Fuelling a net zero economy with synthetic fuels: eight lessons to get it right

Corporate leaders are looking at how synthetic fuels can set their companies on a path to net zero emissions. This is far from easy as they are faced with economic and environmental trade-offs. That’s why we have presented eight insights to help them get it right. Hydrogen's exposure to the energy crisis and the 'greenness' of hydrogen are big challenges

Eight insights for corporate decision-makers

Despite all the buzz around synthetic fuels and government support for it (for example in the US and the Netherlands) the economics are far from easy. High gas and power prices have worsened the business case lately, especially in continental Europe. At the same time, synthetic fuels are positioned as a way to replace Europe’s gas and oil dependency in the future and as a means to radically reduce emissions.

In this article, we analyse the role of synthetic fuels in a net zero economy and unravel the economic value drivers of the hydrogen business case, which is the most promising and best-known fuel. We take a European perspective. In doing so, we present eight key insights for corporate decision-makers in energy-intensive companies that can help them build the case for synthetic fuels. But first things first; what are synthetic fuels?

What are synthetic fuels?

Synthetic fuels are liquid fuels that have the same properties as fossil fuels but are produced artificially in a non-fossil way. Synthetic fuels are entirely produced in a factory or chemical plant environment, rather than extracted from the earth and therefore, ideally, do not involve oil, coal or gas mining.

So while hydrogen can be produced from natural gas (which is extracted), it can also be produced by splitting water with an electrical current (which is a chemical process called electrolysis). Both types of hydrogen share the same features and applications, but the one that splits water into hydrogen and oxygen is entirely free of fossil fuels if it is produced fully with renewable power. If so, its use does not create carbon emissions.

Synthetic fuels can also be made from syngas, which is a combination of carbon oxide (CO) and hydrogen (H₂). Reacting these two substances under specific conditions (temperature, pressure and catalyst) results in synthetic fuels such as gasoline, diesel, gas, or even kerosene.

Electrolysis and syngas reactions are both chemical processes that yield synthetically produced fuels instead of fossil fuels that are extracted from the earth.

Synthetic fuels offer a key pathway to a net zero economy

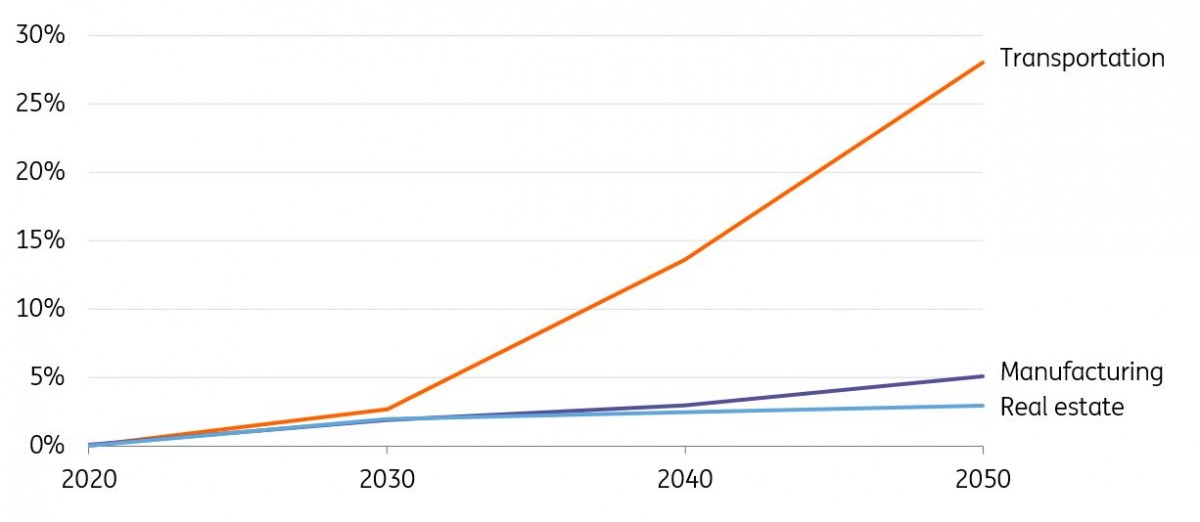

Corporate decision-makers around the world have been encouraged by government pledges to reduce greenhouse gas emissions to net zero by mid-century and the financial incentives that come with it (think of hydrogen subsidies and infrastructure). According to the International Energy Agency (IEA) around 70% of global carbon emissions are now covered by net zero pledges. As a consequence, the use of synthetic fuel needs to increase in energy-intensive sectors towards 2050, particularly in transportation.

