Macro concerns vs commodity supply constraints

- 6 October 2022

- Commodities, Food & Agri Energy

Commodity markets have come under pressure due to a strengthening US dollar and a raft of central banks hiking interest rates recently. This has clouded the macro outlook. However, the supply picture for a number of commodities remains fragile

The OPEC+ put

Oil prices came under pressure in September, with ICE Brent falling by almost 9% over the month and trading to the lowest levels since January. US dollar strength and central bank tightening have weighed on prices and clouded the demand outlook.

From a supply perspective, the oil market has been in a more comfortable position. Russian oil supply has held up better than most were expecting due to China and India stepping in to buy large volumes of discounted Russian crude oil. The demand picture has also been weaker than expected.

However, we believe there is a good floor for the market not too far below current levels. Firstly, the EU ban on Russian oil comes into force on 5 December, followed by a refined products ban on 5 February. This should eventually lead to a decline in Russian supply, as it is unlikely that China and India would be able to absorb significantly more Russian oil.

Secondly, US Strategic Petroleum Reserve releases are set to end later this year. If not extended, we could start to see large drawdowns in US commercial inventories, which are very visible to the market and could provide more support.

Potential OPEC+ intervention should also provide a good floor to the market. Already this week, OPEC+ announced a 2MMbbls/d supply cut through until the end of 2023. However, it is important to remember that given OPEC+ is cutting output from target production levels, the actual cut will be smaller given that most OPEC+ members are already producing well below their target levels. Our numbers suggest that the group’s paper cut of 2MMbbls/d will work out to an actual cut of around 1.1MMbbls/d.

Price caps and price forecasts

As for the proposed G7 price cap on Russian oil, the EU now appears to have agreed on the mechanism. However, once implemented, there is still plenty of uncertainty over whether it will have the desired effect of keeping Russian oil flowing and limiting Russian oil revenues. Without the participation of big buyers, such as China and India, it is difficult to see the price cap being very successful. In addition, there is always the risk that Russia reduces output in response to the price cap.

We currently expect Brent to trade largely within the US$90 area for the remainder of this year and into the first half of 2023, before strengthening over the second half of 2023. However, given the large supply cut recently announced by OPEC+, the global market will likely be in deficit through the whole of 2023, suggesting that there is upside to our current forecasts.

Even tighter times ahead for European gas

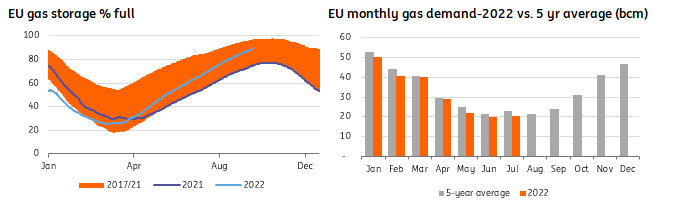

European natural gas prices have come off their highs in August, falling more than 40% from the recent peak. Comfortable inventory levels have helped, with storage 89% full already. The EU has also managed to build storage at a quicker pace than originally planned. In addition, intervention from the EU is likely to leave some market participants on the sidelines, given the uncertainty over how policy may evolve.

It also appears that the EU is moving towards a price cap on natural gas in some shape or form. Whilst this will offer some relief to consumers, it does not solve the fundamental issue of a tight market for the upcoming winter. We need to see demand destruction in order to balance the market through the high demand months of the winter, but capping prices will do little to ensure this. It will be difficult to get through this period unless we see demand falling aggressively, and this becomes more of a challenge when we see seasonally higher demand. The latest numbers from Eurostat show that EU gas consumption was 11% below the five-year average over July, falling short of the 15% reduction the EU is targeting. In recent weeks, consumption has also come under further pressure as a result of industrial shutdowns.

EU gas storage above target levels while demand comes under pressure

It is looking increasingly likely that the trend for Russian gas flows is lower in the months ahead. At the moment, the EU is only receiving Russian pipeline natural gas via Ukraine and through TurkStream, and there is the risk that we will see these flows decline as well. Recently, Gazprom warned that Russia could sanction Ukraine’s Naftogaz due to ongoing arbitration. This would mean that Gazprom would be unable to pay transit fees to Naftogaz, which puts this supply at risk. At the moment, volumes transiting Ukraine are in the region of 40mcm/day. Meanwhile, total daily Russian flows via pipeline to the EU are down in the region of 75-80% year-on-year.

The EU should be able to get through the upcoming winter if demand declines by 15% from the five-year average between now and the end of March. The bigger concern, however, will be for the following winter in 2023/24. Earlier this year, we saw some decent flows of Russian gas, which helped with rebuilding inventory. Next year, Russian flows are likely to be minimal, which means that the EU may build inventories at a slower pace. We therefore expect to go into winter in 2023/24 with very tight inventories, which suggests the risk of even higher prices over this period.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING’s October Monthly: bracing for a tough winter

- This bundle contains 14 Articles