Monitoring Hungary: Uncertain times

- 10 March 2022

- Hungary

In our latest update, we reassess our Hungarian economic and market forecasts to reflect the impact of the war in Ukraine. We look at how economy policies are likely to respond to the prospect of weaker growth and surging inflation

Hungary: At a glance

- We’re downgrading our 2022 GDP growth forecast, despite the strong economic activity during the first one-and-a-half months.

- With yet another upside surprise in inflation, we see a double-digit print on the horizon and revise up our inflation projection.

- The latest official remarks by the National Bank of Hungary are suggesting a more prolonged tightening in 2022.

- External balances will deteriorate further as a new set of shortages are hitting the manufacturing sector alongside an energy price shock.

- The war has made the fiscal situation really complicated and it’s too early to choose between austerity or recalibration.

- Political forces are trying to use the war and sanctions to help their narratives ahead of the general election.

- The minor underperformance of the forint could be reverted in a risk-on environment, but until this arrives, we see high volatility.

- The chance for an inverted local yield curve is looking good for the coming months.

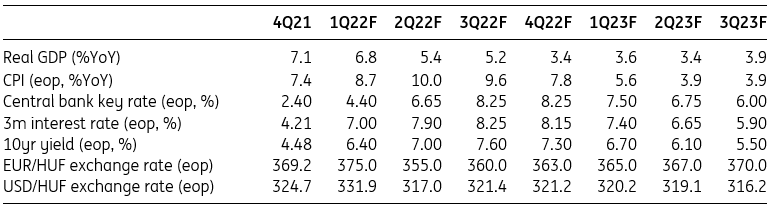

Quarterly forecasts

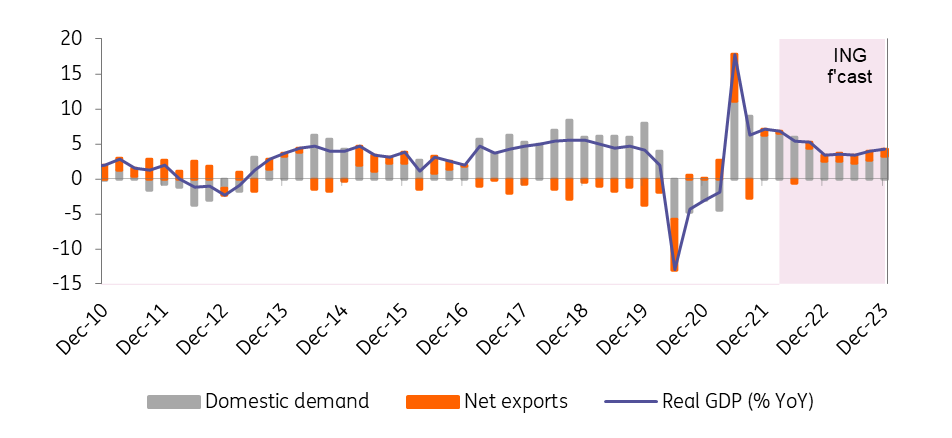

We are downgrading our GDP outlook

Hungary posted a 7.1% record-high GDP growth in 2021 with a quite balanced growth structure despite the several challenges (e.g., Covid waves, shortages in several aspects). After the strong finish to the year, 2022 started out well. Until mid-February the economy was on track for a 7.5-8.5% year-on-year GDP growth in the first quarter. Unfortunately, this rosy outlook is now shattered with the war in Ukraine. The negative channels are mainly related to confidence, trade, supply and price shocks. We cut our 2022 GDP forecast by 1ppt to 5.2%, but this outlook could turn to a quite optimistic one fairly quickly.

Real GDP (% YoY) and contributions (ppt)

