Hydrogen trade: a prerequisite for net zero in the Netherlands and US

- 26 October 2022

- Sustainability

Hydrogen trade is at a nascent stage but could see huge growth this decade. Hydrogen trade will be crucial for net importers like the Netherlands to reach net-zero targets, and for net exporters like the US to maximise benefits from clean energy deployment. More infrastructure and offtake agreements are needed to establish a global hydrogen market faster

Hydrogen trade is still in its infancy but is likely to ramp up this decade

Hydrogen will play a key role in decarbonising the global economy. It is estimated that hydrogen will contribute to 6% of the emissions reduction that is needed to get the world to net-zero emissions by 2050. Global demand for hydrogen is set to substantially increase, although today, hydrogen is a very local business. According to the International Energy Agency (IEA), about 85% of hydrogen gas is produced and consumed on-site within a facility rather than bought and sold on a market.

In the long term, however, hydrogen is likely to become an internationally traded commodity to help countries meet their hydrogen demand in a more economical way. For blue hydrogen (see chart below for definition), countries with more advanced carbon capture and storage technologies will have a comparative advantage for production and exports. Similarly, green hydrogen will be most economically produced in locations that have an optimal combination of abundant renewable resources, available land, access to water, and the ability to transport and export energy to large demand centres.

The International Renewable Energy Agency (IRENA) estimates that by 2050, green hydrogen can be produced cheapest in Australia and Africa at $0.60-$1.0/kg, followed by Latin America and the southeast region of the US at $0.6-$1.5/kg. Production costs in the northwest European region are expected to be considerably higher at $1.5-$2.5/kg and the region has more spatial challenges to produce large volumes of green hydrogen. Over time, it is expected that these differences make up for the transportation costs of hydrogen and its trading derivatives such as ammonia and methanol.

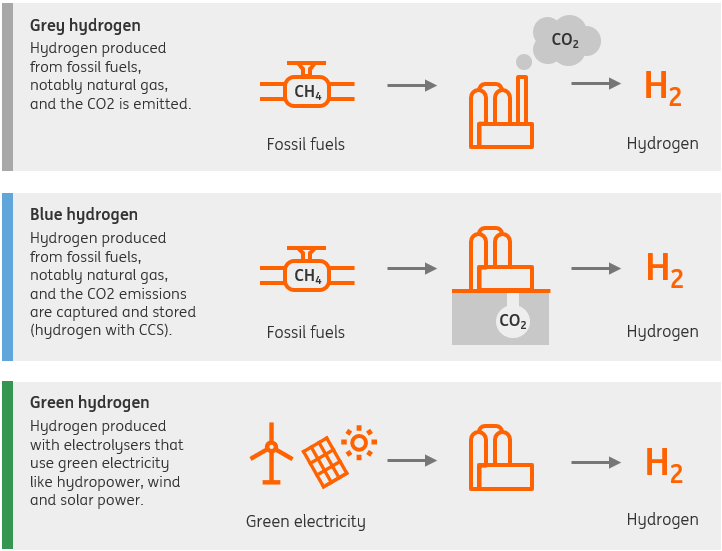

A colourful bouquet of hydrogen production techniques

Hydrogen production techniques

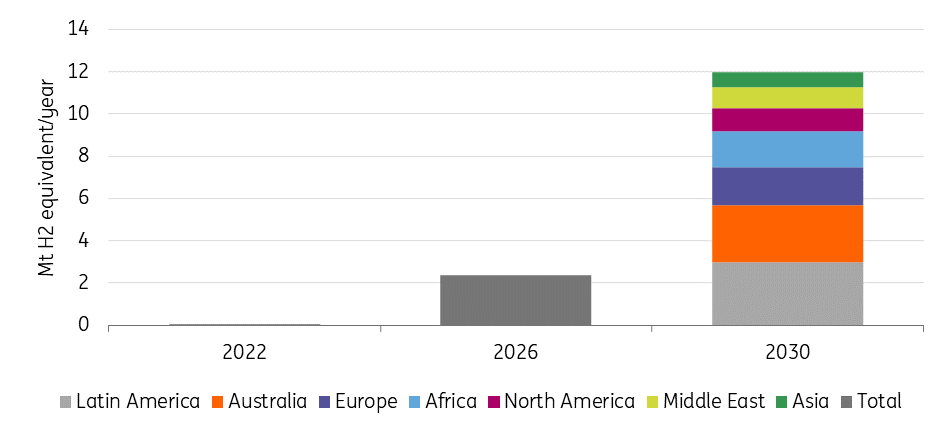

Countries and companies are starting to lay out hydrogen export plans. The IEA estimates that by 2030, more than 12 million tonnes (Mt) of low-emission hydrogen will be exported per year – a huge jump from little to no hydrogen exports today. The planned export projects are located across different regions. Of the 12 Mt, 3 Mt will come from Latin America, followed by 2.7 Mt from Australia, 1.8 Mt from Europe (most of which will be intra-continental), 1.7 Mt from Africa, 1.1 Mt from North America, and 0.7 Mt from Asia.

