National Bank of Hungary Preview: Embracing the present

- 25 January 2024

- Hungary

Despite a clear deterioration in external risks, we believe that favourable internal developments, accompanied by recent comments from Deputy Governor Barnabás Virág, will tip the balance towards a 100bp cut. However, if the forint continues to weaken markedly, then the previous 75bp pace will likely be maintained

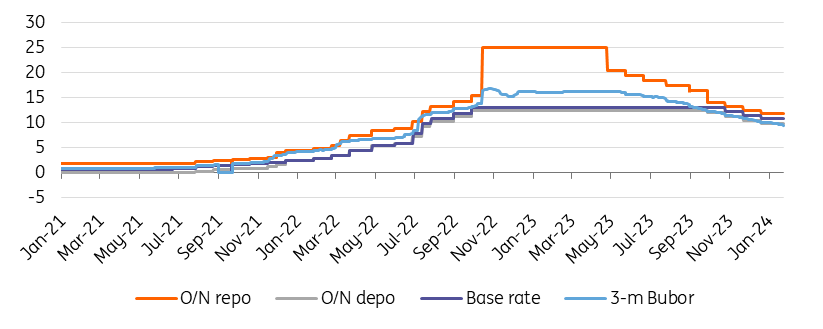

The decision in December

The National Bank of Hungary cut its key interest rate by 75bp to 10.75% in December. At the same time, the central bank has given clear indications that the pace of rate cuts may be increased if internal and external developments allow, as we discussed in our last NBH Review.

The main interest rates (%)

Internal developments strengthen the case for a larger cut

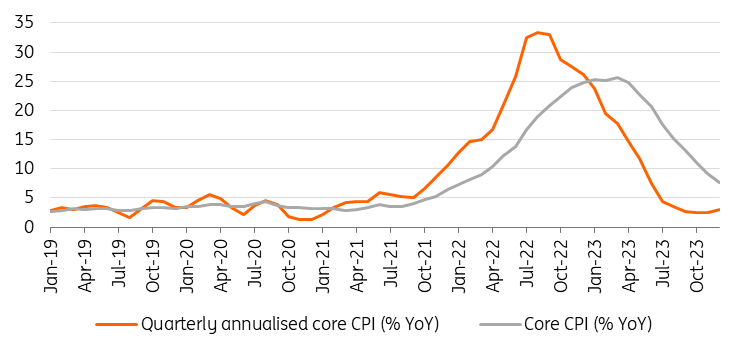

Headline inflation fell by 2.4ppt to 5.5% year-on-year (YoY) between November and December, which in fact was a downside surprise compared to our 5.7% forecast. However, what’s more important is that December’s figure was 0.2ppt lower than the central bank’s own estimate, published in the latest Inflation Report.

Other measures of price pressures also look favourable, as core inflation decelerated to 7.6% YoY in December, while on a three-month on three-month basis, it was below 3%. At the same time, the National Bank of Hungary's measure of inflation for sticky prices also decreased, displaying a reading of less than 8.7% YoY.

Underlying inflation indicators

The country's external balances are also improving, as the trade balance has been in surplus for 10 months, and even reached an all-time high of EUR 1.7bn in November. As for the current account, we have already seen surpluses in the second and third quarters of 2023, and we expect it to remain in positive territory at the end of 2023.

External developments warrant a cautious approach

Let’s start with two of the positive developments regarding external risks:

- We've already seen a dovish pivot from the Federal Reserve, and we expect the European Central Bank to follow suit at some point. This means that the next move for both central banks will be a cut rather than a hike, which in turn means that the HUF carry will not decline as much going forward as it would have if these central banks were still in rate-hiking mode. Even though rate cut expectations have been slightly dialled down compared to the time of the December NBH meeting, the direction of travel is favourable for emerging market currencies, including the HUF.

- One of the key uncertainties has been removed with the positive decision of the European Commission on the horizontal enablers (judicial reforms). With Hungary now having access to around EUR 10.2 bn of Cohesion funds, this could increase risk appetite towards Hungary and support market stability.

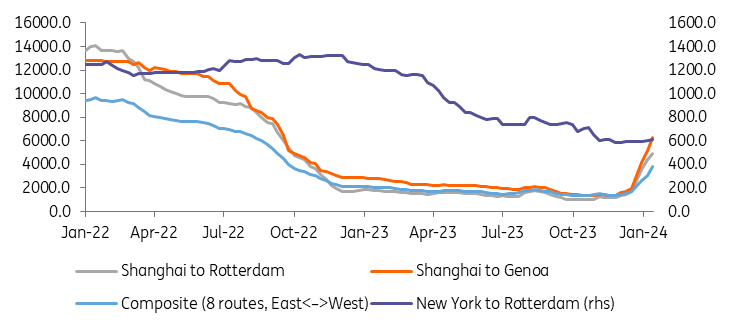

Container freight benchmark rate per 40 foot box (USD)

In our view, there has been one external factor where there has been a clear and marked deterioration, and that is the conflict over the Red Sea. Several shipping companies have already suspended shipments on the Red Sea routes due to the ongoing Houthi attacks, and in our latest note on Hungarian inflation, we’ve also discussed the effects of trade diversion.

