Net energy channel dominates Asia’s response to the Ukraine war

- 31 March 2022

- Australia China

Of the various channels we wrote about last month which could affect Asia's economies, the net energy balance is so far the most dominant. Inflation differentials could take the lead in the months ahead

FX losses mirror energy balance

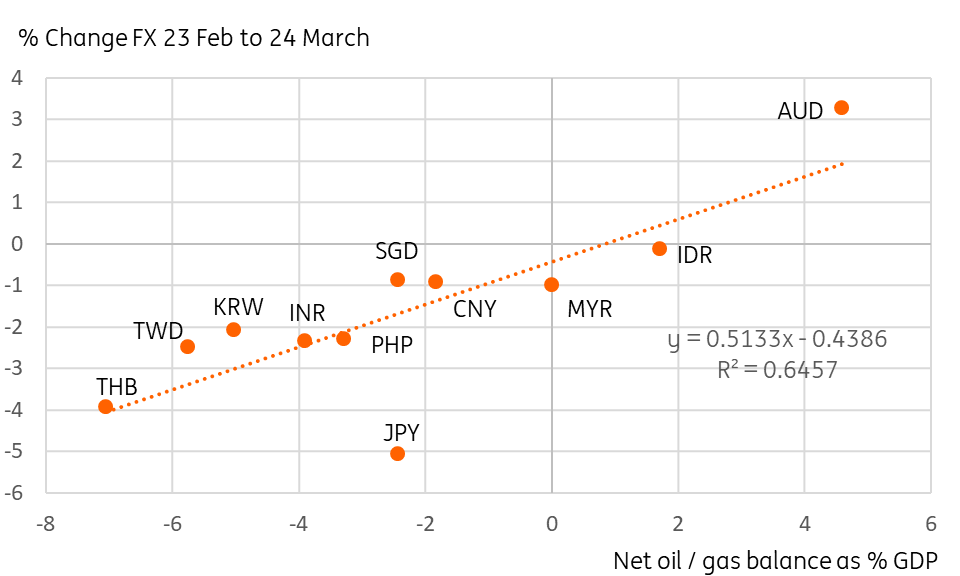

We wrote last month that Asian exposure to the Russia-Ukraine war was relatively light, though the word “relatively” was doing a lot of heavy lifting in that sentence. FX volatility since then has been anything but light. Within the APAC region since the February 24 invasion, there have been very few gainers. The Indonesian rupiah and Australian dollar stand out, with the Malaysian ringgit not far behind.

Holding up the bottom of the table, the KRW, THB, JPY and TWD have lost the most ground. That group includes three of the region’s most developed economies. The Japanese yen is a bit of an outlier.

But even so, of the various channels through which the war may affect APAC economies, the balance of trade in oil and gas seems to be the most powerful. This is a fairly straightforward terms-of-trade effect leading to a greater weakening of the currencies which are most exposed to energy price surges.

FX Performance and net energy balance

Inflation differentials may dominate the next leg

One complicating factor to this is the role of the Chinese yuan. China is the supersized local economy. And the CNY’s strength acts to some extent as an anchor in the region, conferring stability to Asian “satellite” currencies.

Recently, the CNY has also shown a limited degree of additional volatility, and that has had the effect of allowing other currency pairs to fluctuate more wildly. There is no one cause for that recent additional volatility. But the following factors seem likely to have played a role:

- China’s Covid outbreak

- Worries about future sanctions relating to possible support for Russia

- Stock market outflows (derived from 1 and 2 above)

- China’s still very low inflation, requiring less FX stability to be maintained

The energy balance will probably not remain the only channel through which Asian currency volatility plays out. On a slightly longer timeframe than the next few weeks, the inflation impact could also be meaningful. As we noted last month, particularly in the terms of how important food and energy are in the CPI basket, there are some wide differences across the Asia spectrum that could see some currencies softening more than others from an inflation differential perspective.

Before that becomes evident in the macro data, we might be able to see some sign of that showing through in bond markets. So far, since the invasion, 10Y yields on Indonesian and Philippine government bonds have widened the most in the region. We would also keep a close eye on Indian bonds which we expect will also be one of the bigger movers.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: There’s nothing normal about the global economy

- This bundle contains 17 Articles