Energy Outlook: Oil and gas prices to remain elevated

- 26 January 2022

- Commodities, Food & Agri Energy

The exceptional strength in energy markets over 2021 has continued into 2022. Growing geopolitical risks and supply disruptions have proven constructive for prices. Oil should correct lower as supply disruptions subside. However, the gas market will likely remain volatile at elevated levels

Back to surplus for oil

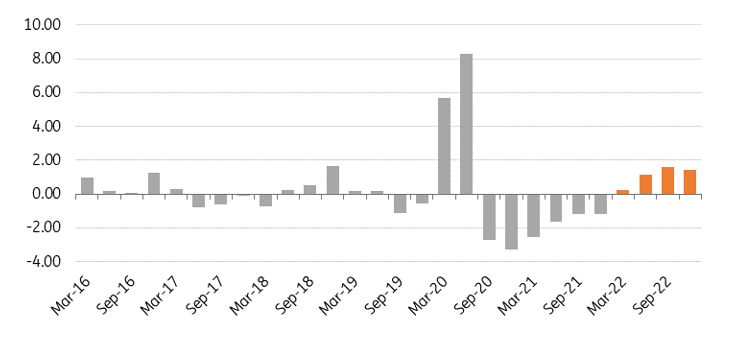

The continued unwinding of OPEC+ supply cuts, along with strong non-OPEC supply growth, should see the global oil market return to surplus from 2Q22. Several supply issues coming into the new year, along with good demand has delayed the return to surplus. Once back in surplus, we expect that the market will remain well supplied until at least the end of this year. However, if OPEC+ believes that it needs to pause its monthly production increases at any stage through the year, this would have an impact on the oil balance though in the current price environment, this is unlikely.

The global oil market set to move into surplus from 2Q22 onwards

Global quarterly oil balance (MMbbls/d)

The expected return to surplus means we forecast ICE Brent to average US$76/bbl over 2022, down from the highs seen in early 2022, but still well above the average levels seen since 2015. Longer-term concerns over the lack of investment in upstream oil, along with falling OPEC spare capacity (as the group eases cuts) will likely put a floor under the market while geopolitical risks should also offer support.

There are several risks for the oil market. On the downside, the most obvious is the return of Covid related restrictions. While a number of countries have accepted the need to live with Covid-19, China continues to pursue its zero-Covid policy. This is a clear downside risk for oil demand if we were to see wide-scale lockdowns across China once again. At the moment, the market does not appear to be pricing in this risk.

In terms of the upside risks to prices, two stand out. Firstly, Iranian nuclear talks are ongoing. If these were to fail, it would reduce the scale of the surplus that is expected over 2022. Admittedly, the slow progress made in talks so far means that the market is likely coming to the realisation that there will be no quick return of Iranian barrels.

Secondly, and very important for the market, is the ongoing tension between Russia and Ukraine. Any escalation would likely lead to increased volatility and stronger energy prices. While Russia is a crucial natural gas supplier to Europe, an escalation would also be supportive for oil prices. Russian oil exports averaged around 4.5MMbbls/d over 2021, so any actions which aim to limit these significant flows would be bullish.

Little relief expected for the European gas market

It is difficult to find a quick solution for the tightness in the European natural gas market. EU gas storage is now below 45% full, compared to a five-year average of around 60% for this stage of the year. Russian gas flows into Europe have fallen significantly coming into the New Year, which has tightened up the market at a fairly quick pace. Flows transiting via Ukraine have fallen sharply. The Yamal-Europe pipeline is also seeing reverse flows from Germany into Poland, rather than flowing in the usual westwards direction.

It is still to be seen how much relief the LNG market will provide to Europe. Towards the end of last year, a number of LNG cargoes were directed to Europe given the surge in prices. We could see more of this in the near term given that European prices are trading at a premium to Asia once again. This trend will continue until around the middle of the year.

It has become increasingly apparent that the European gas market will likely finish the heating season at record lows. A late end to the heating season could certainly leave the market in an extremely tight spot. This tightness and uncertainty over how low inventories will fall mean that European gas prices are likely to stay at elevated levels for much of 2022. While we should see a downward correction in prices as we head into the lower demand period of spring and summer, prices are likely to remain historically high given the need to rebuild inventories over the injection season.

It has also become clearer that the ongoing tightness in the European natural gas market is likely not a one-off. Instead, we are likely to see a fairly tight European market going into next winter as well. However, this will really depend on developments with Russian gas flows. If these continue to remain below normal levels during the injection season, Europe will likely have to deal with another winter of elevated prices. Regulatory approval of Nord Stream 2 could help with flows but given the growing tensions with Russia, this is not guaranteed.

A key upside risk for European gas prices is a further escalation in tensions between Russia and Ukraine. Ukraine is an important transit route for Russian gas into Europe, whilst Russia is the largest supplier of natural gas to Europe, meeting almost 50% of import demand. Any escalation that leads to conflict or sanctions which target energy exports has the potential to significantly tighten the European gas market. You can read here what this will do to European power prices.

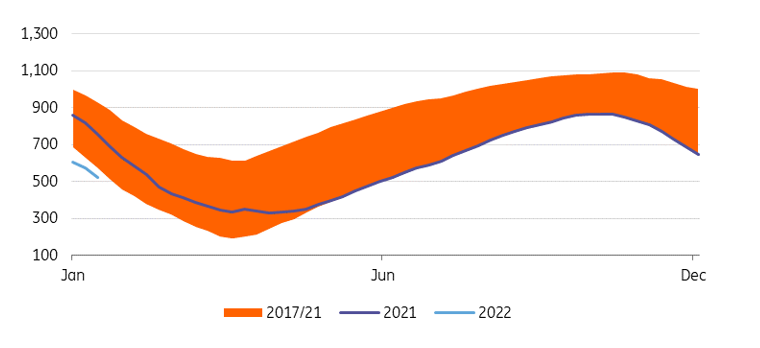

European gas inventories on track to finish heating season very tight

European natural gas inventories (TWh)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Energy Outlook 2022: Powering ahead

- This bundle contains 5 Articles