Synthetic fuels are likely to grow towards 2050, particularly in transportation

Share of synthetic fuels in the global sector energy mix in the IEA Net Zero Scenario

According to the IEA, synthetic fuels are not the holy grail to decarbonising energy-intensive sectors in the sense that they alone will fully substitute fossil fuels and reduce emissions. Other technologies such as electrification, bioenergy and carbon capture and storage also play an important role. But, synthetic fuels certainly add to the solution, especially in transportation sectors like aviation and shipping. They can become one of the many building blocks of a net zero economy, provided that corporate leaders, politicians and scientists get the business case and technologies right. That’s why this article unravels the economic drivers of the business case.

Synthetic fuels provide corporate decision-makers with a tool to go beyond carbon offsetting

The climate strategies of carbon-intensive companies often rely heavily on carbon offsetting strategies. But these come with many drawbacks and enable companies to continue to emit vast amounts of emissions as long as they pay someone else around the globe to make up for it, for example, by planting trees or preserving existing forests.

A growing number of corporate leaders are now fundamentally rethinking their climate strategies and aiming to become net zero emitters by 2050, according to the Science Based Target Initiative. The key is to radically reduce the company’s carbon emissions, even if this requires a fundamental change to the way they do business.

Synthetic fuels are an example of fundamental change, as these can be used in many sectors without creating local emissions. For example, only water vapour is emitted by burning hydrogen in ships, aeroplanes, trucks or cars. The same applies to burning hydrogen in factories and houses to generate heat. So as long as the production of hydrogen is low in emissions (think of green hydrogen production with electricity from wind, solar, hydro or nuclear plants), the lifecycle emissions of hydrogen are much lower than fossil fuels. Synthetic fuels, like hydrogen, have gained a cult status among many industry leaders and politicians as a result.

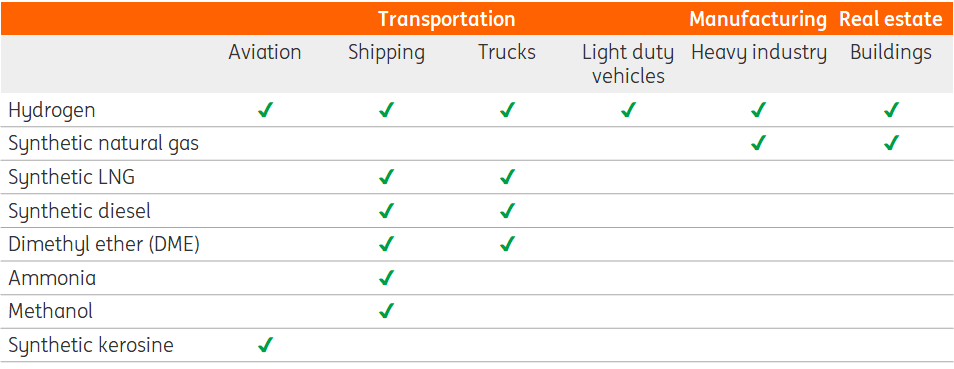

In the remainder of this article, we focus on hydrogen as it is the best-known synthetic fuel and can be applied in many sectors.

