No need to touch Czech interest rates despite upbeat core inflation

- 13 May 2026

- Czech Republic

Czech headline inflation is mitigated by the still muted food price dynamic. Meanwhile, core inflation is set to remain elevated while shaped by opposing forces of higher energy prices and tighter budgets. Regulated prices pose a risk to price stability, yet positive real interest rates suggest stringent enough policy as risks to growth mount

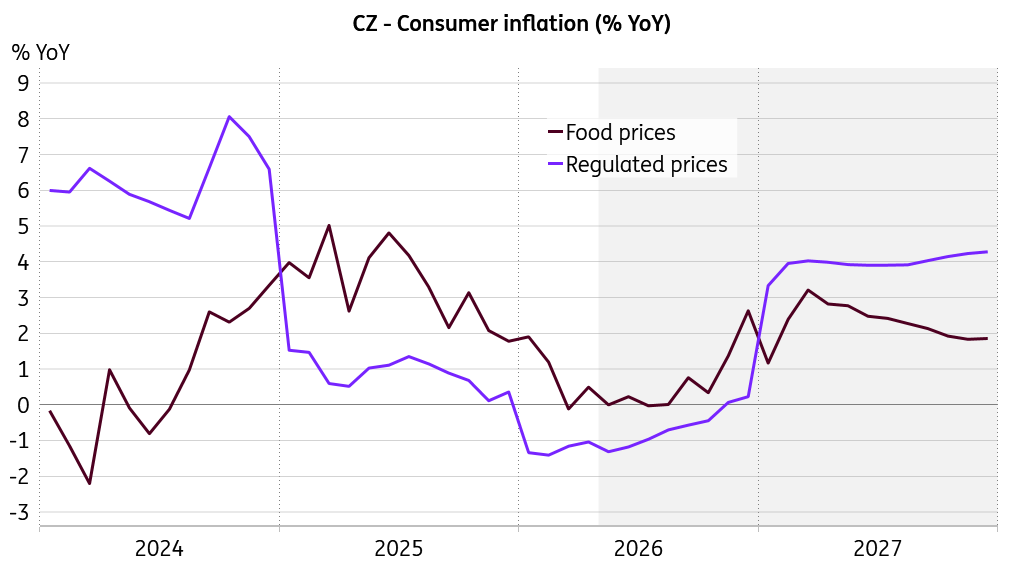

Food prices hold headline inflation back

Czech consumer inflation was confirmed at 2.5% year-on-year in April. The monthly increase of 0.5% was again driven mostly by higher prices in the transport section because of the global energy shock. We saw prices crawling up in the alcohol and tobacco section. The price gains in the housing section were mainly driven by higher imputed rents, along with charges for heat and hot water. April’s imputed rents dynamic is in-line with our mild scenario simulation for this item. In contrast, foodstuffs recorded another monthly drop and carried on in annual decline. Prices of goods gained 1.1% YoY in April on aggregate, while prices of services added 4.8% YoY.

Core rate set to remain elevated

With annual core inflation at 2.9% in April, we expect this measure to remain punchy over the year. Still, we will witness two counteracting forces in the price domain. Higher energy prices will trickle down through all other price circuits as second-round effects on the one hand. Meanwhile, a tighter budgetary constraint due to higher energy bills will dampen the ability and willingness to spend, especially on discretionary items. Add the approaching pressure on economic activity linked to the global negative supply shock, and I believe that you would hardly bet your bottom dollar on how the resultant force vector emerges.

Headline inflation set to peak early next year

We expect core inflation to average just below 3% and to gradually soften toward 2% over the next year. Fuel prices are about to drop in May based on preliminary price surveys, as the margin ceiling for fuel stations set by the government starts to kick in as a binding condition. To capture this administrative measure, we plug in a rather extensive expert judgement of -4% to May’s monthly fuel prices that reverts the dynamics suggested by sole model forecast based on exogenous variables such as oil price and exchange rate. This is the decisive factor that takes this year’s headline inflation outlook somewhat below our previous projection. In the end, along with volatile food prices, we must welcome yet another enfant terrible into our projection exercise, which is administered fuel prices. And I am sorry for this change, as in the model it works wonderfully well for fuel prices.

Regulated and food prices pose risks to next year's inflation

In any case, headline inflation gets punchier next year on average due to a more pronounced increase in regulated prices. The large energy distributors have quite some leeway before they must purchase energy for ample market prices, but as the Middle Eastern conflict gets protracted, we will likely see more propensity to raise electricity and natural gas end prices at the onset of the upcoming year. For sure, we may anticipate some government measures to mitigate the impact on households and firms, yet it is too soon to implement a particular judgement into our forecast at this stage.

Don’t push the economy across the cliff

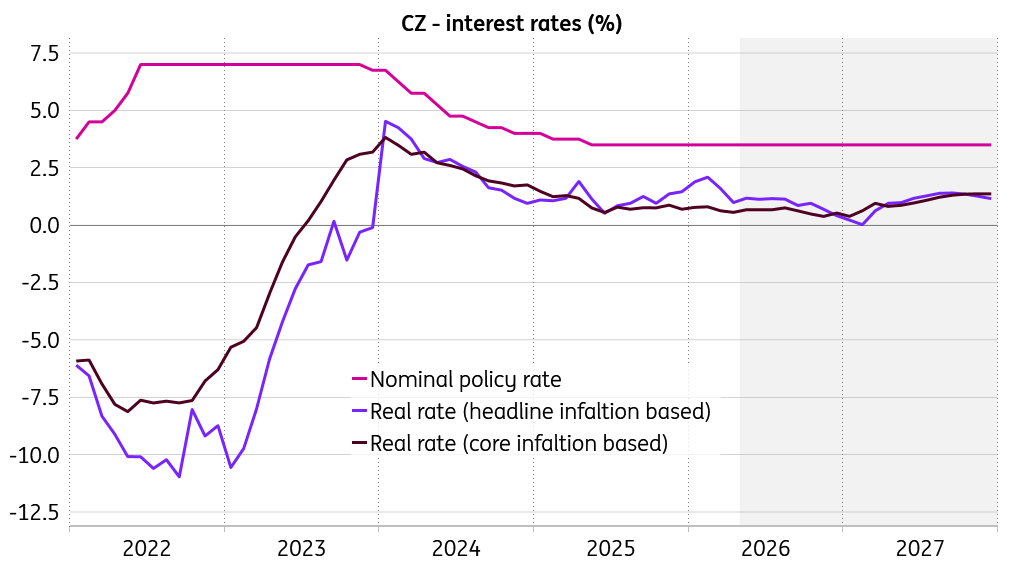

In the current situation, we come back to the basic rule of the Hippocratic Oath: primum non nocere. So, don’t push the economy across the cliff via higher capital costs, especially as it’s tough to quantify the upcoming negative consequences for growth right now, with sharp discontinuities taking shape on the horizon as the global shock drags on. It seems that the Czech National Bank is on the same page and will proceed in soft gloves, keeping the base rate untouched.

Real interest set to remain in the positive territory

Considering our base case scenario with Brent Crude prices hovering above US$100/bbl until August and then gradually receding, the real interest rates would remain mostly positive, which could be deemed as having a restrictive effect on economic activity. With a growing potential for economic nausea, there is not much need to make conditions for households and firms even tougher in times of ample uncertainty.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more