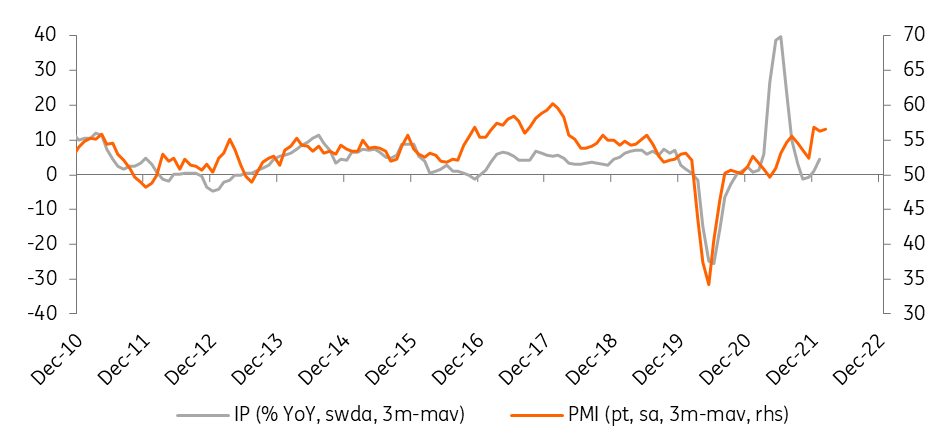

Industry starts 2022 with a strong performance

The sector's growth in January exceeded expectations. Production jumped by 1.9% on a monthly basis, translating into an 8.9% year-on-year growth. Car production played a huge role in the good January performance, as it had risen again after a six-month decline. The strong start will now become unsustainable because of the war. With the closure of Ukrainian plants, car makers (and probably others as well) across Europe are once again facing a shortage of parts. Sanctions could mean shortages of metal commodities as well. Industry is clearly facing another difficult year.

Industrial production (IP) and Purchasing Manager Index (PMI)

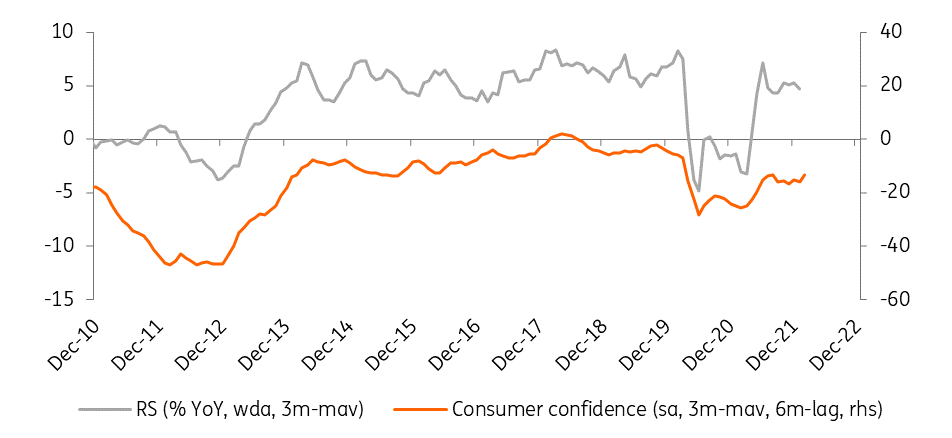

Retail to have some positive impulses

The growth rate of retail sales slowed somewhat in January, as the volume of turnover increased by 4.1% year-on-year. Meanwhile, it showed a 0.1% decline on a monthly basis. The moderated January retail performance can be attributed to both weaker-than-usual food and non-food sales. Meanwhile, turnover at fuel retailers grew dynamically. The current humanitarian catastrophe at Hungary’s Eastern border may have some positive implications on retail sales with the government and households buying aid packages. The February huge one-off fiscal transfers (personal income tax refund for families, 13-month pension, six-month bonus for armed forces) will also boost consumption.

