India’s FY2020 budget targets lower deficit, really

- 5 July 2019

- India

Finance minister Nirmala Sitharaman may have scored some points for fiscal consolidation with a lower deficit target of 3.3% of GDP. Whether her maiden budget revives the economy to 7% of GDP growth in the current financial year remains to be seen

| 3.3% |

FY2020 fiscal deficit target |

| Lower than expected | |

The final Budget for FY2020

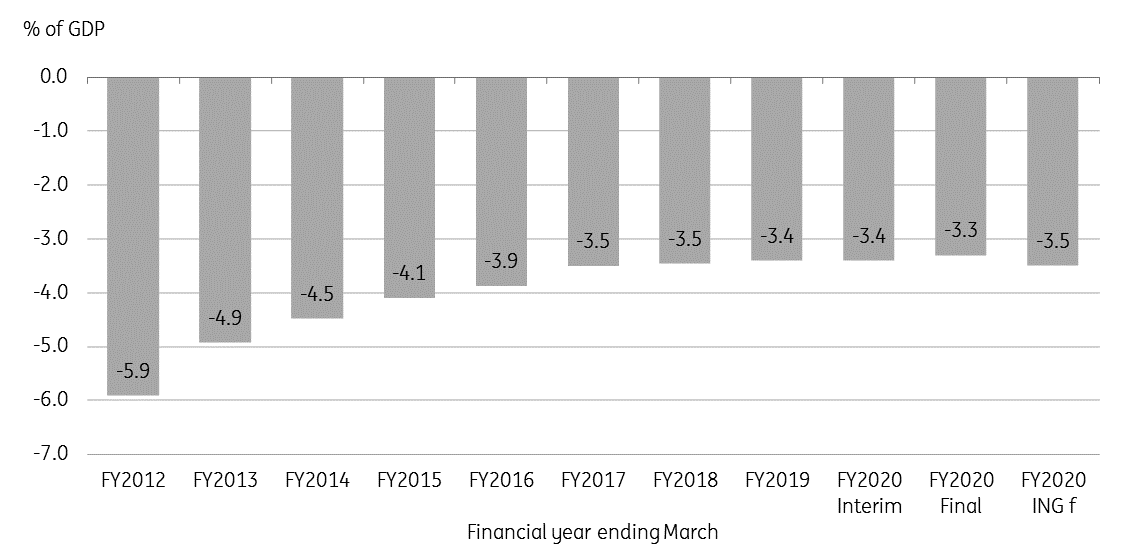

To the surprise of many, new Finance Minister Nirmala Sitharaman’s maiden budget for FY2020 (ending on 31 March 2020) aims for a lower fiscal deficit equivalent to 3.3% of GDP from 3.4% in the interim budget. With persistent downside growth risk likely depressing government revenue and an infrastructure investment drive entailing more spending, the risk to the deficit target will be tilted on the upside.

We continue to expect another overshoot; we forecast the fiscal deficit at 3.5% of GDP in the current financial year, which rests on our view of much slower, 6.6% GDP growth than the government’s 7% projection.

Derailed fiscal consolidation

A $5 trillion economy in five years

Besides its prevailing “Make in India” theme, the government is aiming to make India a $5 trillion economy by 2024, a near-doubling from $2.7 trillion currently. This seems to be a feasible goal on the assumption of steady GDP growth of about 7% and inflation of 4% annually.

However, the long-term potential of 7-8% growth hinges on rapid infrastructure development. On the face of it, the budget appears to be heavy on words and light on concrete action on this front, while the long-term nature of infrastructure projects also makes them prone to frequent alterations, cost overruns, and uncertainty. Moreover, boosting infrastructure investment spending in the future could be a difficult proposition if countered by the drive to improve public finances and cut down the deficit, which will be an ongoing necessity to build global investor confidence, as the government eyes the international debt market for deficit financing (see below).

Among other things, the measures to attract more foreign investment (both direct and portfolio), public-private partnership (PPP) in infrastructure projects, and reduction of corporate taxes are some of the better initiatives.

Tapping international market for funds

In an initiative aimed at broadening the debt market, the government plans to turn to the international market to meet its funding needs. Given the low level of external debt, running around 20% of GDP, the move to broaden deficit financing to overseas debt markets may not be an issue.

The success, however, depends on the kind of investor response the government receives on this front. Considering the significant growth potential of the Indian economy ahead, this could be positive, once the cyclical slowdown currently underway has passed. Moreover, investors will also be looking at the government's record of fiscal management. Weak growth feeding into the risk of sustained deficit overruns won't go down positively in the international market as this also adds to the risk of a sovereign rating downgrade - a risk that hasn't even been discounted currently with a persistent twin-deficit (fiscal and current account deficit).

For now though, this move should ease some of the supply overhangs on the domestic bond market, and thus reduce upward pressure on yields. Meanwhile, the government has maintained its INR 7.1 trillion local borrowing target for this year.