Hydrogen is the best known synthetic fuel and can be used in many sectors

Potential use of different synthetic fuels in sectors

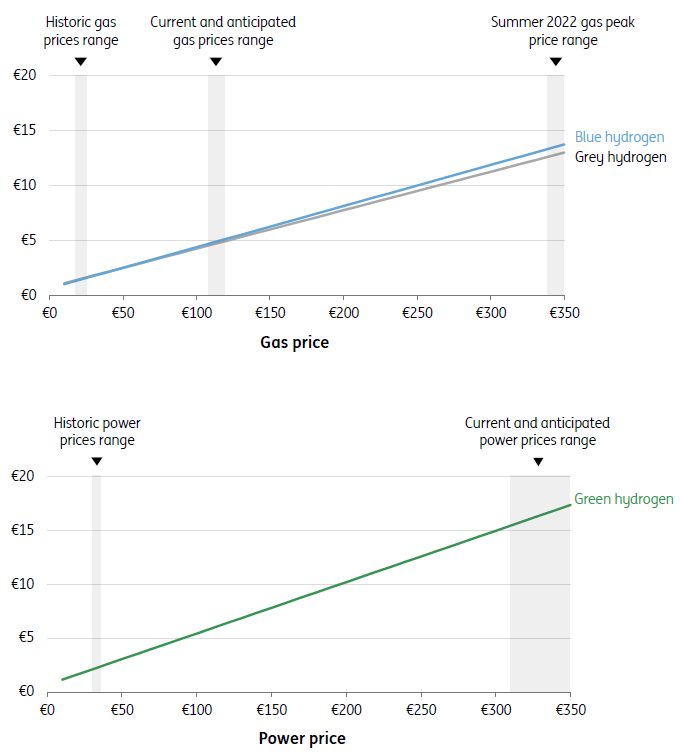

Hydrogen production has not been immune to the energy crisis

Hydrogen production comes in three forms with a colour attached to each of one. Grey hydrogen is produced from natural gas and the emissions are not captured and stored. Hence the gas and carbon price are the main value drivers of the business case. That is also the case for blue hydrogen where most emissions are captured and stored. As a result, the business case of blue hydrogen is less impacted by the carbon price. Finally, green hydrogen is made with electrolysers that run on electricity. Therefore, the power price is the major value driver of the business case for green hydrogen.

To sum up, hydrogen is made with natural gas or electricity where prices change over time, particularly during an energy crisis such as the one seen in Europe this year.

Cost of hydrogen production depends on gas and power prices

Indicative unsubsidised cost of hydrogen in Europe per kilogram at a carbon price of 75 €/ton

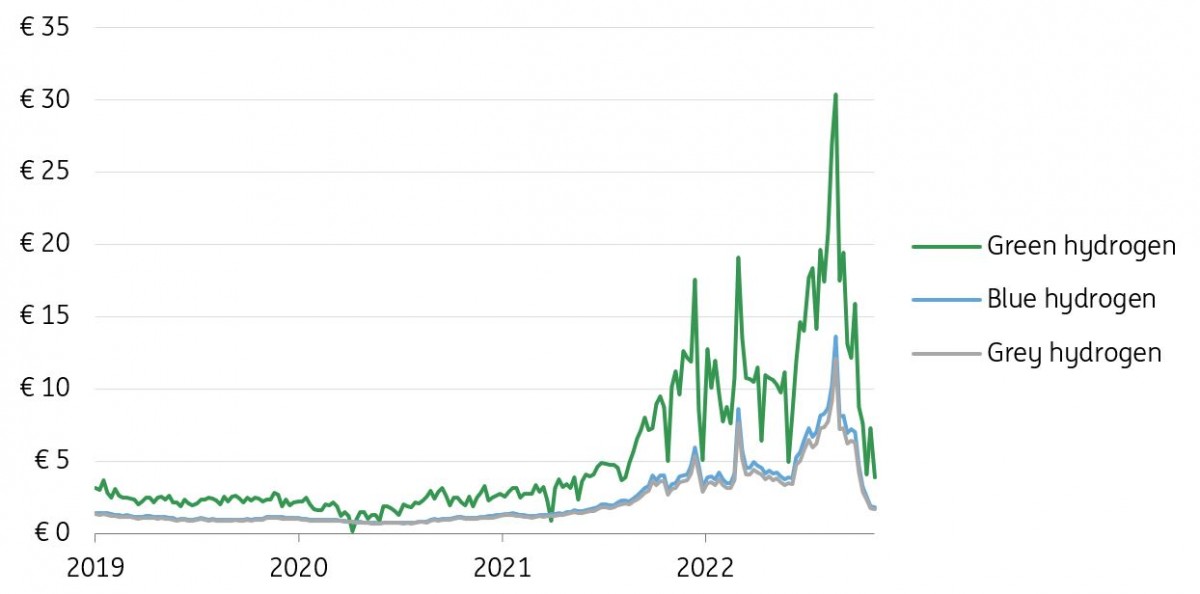

The energy crisis has had a severe impact on hydrogen production costs through higher natural gas and power prices, particularly in Europe. In the Netherlands and Germany for example, the cost of hydrogen production has skyrocketed as gas prices went from an average 20 €/MWh in the years before the crisis to a peak of 350 €/MWh this summer. Power prices increased from 40 €/MWh to a peak of 700 €/MWh in the Netherlands and even 1,000 €/MWh in France. The cost to produce hydrogen reached record levels on the back of skyrocketing energy prices and hydrogen production was scaled down as a result. For example, Yara produces hydrogen out of natural gas for its ammonia and fertiliser production and curtailed production at its Ferrara (Italy) and Le Havre (France) plants.

Energy crisis pushes hydrogen production costs higher

Indicative cost of hydrogen production in Europe in €/kg at realised TTF-gas and APX-power prices

Both gas and power prices have fallen rapidly recently. Ample LNG supply could not be stored as gas storage facilities in Europe are almost completely filled. On the demand side, the heating season has not kicked in as weather temperatures have been unusually high for this time in the season. This combination of lower-than-expected demand and ample supply caused gas process to fall below 50 €/MWh and power prices below 100 €/MWh. Still, the market expects this to be short-lived. The futures markets indicate gas prices of around 125 €/MWh throughout the winter and power prices of over 300 €/MWh depending on the month of delivery. Hydrogen production costs will move again towards 5-6 €/kg for grey and blue hydrogen and around 15 €/kg for green hydrogen if these expectations materialise.