Planned low-emission hydrogen exports

In this article, we will illustrate the importance of future hydrogen trade through the analysis of two countries: the Netherlands, which is set to become a hydrogen net importer, and the US, which is likely to be close to self-sufficiency but is expected to be a key exporter. We will also look at how hydrogen trade is a crucial component in implementing the two countries’ national hydrogen strategies and realising climate targets.

Netherlands: Ambitious plans to build hydrogen infrastructure – but don’t forget about hydrogen demand

Currently, the Netherlands produces around 175 petajoules (PJ) of hydrogen. In terms of volume, around seven billion cubic metres are produced in processes where hydrogen is the main product, for example in the production of ammonia (fertilisers) and methanol (chemical industry). In other processes, around nine billion cubic metres of hydrogen is produced as an inevitable byproduct, for example in gasoline production (naphtha crackers) and steelmaking (coke oven gas). In Europe, the Netherlands is the second-largest user of hydrogen after Germany. Almost all hydrogen is produced from natural gas (grey hydrogen), without capturing and storing the carbon emissions (blue hydrogen). Natural gas in Europe soared to 350 euro/MWh during the summer, driving the cost of hydrogen production up tenfold. Prices have come down to 100 euro/MWh recently, but that still makes hydrogen three times more expensive compared to pre-energy crisis levels.

The Netherlands, like many other European countries, has high ambitions for hydrogen. Scenarios from Dutch grid operator TenneT for a net zero economy by 2050 point to Dutch hydrogen use of 200 to 900 PJ per annum. But hydrogen production must transition away from grey hydrogen created from natural gas towards green hydrogen production based on electrolysis with solar and wind power. Blue hydrogen can be a transitory solution to lower emissions from natural gas-based hydrogen production, as it captures and stores most of the emissions (CCS).

While 2050 provides a dot on the horizon for hydrogen demand, businesses and policymakers need guidance for the nearer term. That’s why the Dutch government has set five important hydrogen targets for 2030:

- Development of hydrogen infrastructure between the main industrial clusters and neighbouring countries by HyNetwork Services, a subsidiary of Gasunie, the Dutch transmission system operator of the gas infrastructure. The infrastructure will be developed in three phases:

- The first phase runs to 2026 and comprises pipelines in the western part of the country to connect the industrial cluster at the coastline (Zeeland, Rotterdam, Amsterdam, Den Helder, Noord).

- The second phase runs to 2028 and comprises eastern pipelines running from Eemshaven in the north (Noord) to the Chemelot industrial cluster in the south (Limburg) and connecting the hydrogen infrastructure in the Netherlands with Germany.

- By 2030, these western and eastern routes will be connected to a southern route that also taps into the Belgium hydrogen infrastructure (third phase near Sas van Gent and Dilsen).

- Investment in the Dutch hydrogen infrastructure is expected to total €1.5bn of which the government will provide €750m.

- Three to four underground hydrogen storage facilities will be built in the north and northeast parts of the Netherlands using empty salt caverns.

- In order to make the transition from grey to green hydrogen, the government aims for a 500-megawatt electrolyser capacity by 2025 and a 3-to-4-gigawatt capacity by 2030.

- To power the electrolysers with renewable energy, the government aims for 21 gigawatts of offshore wind capacity by 2030 and 35 terawatt hours of onshore renewable power generation, mostly from solar panels and onshore wind turbines. The Dutch government, for example, is developing coordinated tenders for offshore wind and hydrogen and has provided a subsidy for the world's first pilot with offshore hydrogen production from seawater. Nevertheless, current estimates indicate that the offshore wind target is very ambitious while the onshore target is likely to be met well before 2030.

The Netherlands will need to import green hydrogen if it wants to meet EU targets

The Netherlands is one of the countries that will likely rely on large amounts of hydrogen imports to achieve its clean energy targets. The European Commission, as part of the Fit-for-55 package, has proposed a target for member states to ensure that 50% of all hydrogen used in manufacturing will come from green hydrogen production.

