US: The higher you climb the greater the fall

- 1 September 2022

- United States

The Federal Reserve looks set to raise interest rates to 4% by year-end as officials signal a clear intent to deal with inflation. But with the global backdrop deteriorating and higher interest rates and a strong dollar set to weigh on an economy already experiencing a housing market downturn, we expect rate cuts will come next year

A recession that isn't a recession

The trade and inventory-induced technical recession in the first half of the year failed to dent the Federal Reserve’s appetite for hiking interest rates. After all, it wasn’t what we might term a “proper” recession given rising consumer spending and the fact that 3.3mn jobs were created between January and July.

Moreover, third-quarter GDP should bounce back nicely with trade and inventories moving much more favourably while the recent decline in gasoline prices has boosted consumer spending power. At the same time, core inflation is likely to rise back above 6% Year-on-Year on September 13th, while the upcoming August jobs employment should be decent given the surprise rise in job vacancies.

Fed pushes back against market pricing

Despite 225bp of interest rate hikes so far and the strong dollar, financial conditions have actually loosened in recent months. This came via tightening credit spreads and falling longer-dated yields as markets increasingly doubted the Fed’s intentions and predicted a pivot to rate cuts next year. The Fed fought back at the recent Jackson Hole symposium as officials ratcheted up the hawkishness, affirming that policy will be tightened further - and kept tight - to ensure inflation comes down.

The robustness of the Fed’s language seems to have changed perceptions somewhat and it now appears likely it will implement a third consecutive 75bp interest rate increase on September 21st. With more rate hikes at the November and December policy meetings we now see the Fed funds rate peaking at a 3.75-4% range by the end of the year.

Another key message from Chair Powell’s Jackson Hole speech was that the market shouldn’t get carried away with the pricing of rate cuts next year, which we suspect was part of the push intended to get longer-dated yields higher to tighten financial conditions to get inflation lower. Unfortunately, we have far less conviction than Powell that there won’t be the need for a loosening of policy in 2023.

Real recession risks are rising with inflation set to fall sharply

Residential investment is already a drag on growth due to the rapid downturn in the housing market while the global backdrop is deteriorating due to Europe’s energy crisis and China’s apparent slowdown. A strong dollar and higher-for-longer interest rates will only intensify the downside risks for growth in 2023 with the potential for what might be termed a “real recession” with rising unemployment and falling spending looking increasingly likely for late 2022/early 2023.

Inflation will stay high through the rest of this year. However, we remain hopeful that inflation can get back to 2% by the end of 2023. Housing and cars account for nearly half of the core CPI basket of goods and services, and the downturn in demand and rising supply will weigh on prices and be a major driver of lower CPI from April onwards. We also expect the weaker growth environment to result in a squeeze on corporate profit margins which will help depress inflationary pressures while a weaker growth environment translating into stagnant payrolls will take the heat out of wage inflation.

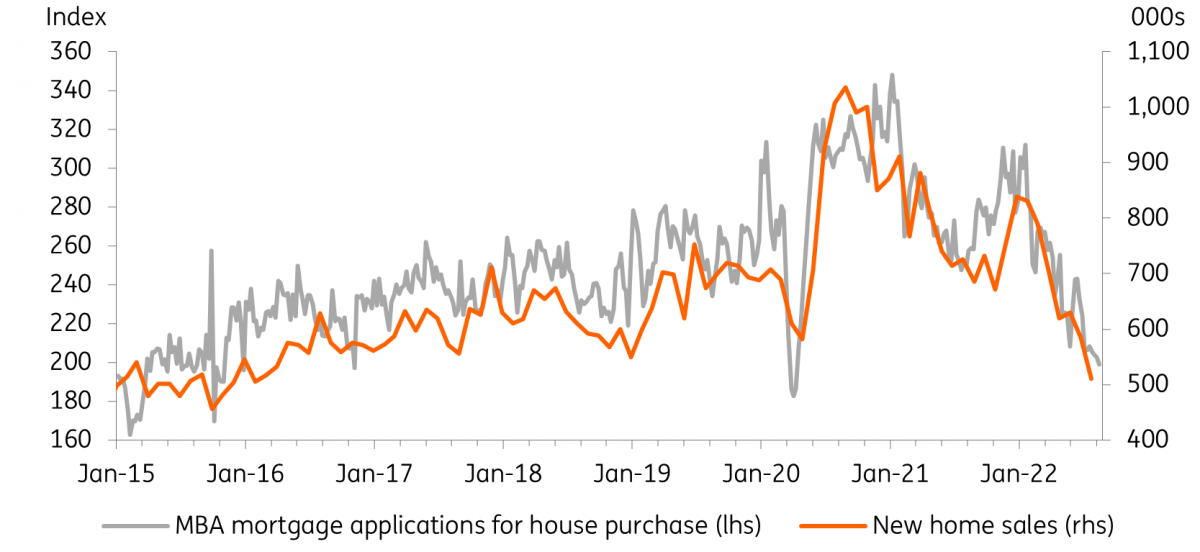

Housing demand and transactions continue to fall, prices will follow

Odds continue to favour 2023 rate cuts

Our base case for next year is a broad downturn in economic activity with the labour market losing jobs and inflation falling more quickly than the market and the Fed anticipate. This will open the door to rate cuts in summer 2023.

In order for the Fed not to cut rates, we need to see an environment where inflation stays stickier and the economy doesn’t experience as much of a slowdown as we expect. This most likely scenario would be via ongoing falls in gasoline prices (and perhaps food prices on top) spurring consumer demand with inflation pressures rising in other areas in what is a continually supply-constrained world. Additionally, while worker demand slows there continues to be worker shortages and the fight for talent remains strong, particularly in leisure and hospitality.

We would also probably need to see financial conditions remaining loose, which could come via the dollar weakening and longer dates' yield declining, dragging borrowing costs lower more broadly - basically, the market not believing the Fed. In the topsy turvy world of market behaviour, we would also need credit spreads to stay narrow with equities proving resilient. While not implausible, we do not see this as the most likely path ahead, hence our forecast for rate cuts.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly September: Recession’s coat of many colours

- This bundle contains 14 Articles