Although hydrogen is often touted as a solution to becoming less dependent on fossil fuels, the economics are still driven by the gas market. This also holds for green hydrogen as gas is likely to remain the price-setting technology in many power markets in the coming years.

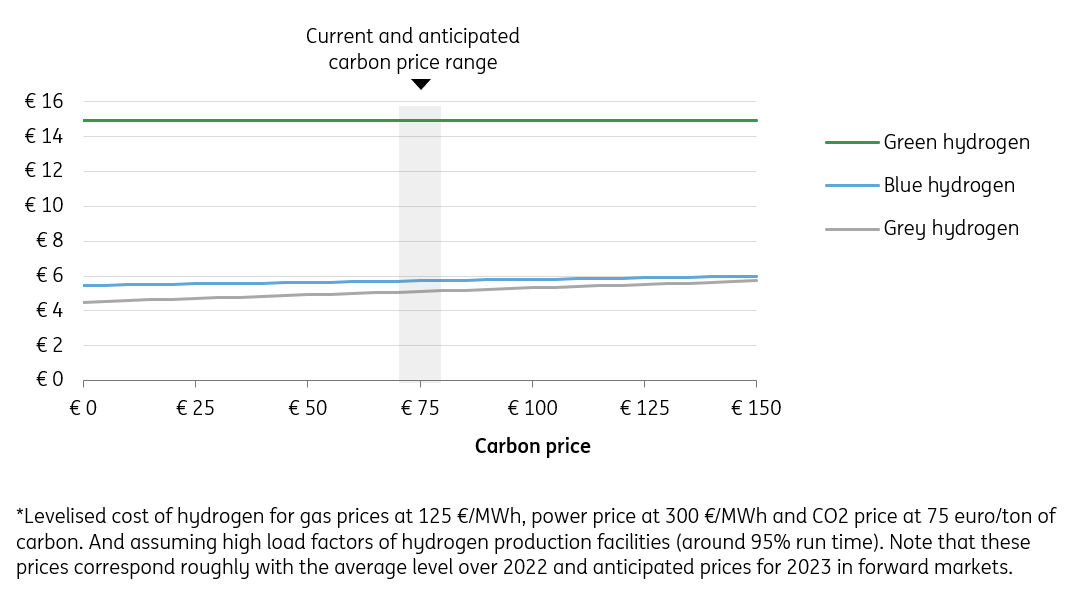

At current carbon prices green hydrogen is not cost competitive with grey and blue hydrogen

In Europe, carbon prices are the main mechanism that drives the environmental competitiveness of the three types of hydrogen. Before the energy crisis, blue hydrogen in general was cost competitive with grey hydrogen at a carbon price above 60 euro per ton CO2. That provided hydrogen producers with an incentive to apply carbon capture and storage (CCS) to hydrogen production and it was expected that they would switch from grey to blue hydrogen production once CCS infrastructure was in place. That no longer holds for current gas and power prices. In fact, grey hydrogen is currently the cheapest form of hydrogen at any carbon price below 150 euro per ton CO2. And green hydrogen is almost three times as expensive as grey and blue hydrogen at the current carbon price and state of technology.

Despite initiatives to strengthen the European carbon market, fears of a recession are likely to continue to weigh on carbon prices. With high energy prices, the carbon market won’t offer a decisive push towards less polluting blue and green hydrogen.

Grey hydrogen is the cheapest form of hydrogen production at current carbon prices

Indicative unsubsidised production costs* of hydrogen in Europe in €/kg for different carbon prices

The public debate for a net zero economy often assumes that hydrogen production will be green, both explicitly and implicitly. Governments also tend to focus on green hydrogen in their vision for a hydrogen economy or net zero pathway. But production of green hydrogen in Europe cannot compete with blue and grey hydrogen at current energy and carbon prices.