This target is very ambitious and, according to CEDelft, the impact on the Netherlands will be larger than on most other EU member states due to the large concentration of industries that use hydrogen, such as the chemical industry and refineries. CEDelft analyses three hydrogen demand scenarios for the Netherlands and investigates if the 50% green hydrogen target can be fully met with domestic production or to what extent green hydrogen must be imported. The study concludes that:

- The low-demand scenario requires 80 PJ of green hydrogen production by 2030 to meet the 50% target.

- This low-demand scenario requires an additional five gigawatts of offshore wind energy on top of the existing plans to grow the current capacity from two gigawatts to 21 gigawatts in 2030.

- Most of the available renewable power will be needed to produce green hydrogen, leaving no green power for the electrification of buildings, transportation, and agriculture.

Given the fact that the targeted 21 gigawatts of offshore wind capacity are already highly ambitious and the fact that every sector wants green power too in order to become more sustainable, it is unrealistic that the Netherlands can meet the 50% green hydrogen target without importing large volumes of it. The need to import green hydrogen is even higher in the mid and high-hydrogen demand scenarios, if one considers the fact that Dutch harbours could also import hydrogen for Germany and Belgium. Dutch hydrogen imports could range from 48 to 120 petajoule by 2030, according to CEDelft.

As a result, the Netherlands is partnering with countries all over the world to set up hydrogen trade relations. In 2020, the US and the Netherlands signed a statement of intent to collaborate on hydrogen. That should be viewed as the foundational work for a future hydrogen economy. The existing Memoranda of Understanding between the Port of Rotterdam and the ports of Houston and Corpus Christi to facilitate trade only add to that process.

US: Ramping up hydrogen efforts with new legislation and roadmap

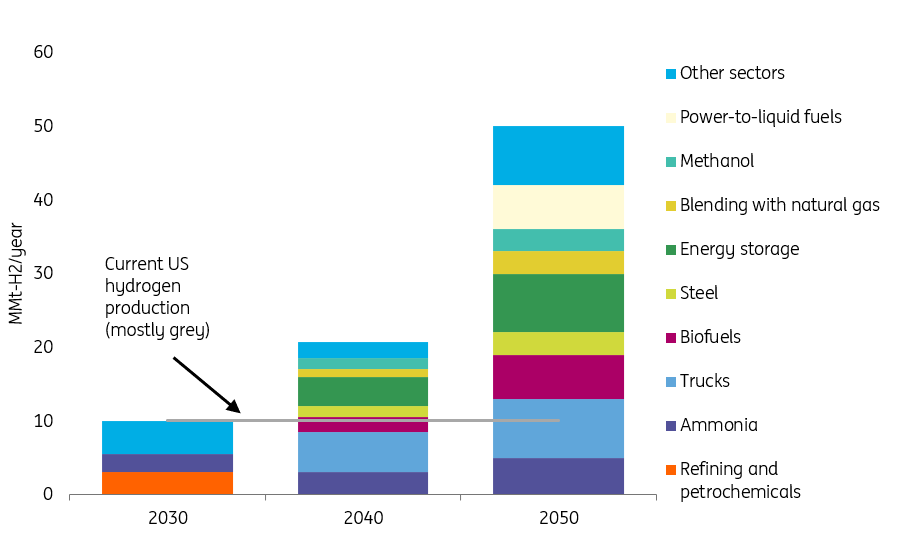

The US is the second-largest consumer and producer of hydrogen behind China. The US produces roughly 10 Mt of hydrogen per year, accounting for 11% of production globally. However, more than 95% of the hydrogen is grey. In its National Clean Hydrogen Strategy and Roadmap published in September, the Department of Energy (DoE) has set up a target to produce 10 Mt of clean hydrogen per year by 2030, before ramping up to 20 Mt annually by 2040 and 50 Mt annually by 2050.

Clean hydrogen production estimates from the DoE’s roadmap

A number of hydrogen projects have been announced and are being developed. One driver for this is the Infrastructure Investment and Jobs Act passed last year, which aims to dedicate $9.5bn to clean hydrogen development. Of this, $8bn is allocated to establishing regional clean hydrogen hubs (H2Hubs) across the country in the industrial sector and beyond, $1bn is set to advance the Hydrogen Electrolysis Program and lower the cost of electrolysis and hence hydrogen production, and $0.5bn is targeted at promoting hydrogen manufacturing and strengthening domestic supply chains.

