

Scope 3 are all other indirect emissions in the entire value chain, both at customers and suppliers. This includes emissions related to purchased building materials, transport by third parties, commuting by staff, business travel, waste and emissions related to the use of the built property.

Schematic breakdown of emissions in the construction sector

Major share of CO2 emissions from contractors lies with suppliers and customers

Indication of distribution of CO2 emissions in the EU construction sector

Dutch and Belgian construction are relatively polluting

If we compare the direct emissions from construction (scope 1) in different EU countries, we see that they are relatively high in the Netherlands and Belgium. In Spain and Poland, on the other hand, these emissions are relatively low. The higher emissions in the Netherlands and Belgium seem to be partly explained by a composition effect. Construction companies in the Low Countries are relatively small and the renovation market is relatively large. As a result, there are probably more transport movements and therefore more direct emissions. However, despite the large differences between countries, we must bear in mind that the total direct emissions from construction (scope 1) are relatively limited.

So the emissions are mainly coming from the suppliers. In the European Union, the average emissions of the energy-intensive building materials industry as a share of value added are about a factor of 30 higher than in the construction sector. It is striking, however, that the Dutch building materials industry has relatively low emissions. This is largely due to the relatively high gas and electricity consumption in this sector in the Netherlands, which releases relatively fewer greenhouse gases compared to other fossil fuels (such as coal and oil, which are still used in many other countries). In the Polish and Spanish building materials industry, on the other hand, these energy carriers are still used relatively often.

High CO2 emissions in Dutch and Belgian construction

Ratio of CO2 equivalent emissions (thousand tons) compared to the added value of the construction sector (in million euros), 2022

But low CO2 emissions in the Dutch building materials industry

Ratio of CO2 equivalent emissions (thousand tons) compared to the added value of the building materials industry (in million euros), 2021

Emissions decline in construction sector lags behind the economy as a whole

Now that we have some insight into how much the construction chain emits in total, and across different countries, let's focus on the reduction of greenhouse gases. Unfortunately, figures for the reference year 1990 used for the international objectives are not available. So we use 2008 instead. In 2023, total emissions in the European Union had fallen by almost 25% compared to 2008. However, the direct reduction in emissions from the EU construction sector lags far behind at only 11%. The construction sector therefore still has some catching up to do.

The building materials industry has already made great strides

The building materials industry has already made significant strides. Emissions in this sector were more than 30% lower in 2022 than in 2008. This is mainly due to the fact that highly polluting energy carriers such as coal and oil products have partially been phased out. For example, in 2014, more than 108,000 terajoules of coal were still used in the European Union. This has dropped to less than 80,000 terajoules in 2021.

Decline of CO2 emissions lags behind in construction sector

CO2 emissions European Union (Index 2008 =100)

European construction company goals

To achieve emission reductions, builders must first start by mapping their own greenhouse gas emissions and set reduction targets. Large companies are also increasingly obliged to do so by legislation.

Majority of contractors aim for net zero by 2050

25 large construction firms with net zero target companies (scope 1)

Construction companies' climate goals

We analysed 25 large European construction companies and found that 70% of the companies have published concrete climate targets for scope 1 and 2 emissions.

Almost 50% of contractors have a reduction target for scope 3

EU construction firms with a reduction target

Scope 3 most challenging objective

Of the 25 companies analysed, almost 90% have published a reduction path (not necessarily leading to net zero) for scope 1 & 2 in which they indicate how much they want to reduce their greenhouse gas emissions. For scope 3, this is only 48%. This is not surprising, as emissions in scope 3 are much more difficult to map and reduction targets are also much more difficult to achieve. After all, you have to collect information from your entire value chain and work with suppliers and customers to achieve these objectives.

Even the companies that do not have a concrete target have almost all published some CO2 reduction plans. However, the objectives are often not translated into specific goals for all activities. For example, specific goals are often set for the fleet, but a comprehensive plan is lacking.

Different reference years

Reduction targets set by the companies are difficult to compare because the reference years vary from 2009 to 2023. The reduction target years and the intended path to be followed are also often different. The graph below shows these variations for several large companies analysed. Of the 10 largest construction companies we surveyed, BAM and Skanska have the most ambitious reduction targets.

Wide variations in reduction targets

Planned CO2 reduction target path (linear), Index company base year=100 (period 2015-2030*)

How can companies achieve the goal of net-zero?

To meet climate targets, construction companies need to take significant steps to reduce their CO2 emissions. Greenhouse gases are released during many activities, so a wide range of measures is therefore needed. We discuss the most important ones per scope below.

Scope 1: Direct emissions

- Electrification of equipment and vehicles

Investing in electric construction equipment and vehicles can eliminate direct emissions. In particular, smaller electric excavators, bulldozers and trucks are increasingly available and can drastically reduce emissions on construction sites. Bottlenecks here are often the higher purchase costs and the required charging infrastructure. This can range from simple charging stations to advanced fast charging stations and mobile batteries for construction sites where no other charging facilities are available. - Use of clean(er) fuels

Switching to biofuels or hydrogen can significantly reduce CO2 emissions. Biofuels are produced from renewable sources such as vegetable oils and waste, while hydrogen is especially more sustainable when produced with renewable energy. For example, HVO (Hydrotreated Vegetable Oil) can be used in many regular diesel engines, but is not yet available everywhere and is currently more expensive. However, the Dutch contractor TBI Holdings, for example, has already decided in 2023 to use HVO on all its construction sites. - Efficiency improvements

Limiting transport movements as much as possible, economical use (e.g. driving more slowly) and regular maintenance and optimisation of machines and vehicles can improve efficiency. For example, by driving slower, you can quickly save 10% fuel and thus also limit greenhouse gas emissions. In addition, reducing transport distances can be done, for example, by using a construction hub. The necessary building materials are taken to a central location outside the city and then transported to the construction site in one journey, which reduces the number of kilometres driven. - Making business premises energy-neutral

Construction companies' own buildings must also be made emission-free. By better insulating and switching to a heat pump, for example, the gas consumption of the company's own office can be addressed.