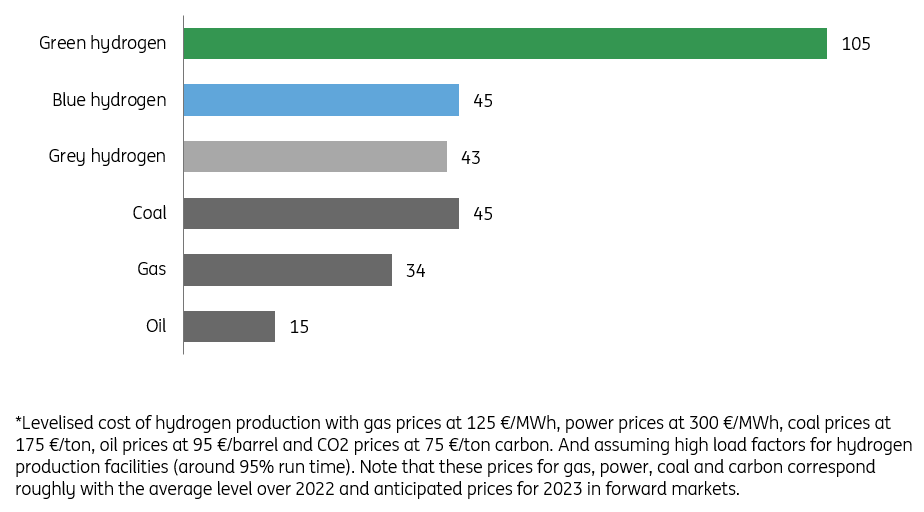

Green hydrogen is currently also more expensive than fossil fuels

At current market prices, green hydrogen is also not cost competitive with fossil fuels. Based on the energy content of fuels, green hydrogen is more than twice as expensive as coal and gas and almost seven times as expensive as oil.

Fossil fuels are not only cheaper, they are also performing better on important chemical characteristics, such as voluminous energy density. Many synthetic fuels, like hydrogen, are very light and voluminous substances, so they require a lot more space to store and use. That puts them at a disadvantage over fossil fuels when used in aviation, shipping, trucking and cars when it comes to the adjustments of the vehicles (large storage tanks) and the infrastructure required to run on these alternative fuels.

Fossil fuels are still cheaper, particularly compared to green hydrogen

Indicative unsubsidised production cost* of energy carrier in Europe in euro per GigaJoule

Corporate decision-makers in energy-intensive companies are exploring the option of synthetic fuel to reduce emissions and get to net zero. This does not mean green hydrogen will win out, however, as companies have to manage costs, too. In practice, green hydrogen will be in competition with other fuels. Fossil fuels are considerably cheaper and even within the hydrogen space, grey and blue hydrogen are cheaper. The adaptation of green hydrogen in the coming years will largely depend on the extent that governments are inclined to subsidise the price gap to help the industry scale.

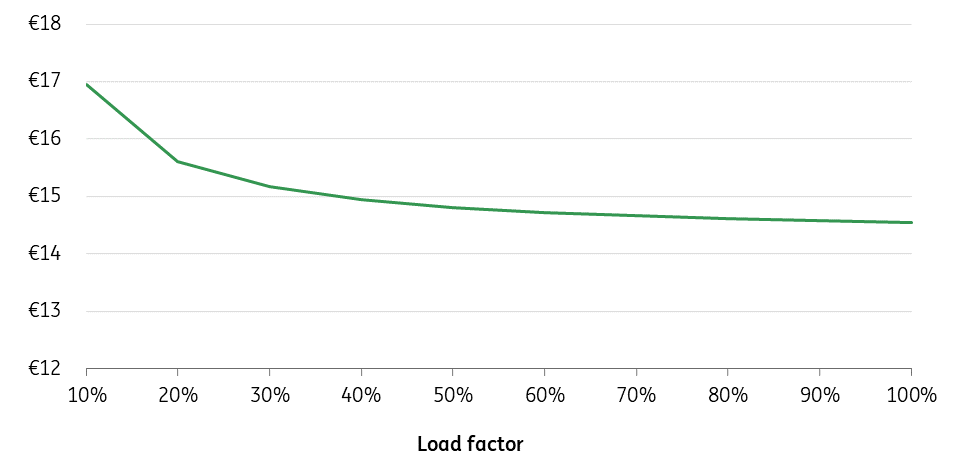

It is not economical to produce green hydrogen only at times when solar and wind power are in abundance

Solar panels and wind turbines are perceived as the pillars of the electricity mix in a net zero economy. Green hydrogen production is often presented as a solution to absorb an oversupply of solar and wind power on windy and sunny days when power prices are low. That could well be the case from a technical point of view. However, from an economic perspective electrolysers need to run all year round, 24/7, in order to reduce hydrogen costs.

Moments of surplus wind and solar power are still quite rare, even in power systems dominated by solar panels and wind power. Experts indicate that it is limited to 5% in 2030 and 20% of the time in 2050. If one runs electrolysers only in times of surplus solar and wind power, hydrogen production costs would increase by 2 €/kg (+17%) in the current market environment with high power prices.

The economics and runtime of electrolysers are even more important in normal market conditions. At historic power prices of 40 €/MWh, an electrolyser that operates on low runtimes (around 20%) produces hydrogen that is twice the cost (+100%) when the electrolyser runs all year round (95% runtime).