Retail sales and consumer confidence

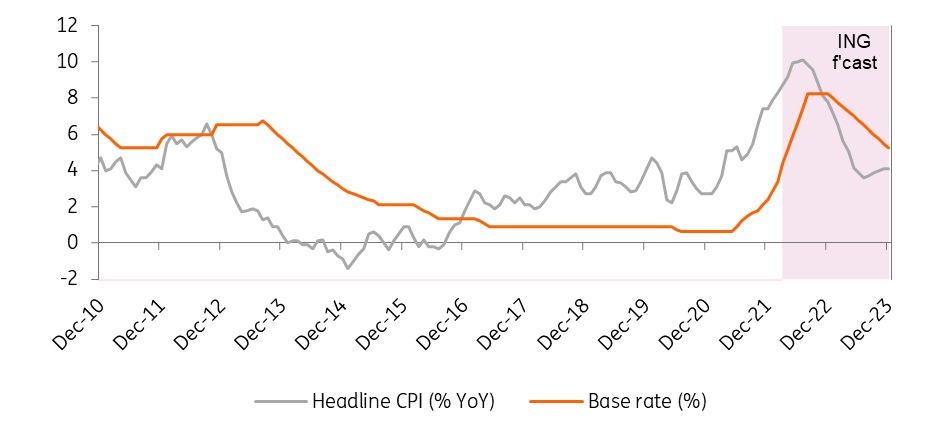

Double-digit inflation on the horizon

By now we shouldn't be surprised by Hungary's higher-than-expected inflation readings. The 8.3% year-on-year February data is the highest figure since August 2007. Core inflation moved above 8% as well, matching the highs of 2001. The uptick in the second month of 2022 means that the government’s anti-inflationary measures weren’t able to stop the general price increase. The main drivers of the acceleration were food, services and durables. We see a significant jump in inflation in May-June: probably above 10% year-on-year, as the price caps will expire. We see 8.0-9.5% average inflation with further upside risks in 2022.

Inflation and policy rate

Central bank tightening continues

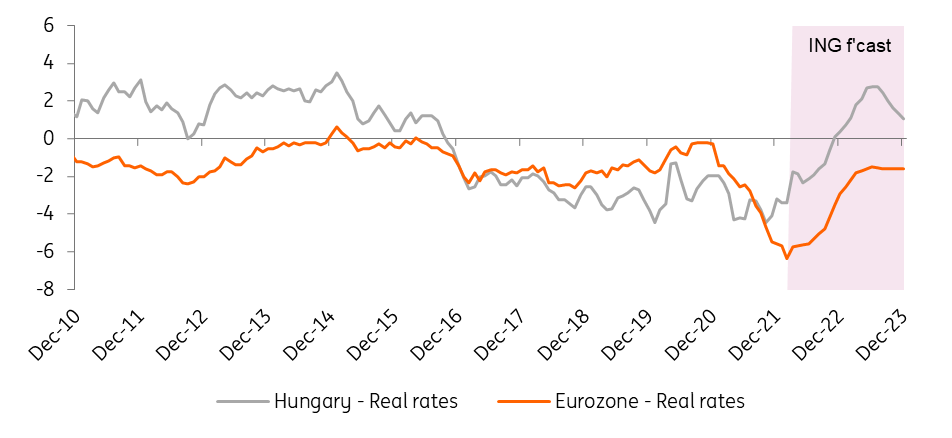

We expect the interest rate cycle to continue in the coming weeks (1-week deposit rate hikes) and months (raising the 1-week deposit, the base rate and interest rate corridor). The National Bank of Hungary is eager to fight against inflation and maintain the stability of financial markets and it is ready to use all its tools. We expect the effective interest rate to rise to as much as 8.25% by the middle of this year. But this can change both upwards and downwards by the course of the Ukrainian war. We consider it less and less likely that inflation will return to the 3% target in 2023 with any realistic assumption of central bank tightening.

Real rates (%)

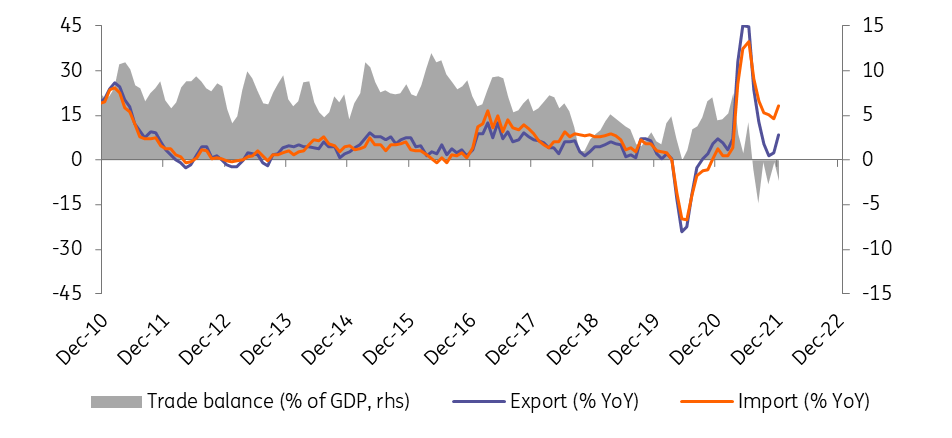

External balances to remain in deficit

The trade balance in 2021 came in at a €1.9tr surplus, showing a €3.7tr drop compared to 2020. The value of imports grew by 8.3% on strong domestic demand and exports rose by 7.8% despite supply shortages. Preliminary current account data showed improvement in the fourth quarter, but the 2021 deficit was still around 3% of GDP. The war and the sanctions will limit exports, while the booming energy prices will make commodity imports more expensive. In this regard, the trade and current account balances could show further deterioration in 2022.

