James Smith: Why we disagree with markets on the Bank of England

- 1 June 2023

- United Kingdom

Investors think Bank Rate could rise another 100 basis points following some shock inflation data. But there are also broader signs that wage and price pressures are slowly easing, which suggests one or perhaps two more rate hikes will prove sufficient

Market expectations for the Bank of England reminiscent of last year's crisis

UK investors would be forgiven for feeling a sense of déjà vu over recent days. An unexpectedly high inflation reading helped send market expectations for the Bank of England into territory last seen in October and November in the aftermath of the fateful ‘mini budget’. That remains true whether you look at the peak rate being priced (5.5%) or the spread between expected policy rates in the US and UK in 6-12 months.

That equates to four more rate hikes, and incidentally, these are the same levels that prompted BoE policymakers to offer some rare pushback against market expectations at last November's meeting.

All of this seems excessive – and the BoE itself has repeatedly stated that much of the impact of past rate hikes is still to hit the economy. That being said, the Bank may be more reluctant than it was last November to push back against these lofty expectations. Given the tendency of recent inflation figures to come in hot, policymakers won't want to pre-commit. The current ‘data-dependent’ approach points to another hike in June – and perhaps one more in August.

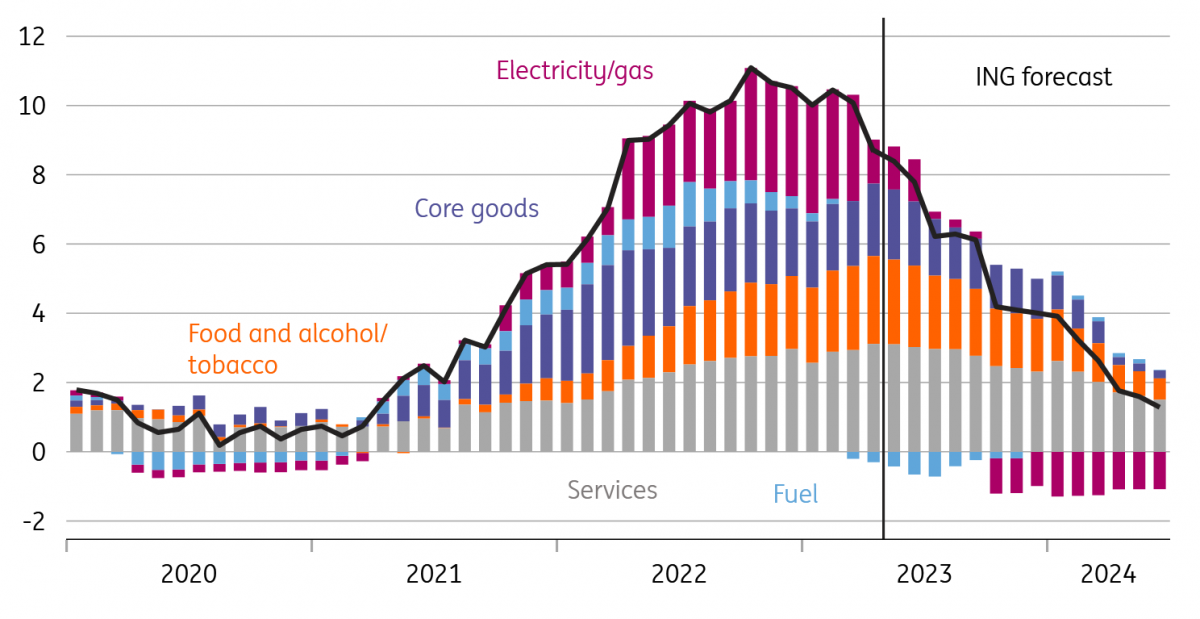

Lower gas prices should see inflation fall to 4% area by year-end

Dig deeper and inflation doesn't look as bad - but we could be wrong

It’s worth emphasising that beneath the surface of the recent shock CPI numbers, the story is not quite as bad as it looks. Recent strength is partly down to goods categories, like alcohol and vehicles, and these are trends that are unlikely to last. Services inflation, which is the Bank's main focus, would have been roughly in line with expectations had it not been for a highly unusual month-on-month spike in rents.

Broader measures of inflation, including the BoE’s survey of CFOs, point to lower inflation and wage expectations over the coming months. The latest jobs data points to cooling hiring demand and more muted pay pressure.

In short, we expect rates to peak below where markets expect and we think that rate cuts (when they eventually materialise in mid-2024) could be deeper, too. Investors expect Bank Rate to settle around 4% in three years’ time, which seems high.

Where our view could start to fall apart is if services inflation fails to come down over the rest of this year. We think lower gas prices will alleviate a key source of price pressure, particularly in the hospitality sector, which has accounted for much of the rise in services inflation. There’s a clear risk that firms bank some of these lower costs to rebuild margins, and that’s essentially the view of the BoE hawks right now. In other words, what went up pretty quickly could be much slower to come down.

Worker shortages are also undoubtedly still a big issue for employers, and that looks like a structural rather than a cyclical challenge. We can’t rule out a rebound higher in wage growth. Though not our base case, in this scenario markets may well be right that interest rates end up rising above 5% and stay very restrictive for longer.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: We’re only human

- This bundle contains 9 Articles