Higher electrolyser load factors lower hydrogen costs

Indicative unsubsidised production cost* of green hydrogen production in Europe for different runtimes of an electrolyser (load factor) in €/kg/H2

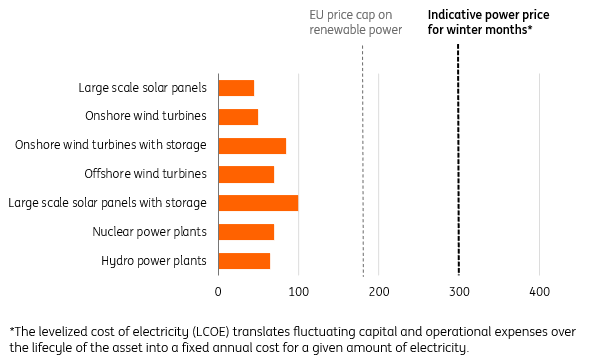

There is another reason why solar panels and wind turbines are mentioned a lot with respect to green hydrogen. Why would one pay high market power prices of 300 €/MWh or more, when the life cycle cost of electricity from renewable assets is often well below 100 €/MWh? The power costs are much lower if an owner of an electrolyser invests in solar panels or wind turbines to directly power the electrolyser. And this is a valid question too if one buys electricity from the power markets, now that the European Commission has capped the power price from renewables at 180 euro/MWh in the day ahead market. Renewables offer a way of becoming less dependent on high market power prices.

But, capitalising on lower power prices from renewables is difficult for three reasons;

- Increasing the runtime of electrolysers often also requires the use of grey power from the grid (see above).

- The proposed price cap only applies to the day-ahead market on which approximately 20-30% of the power is traded. So, most of the power is not subject to the price cap. European power generators, also the ones with solar and wind assets, tend to pre-sell about 80% of their future power production in one-year ahead futures contracts or through Power Purchase Agreements (PPAs).

- PPAs are designed to buy green power at fixed prices for longer periods, so hydrogen producers can use PPAs to lower power costs. That works in theory. In practice, PPAs are often linked to a power price index, so power prices from renewables still go up in times of crisis. And the length of PPAs is typically only a couple of years, so it is hard to fix the power price at the levelised cost over the entire lifecycle of the electrolyser, which lasts about 20 years.

Clean power is much cheaper compared to current market prices, also because some of it is capped by the EU

Indicative unsubsidised cost* of low carbon power sources in Europe in €/MWh

Corporate decision-makers face a trade-off in the economics of electrolysers between high fixed costs at low load factors and higher electricity costs at high run times. Ideally, one would like to run electrolysers on clean power from solar panels and wind turbines at all times. But an electrolyser that only runs on cheap power from renewables is simply not economical as it cannot recoup the high capital costs.

The economics of an electrolyser incentivise corporate decision-makers to maximise the run time of an electrolyser to lower the cost of green hydrogen. This often requires that electrolysers are also run by power from the grid, that at times may not be so green and powered by gas or coal-fired power plants. Sourcing renewable power through Purchasing Power Agreements in practice is only a partial solution.

Green hydrogen produced with electrolysers is not necessarily green(er)

Powering electrolysers to produce hydrogen requires a great amount of electricity. As aforementioned, electrolysers must run constantly in order to lower production hydrogen costs. In practice, this means that electrolysers run on power from the grid too, especially at times when the sun is not shining and the wind is not blowing. This could come with the downside of higher emissions, as power from the grid can be generated from coal or gas-fired power plants.