Trade balance (3-month moving average)

Austerity or recalibration in fiscal policy

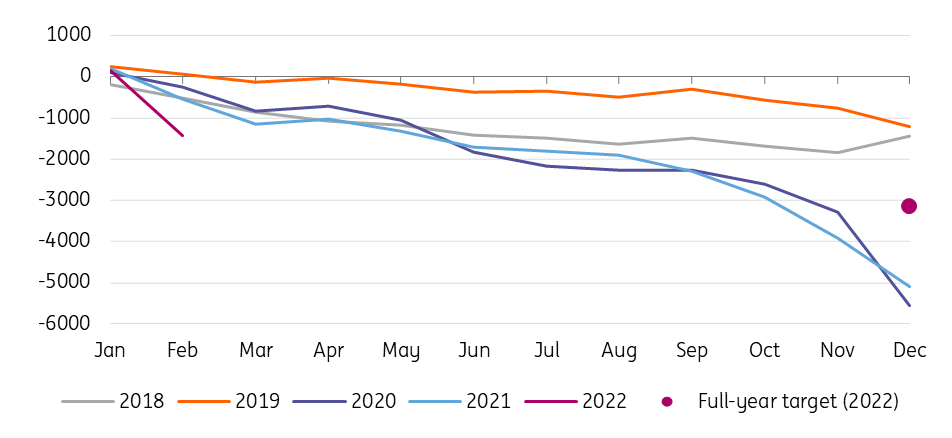

The Hungarian budget posted a HUF1,585bn deficit in February, the second biggest monthly deficit ever. With the small surplus in January, the year-to-date deficit accumulation is at HUF1,434bn. This equals to 45.5% of the full-year cash-flow deficit target. The extreme shortfall was planned and was driven mainly by one-off transfers to households (PIT refund, pension, bonuses, etc). In a vacuum, this data would not concern us. What makes the situation delicate is the war in Ukraine, which could have significant implications on the 2022 fiscal targets. In this volatile and fragile situation, we don’t expect the government to rush into any decision, whether it is an austerity measure or a recalibration of the deficit and debt targets – especially not with the general election looming (3 April).

Budget performance (year-to-date, HUFbn)

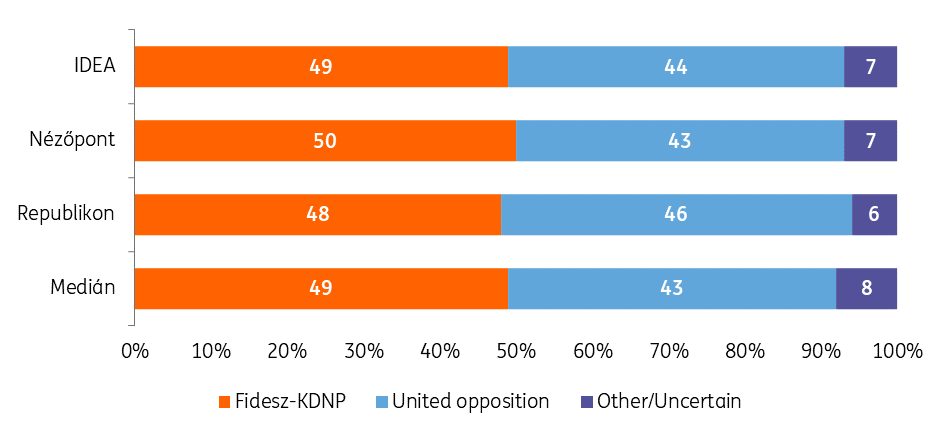

Voters favour the ruling power in a crisis

The pre-election landscape hasn’t changed much in February based on the latest opinion polls. The recent governing power Fidesz-KDNP still has a roughly 5-point lead (on average) versus the united opposition. Only one survey was conducted partially during the war. According to Medián’s survey published in early March, the advantage of the ruling parties was only 4 points despite the big transfers (PIT refund, 13-month pension, bonuses) in February. However, after the invasion this gap increased to 12 points. So, it seems true, that in a crisis, the support is growing behind the actual leader who is in a decision-making position. This may have led to the jump in the proportion of Fidesz-KDNP voters.