The impact of the Red Sea conflict on supply chains is already being felt as Suzuki halted the production of the Vitara and S-Cross models at its Esztergom, Hungary plant between 15 and 22 January. The shutdown was caused by delays in the delivery of Japanese engines.

With shipping costs rising and supply chain disruptions already evident, we have identified the deterioration in external developments as the dominant factor that would affect the central bank's reaction function.

The comments of Deputy Governor Virág were deliberate

However, on 17 January Deputy Governor Virág spoke at the Euromoney conference in Vienna, and his remarks tilted our rate cut expectations from 75bp to 100bp. He conveyed the message that: “based on the information available, there were as many reasons for a 75bp cut as there were for a 100bp cut at the January meeting”.

We believe that these comments are more likely to indicate an increase in the pace of rate cuts, as they were made in the context of weighing the favourable developments in internal factors against unfavourable developments in external factors.

Our call

Against this backdrop, we see the National Bank of Hungary cutting the base rate by 100bp on 30 January. This could bring the key rate down to 9.75% after the rate-setting meeting, while we expect the Monetary Council to also cut both ends of the rate corridor by 100-100bp. There remains one major factor that poses a downside risk to our call and that is FX stability. We believe that if we were to see a further marked deterioration in EUR/HUF, this would encourage the central bank to remain more cautious and maintain the previous pace of 75bp of easing.

However, as the central bank will certainly remain in data-dependency mode, this does not mean that 100bp cuts will be automatic going forward. Rather, we expect the NBH to cautiously assess both internal and external developments and act accordingly on a meeting-by-meeting basis.

Our view on the pace of disinflation has not changed, as we expect disinflation to continue forcefully in the first quarter, but then to stall from the second quarter onwards as base effects reverse. This means that, on the basis of current information, we expect the pace of rate cuts to be reduced at the March meeting.

Our market views

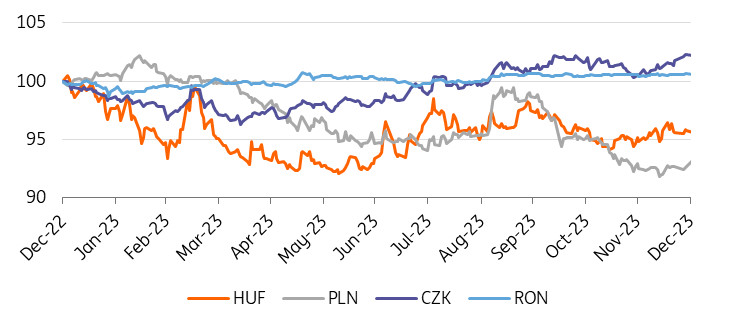

The Hungarian forint outperformed its CEE peers significantly in the first days of the year with lows below 378 EUR/HUF. However, we turned negative on HUF ahead of the December inflation reading due to significant divergence between FX and rates, which proved to be the right decision. HUF has since weakened by 2% flushing out the long positioning that the market had built in the last two months. Of course, EUR/HUF is one of the main, if not most important, factors influencing the speed of the NBH rate cut.

CEE currencies vs EUR (end 2022 = 100%)

For now, we think EUR/HUF levels of 386-387 are still comfortable for the central bank, however, we believe that above 390 the NBH would start to consider a more cautious approach with a hard stop above 395, i.e. only a 75bp rate cut.

We believe the gap between FX and rates that we pointed to earlier has been closed, but positioning and global risk-off sentiment affecting the entire CEE region could push EUR/HUF higher, which would raise the risk to our NBH call.

Hungarian yield curve

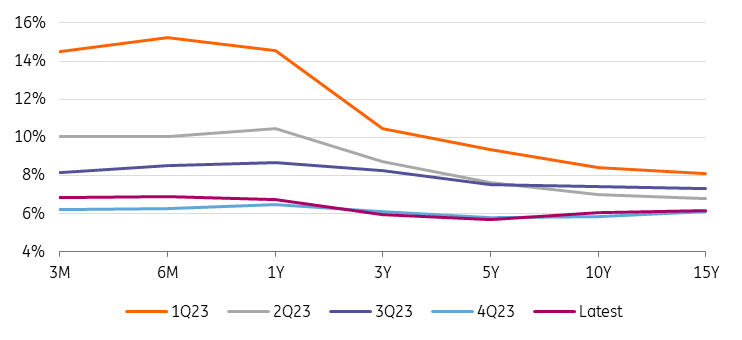

After a huge rally in rates in the first half of January, the market pressure eased and some bets on rate cuts were taken back. However, the curve continues to steepen with the 2s10s IRS within reach of zero, significantly outperforming CEE peers at the moment. However, if the NBH delivers a 100bp rate cut as we expect, the market will move back to where it was after the December inflation reading and comments from NBH officials. That's why we like receiving rates at these levels at the short end of the curve.

Looking even better in our view are Hungarian Government Bonds (HGBs) which have also sold off and are not trading far off the IRS curve. So with a very favourable inflation profile for the coming months and the central bank cutting rates, we see good value here once again. Additionally, the supply side of HGBs looks good, with a significant drop in net supply in particular, from last year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more