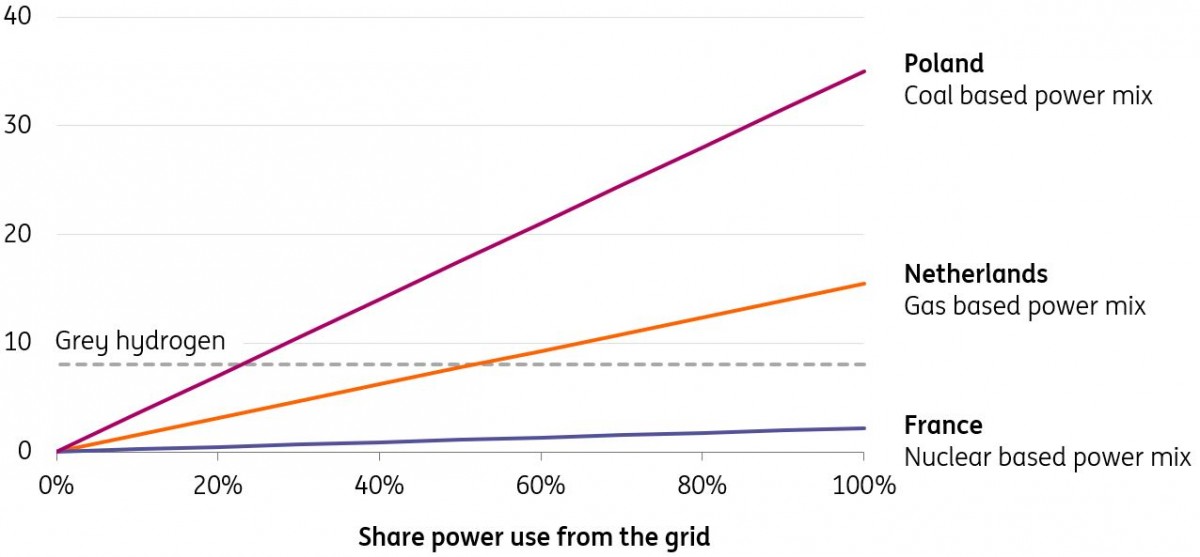

Grey hydrogen emits approximately 8.1 kilograms of CO2 per kilogram of hydrogen. When corporate decision-makers decide to use green hydrogen instead, they must carefully analyse whether this will lead to a decrease in the company's emissions. This is not an issue if one uses nuclear or hydropower (think of connecting an electrolyser to the grid in France or Norway). Green hydrogen will have lower emissions compared to grey hydrogen, even if the electrolyser is fully powered by the grid.

However, in countries with a lot of coal-fired power plants (like Poland), green hydrogen only comes with lower emissions if more than 85% of the power comes from renewables, which is unrealistically high. In countries with a lot of gas-fired power plants (like the Netherlands) hydrogen produced with electrolysers only comes with lower emissions compared to grey hydrogen if approximately 50% or more power comes from renewables.

A countries’ power mix determines whether green hydrogen comes with lower emissions than grey hydrogen

Indicative emission intensity in kgCO2/kgH2 for hydrogen produced with electrolysers in Europe for different amounts of power they take from the grid

So in order for green hydrogen to be truly green, a vast amount of renewable power is needed. It is estimated that global hydrogen production by 2050 would require 18 times the amount of current solar power and eight times the amount of current global wind power.

Corporate decision-makers face an incentive to run electrolysers 24/7 year-round to minimise the cost of hydrogen. That requires the use of grid power which could make green hydrogen more polluting than grey hydrogen. Sourcing green power from an energy company looks good on paper, but still requires the electrolyser to run on ‘dirty’ grid power at times when the sun is not shining and the wind is not blowing.

In practice, the emissions level of green hydrogen changes continuously based on the type of electricity that is used. A company’s decision to use green hydrogen should always be accompanied by decisions about a company’s power mix in order to guarantee a positive climate impact. In other words: company leaders have to tackle hydrogen emissions before they can position hydrogen as a viable net zero solution. This is the reason why the European Commission is setting standards and labels for green hydrogen.

A future for hydrogen: technological progress helps, but gas and power prices need to come down first