Party preference among active voters as of February

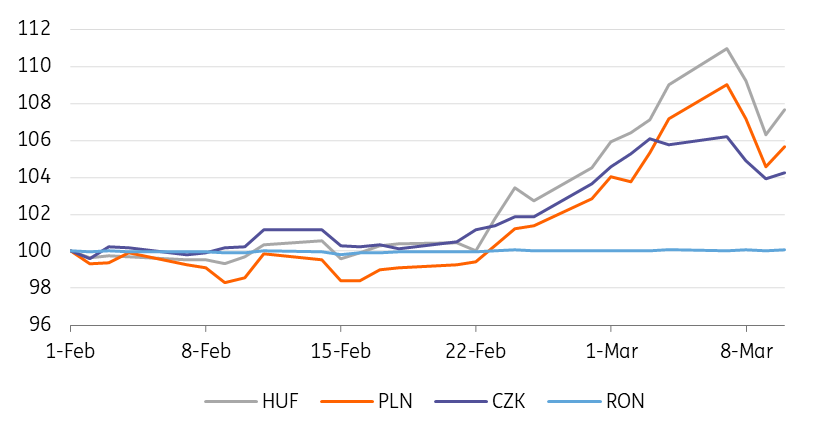

FX: In HUF we trust

Investors throw everything but the kitchen sink into hard currency in these days. HUF was not able to resist the mass exodus from risk assets, reaching a new record at 400 vs EUR. The verbal interventions and the total 125bp 1-week deposit rate hikes by the National Bank of Hungary in early March showed that the central bank is ready to fight against pro-inflationary pressures. We see more rate hikes to come, but we don’t see real interest rates reaching positive territory in the next couple of quarters, despite our 8.25% terminal rate forecast.

We see EUR/HUF hovering around 375 in the coming weeks. As soon as the risk sentiment will improve, new short positions (HUF600bn during early March) will be unwound, thus we see a chance for EUR/HUF moving back to the 355-360 range quite rapidly. The slight underperformance of the HUF since the outbreak of the war is reversible, in our view. This phenomenon is related to Hungary’s unique exposure.

Hungary is having the highest debt in our region and it is more vulnerable to external demand shocks. Although the latter could be true for Czechia, it can be seen as a developed economy with its 93% GDP/capita level versus EU average in PPP terms. Hungary is only at 74%. Moreover, Hungary’s external trade ties (especially its energy dependency) are a bit deeper with Russia. Last but not least, Hungary’s sovereign credit rating is lower than its regional peers, expect for Romania.

FX performance vs EUR (1 Feb = 100%)

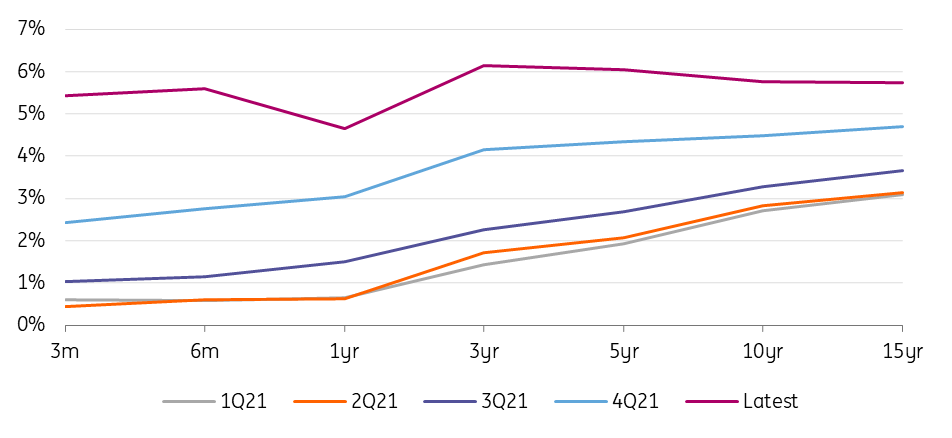

Inverted local yield curve is coming

The central bank is ready to fight against inflation and for financial stability. With further upside risks in inflation, we see further rate hikes both on a weekly basis in the 1-week deposit rate and on a monthly basis in the base rate. The convergence of the two could come at 8.25% in August. In this respect, we expect further flattening in the Hungarian yield curve. The chance for an inverted curve looks real in 2H22 with a decelerating inflation and some normalisation in risk taking.

Hungarian sovereign curve

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more