Steps towards emission-free construction

Scope 2: Indirect emissions from energy consumption

If emissions in scope 1 decrease due to electrification, for example, they often increase in scope 2 because power consumption increases. Extra steps must therefore be taken here. Possible options are:

- Self-generation of renewable energy

Generating your own electricity by installing solar panels on the company's premises or buildings can help to reduce dependence on fossil fuels and reduce CO2 emissions. - Renewable energy procurement

Construction companies can switch to an electricity supplier that supplies 100% renewable energy. The Swedish construction company Skanska, among others, already uses 93% renewable electricity of its total electricity needs. - Energy efficiency

Here too, energy saving can help to reduce use and thus emissions in this category. Implementing smart meters and energy management systems to monitor and optimise energy consumption can contribute a lot to this.

Subsidies, pricing and/or regulations?

Tackling greenhouse gas emissions requires a combination of measures from both construction companies themselves and the government. The effectiveness of measures depends on the context and the specific circumstances.

Business initiatives: Companies can act proactively with their own reduction targets. However, there is a danger that this will worsen the competitiveness of these companies due to higher costs and that initiatives will be limited to a small number of companies.

Customer demand: Construction companies can reduce their emissions to meet the requirements of environmentally conscious customers. Because a large part of the construction orders come from government agencies, which more often include sustainability requirements in tenders, this can certainly bring about a shift. However, not all clients consider sustainability to be of paramount importance.

Government regulation: Legislation is crucial to create a level playing field and ensure that all companies start contributing to the reduction of emissions. Strict environmental regulations can thus force companies to adopt cleaner technologies and reduce their emissions.

Pricing emissions: Pricing CO2 emissions, for example through a CO2 tax or emissions trading systems (e.g. ETS) is one of the most efficient ways to reduce emissions (e.g. on concrete and cement). It creates a financial incentive for companies to reduce their emissions and stimulates innovation in clean technologies.

Government subsidies: Subsidies accelerate the transition to a zero-carbon economy by supporting investments in renewable energy and other green technologies. This is particularly useful in the early stages of new technologies that are not yet competitive without financial support. However, a disadvantage of subsidies is that they entail (considerable) costs for the government. In addition, they do not encourage other energy-saving measures such as other innovations and more efficient behaviour.

In practice, a combination of these measures is often the most effective. Government regulation and emissions pricing encourage companies to take action, while subsidies support the development and implementation of new technologies. It is important that these policies are consistent and clear so that companies can prepare for them well in advance. Business initiatives also contribute to a culture of sustainability and innovation.

Scope 3: Other indirect emissions

We have already seen that by far the most greenhouse gases in the construction chain are emitted by suppliers of building materials (upstream) and also during the final use of the buildings (downstream). This also makes this the most difficult scope to tackle because cooperation with other companies often has to be sought to achieve this. Here we show different options for both upstream and downstream.

Upstream

- Other (biobased) materials

Construction companies can choose to use materials that are less energy-intensive, which significantly reduces the total CO2 emissions of a construction project. For example, wood can be used for many structures instead of concrete or steel. - Circular construction

Circular construction helps reduce waste and emissions by limiting the use of new building materials and recycling and reusing materials. This can be done, for example, by opting for renovation instead of demolition and new construction, separating waste streams on the construction site and looking for opportunities to reuse materials. - Suppliers involved

Involving suppliers in targets can help reduce their CO2 emissions. This can be done by making agreements together to implement sustainable practices and by working together on joint CO2 reduction projects. The commonly used basic products, concrete, steel and plastic, can each be produced in different ways with far fewer CO2 emissions.

Downstream

Emissions must also be reduced to zero during the eventual use of the constructed buildings. There are various regulations for this, such as the EPBD of the European Union. The ultimate goal is to make buildings completely energy-neutral. Construction companies can do this in several ways:

- Energy-neutral buildings

By means of, for example, good insulation, heat pumps and self-generation of energy with solar panels, buildings can be constructed that no longer use (and sometimes even generate) net energy. - Making strategic choices

Companies can also make strategic choices about what they still build. For example, energy-intensive wellness centres and data centres may fall outside the company's goals.

What to do as a construction company?

Reducing CO2 emissions in the construction sector requires an integrated approach that addresses both direct and indirect emissions. By investing in technologies, sustainable practices, and working with suppliers and government, construction companies can make a significant contribution to climate goals. Construction companies can choose to be a frontrunner or to follow the general trend and regulations. Both have their own advantages and disadvantages.

Leader

Construction companies can choose to be at the forefront of net-zero, with targets that are much stricter than legislation requires. This can make them attractive to clients with their own sustainability requirements and attract environmentally conscious staff in a tight labour market. Moreover, it helps to limit CO2 emissions, so that global warming increases less quickly. The downside is that these companies sometimes have to pull the chestnuts out of the fire by investing in new sustainable technologies that are not yet always fully proven. They may also have (temporarily) higher costs, which means that a lower profit margin must be accepted.

Follower

Construction companies can also choose not to be ahead of the curve and to limit themselves to the legal standards. They can be advantageous in terms of costs, but it is also possible that they miss out on assignments due to stricter sustainability requirements from clients. This can weaken their competitive position. Moreover, they run the risk of having to invest in sustainability later and having to write off equipment that turns out not to meet new standards. This could result in less time to adapt to new regulations, which also worsens the market position.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article