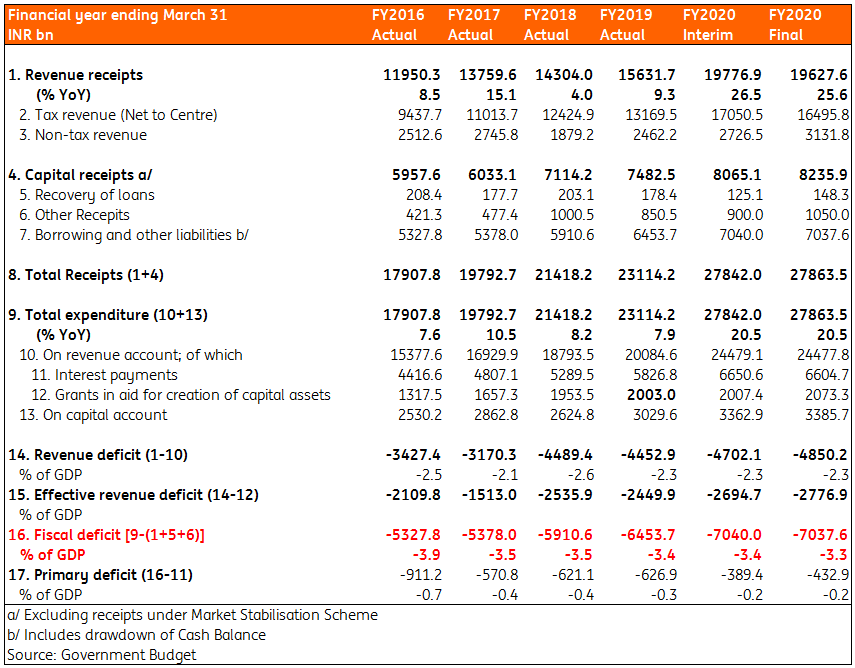

Budget in figures

Some of the budget initiatives

- Virtuous investment cycle with heavy infrastructure investment in national and state highways and inland waterways to facilitate the growth of internal trade. Boosting investment in suburban railroads with PPP initiatives.

- Boosting rural infrastructure with easier availability of electricity and water to farmers. Zero-budget farming (no credit, no chemical fertilizer) farming to double farmers’ income.

- More support to MSMEs (micro, small, and medium enterprises) with easier credit availability. Pension plans for small businesses.

- Measures to attract foreign direct investment (FDI). Opening of aviation, insurance and media sectors to foreign investors. Labour market reforms enabling easier access for foreigners.

- Simplifying KYC (know your customer) guidelines for foreign portfolio investors (FPI) and allowing ‘AA’ rated bonds as investment collateral.

- INR 700 billion recapitalisation for state-owned banks. More powers to the Reserve Bank of India to regulate the non-bank financial sector, including housing finance companies.

- Increase in public stockholding limit for companies up to 35% from 25%. Rise in the target of public sector asset sales by 17% to INR 1.05 trillion in FY2020 from the interim budget. Proposed reduction in government shareholding in state-owned companies below 51%.

- Reduction of the corporate tax rate for turnover of up to INR 4 billion to 25% from 30%. Electronics assessment of personal income tax and surcharges of up to 7% for high-income earners.

- Hike in customs duty on gold and precious items and excise duty on petrol and diesel. Discouragement of cash economy with 2% tax deduction at source on over INR 10 million cash withdrawal per year.

- Tapping international market for sovereign borrowing. No change to the INR 7.1 trillion gross (4.73 trillion net) domestic borrowing target for FY2020.

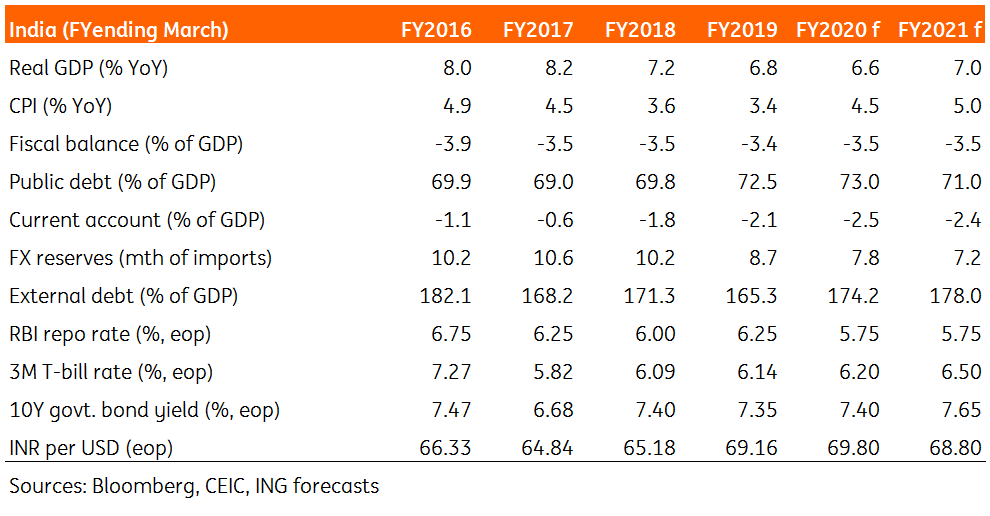

India: Key economic indicators and ING forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

What’s happening in Australia and the rest of the world?

- This bundle contains 7 Articles