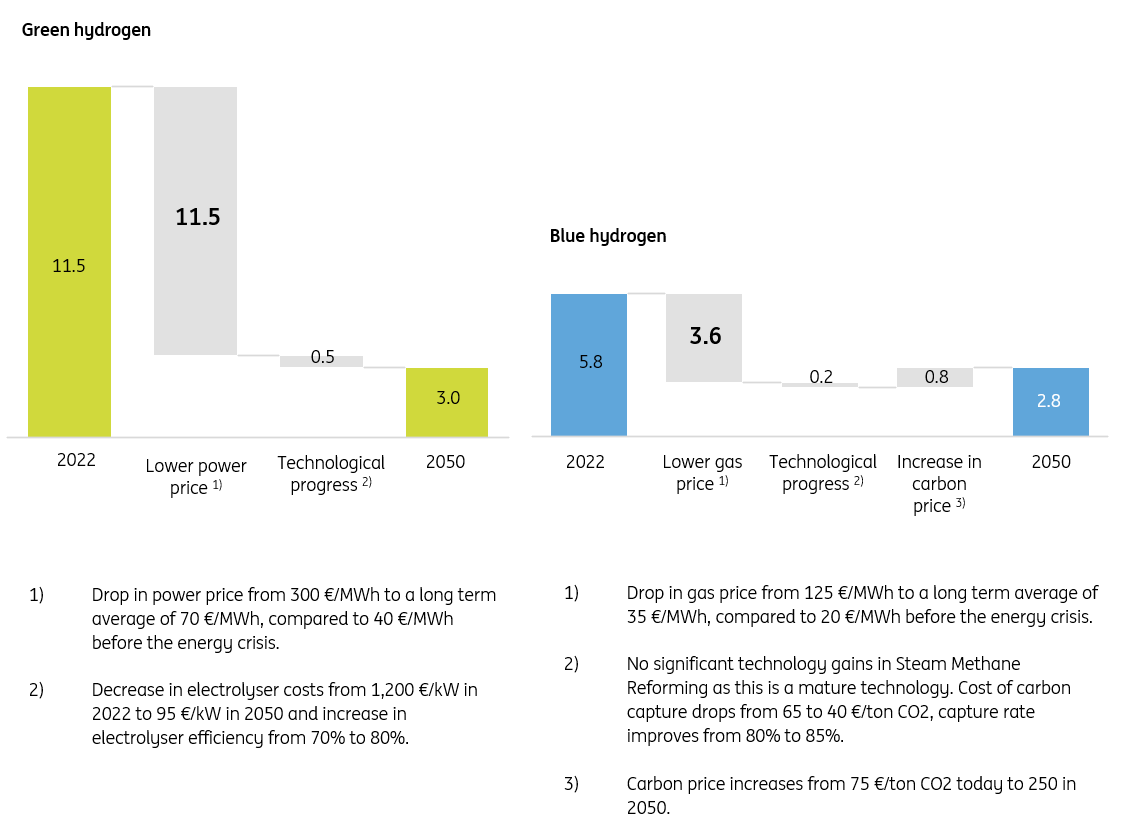

While hydrogen is currently very expensive, especially in Europe, there are two main drivers that are likely to significantly reduce the cost towards 2050.

- Like every crisis, the current energy crisis won’t last forever. Experts from Bloomberg New Energy Finance and Aurora Energy Research expect European gas and power prices to find lower equilibrium levels from 2025 onwards. That’s well before 2030, the year that many government policies target the hydrogen economy to really take off. The energy crisis does have a long-lasting impact though as long-term gas and power prices are expected to be 75% higher compared to past averages.

- Technological progress will reduce the cost of electrolysers and increase electrolyser efficiency. According to Bloomberg New Energy Finance, investment costs for PEM electrolysers will drop by over 90% towards 2050, from 1200 €/kW today to just 95 €/kW by 2050. Also, electrolyser efficiency is expected to increase from an average of 70% today to 80% by 2050. Electrolysers will use less power to produce a kilogram of hydrogen in the future as a result. Electrolyser technology is still in its infancy but is expected to see similar cost declines as solar panels and wind turbines have shown in the past.

Lower gas and power prices are the main source of declining hydrogen costs

Indicative unsubsidised levelised cost of hydrogen in €/kg (real prices)

Before the energy crisis, IRENA estimated that by 2050, hydrogen production costs in the northwest European region would be around €1.0-€2.0/kg. That seems no longer the case if the current energy crisis has a long-lasting impact on energy prices. According to Bloomberg New Energy Finance and Aurora, new equilibrium levels for gas and power prices are likely to be 75% higher compared to pre-crisis levels. In such a world, hydrogen production costs will be more in the range of 2.5-€3.0/kg, with green hydrogen still being the most expensive option.

But predicting gas and power prices is notoriously difficult. The energy crisis might also speed up the energy transition and phase out fossil fuels much faster, which might lower long-term gas and power prices. The IEA hints in that direction in its 2022 World Energy Outlook. That’s why we will monitor energy markets closely in the years ahead and continue to assess the impact on the economics of synthetic fuels.

Before the start of the energy crisis, innovation was considered the biggest driver of lower hydrogen costs towards 2050. It still has a role to play, but lower gas and power prices have a much bigger impact now that Europe is facing an unprecedented energy crisis.

Conclusion

Currently, the production and use of synthetic fuels like hydrogen are often done by one company or within a specific cluster of companies in the chemical sector. Unfortunately, this is far from easy as producers are faced with many economic and environmental trade-offs, such as high energy prices, high technology costs and a shortage of renewable power. That’s why we’ve presented eight insights that corporate decision-makers need to know about synthetic fuels, so they can make them work. Our analysis shows that gas and power prices need to normalise for the production of synthetic fuels to take off.

Now corporate leaders in many other sectors are looking at how synthetic fuels can set their companies on a pathway to net zero emissions by 2050. The use of synthetic fuels:

- holds the potential to fundamentally change the business towards net zero emissions;

- provides energy-intensive businesses a license to operate in a low-carbon world and gain support from society

- could reduce fossil fuel dependency and supply chain disruptions.

In future articles, we will shift the focus from the production side of synthetic fuels towards the use case of synthetic fuels in transportation, manufacturing and buildings.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article