In June, the DoE announced details of the selection criteria for the $8bn H2Hubs programme over the next five years. The DoE intends to grant funding to at least four H2Hubs and there are already several states aiming to apply as a coalition or individually. The DoE plans to select hubs that would together form a diverse hydrogen portfolio in terms of feedstock, end-use, and geography. The DoE will choose at least one hub that produces hydrogen from fossil fuels (with CCS technologies), one from renewables, and one from nuclear energy; it will also grant at least one hub in the power, industrial, heating, and transportation sectors.

Additionally, the Inflation Reduction Act signed into law in August has introduced production tax credits (PTCs) between $0.6/kg and $3/kg for clean hydrogen development in the country if certain wage and labour requirements are met. Projects that have lifecycle emissions of less than 4kg of CO2 equivalent per kg of produced hydrogen (kgCO2e/kgH2) can start receiving tax credits – this is aligned with the DoE’s newly proposed clean hydrogen production standard. To receive the highest credits, a project needs to emit lower than 0.45 kgCO2e/kgH2. Despite the strict qualification provision, the hydrogen PTCs would largely lower the cost of hydrogen production. Bloomberg New Energy Finance estimates that at this PTC level, clean hydrogen production could already be cost-competitive with grey hydrogen production. The infrastructure bill and the Inflation Reduction Act will together attract more new hydrogen projects in the US over the next few years.

US: Hydrogen hub and port buildout sets the scene for exports

The US does not have a specific target for hydrogen trade, but the DoE’s draft National Clean Hydrogen Strategy and Roadmap sets a long-term goal to establish US leadership in the global energy transition through exporting clean hydrogen. The US is well situated for hydrogen exports through hydrogen hubs and ports in coastal states.

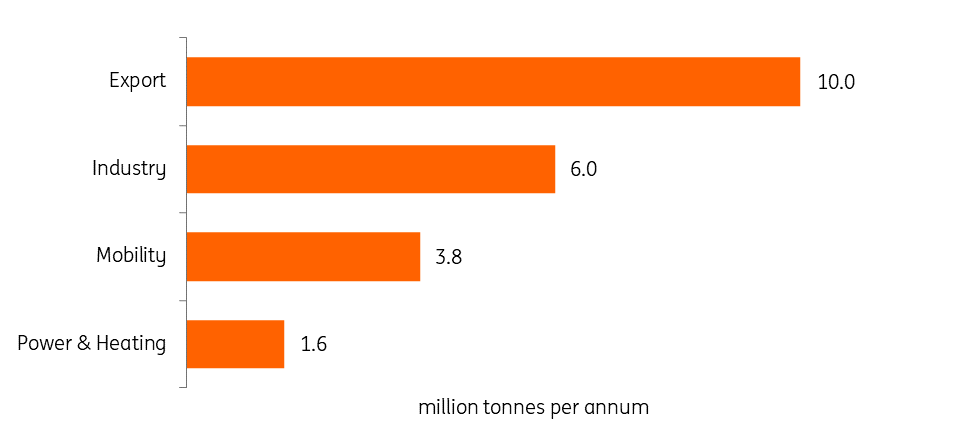

For example, Texas is a region with significant advantages for the deployment of hydrogen – not only green hydrogen that is produced using wind and solar power but also blue hydrogen from cheaper-than-national-average natural gas using carbon capture and storage technologies. Texas already has the advantage of existing facilities that produce ammonia (a hydrogen carrier for transportation). While the initial exports are looking to be blue because of the abundant access to natural gas in Texas, more exports of green hydrogen will follow suit in the longer term. McKinsey forecasts that Texas will likely be able to export around 10 million tonnes per annum (MTPA) of hydrogen by 2050, provided that its share of global hydrogen remains at today’s level of 4%, or that future exports align with the state’s current 8% share of global liquefied natural gas (LNG) export.

Several hydrogen hubs and projects are being developed in the state, including Hydrogen City, Clear Fork, H2 HoustonHub, and Port of Corpus Christi Hydrogen Hub. In 2021, the Port of Rotterdam and the Port of Corpus Christi signed a memorandum of understanding (MOU) to collectively develop new technologies such as hydrogen. This will facilitate the trade of the fuel in the future.

Demand for clean hydrogen in Texas could reach 21 MTPA, with exports contributing most to demand

Hydrogen use in Texas by 2050 in million tonnes per annum

Hydrogen exports can help the US maximise the benefits of deploying clean energy projects and further take advantage of the clustering effects of infrastructure and resources, which can then fast-track the country's pursuit of a net-zero economy.

Building the international hydrogen trade market

Although an estimated 12 Mt of clean hydrogen is forecast to be exported per year by 2030, only a sixth of it is already under an offtake agreement or has a potential buyer in the consortium of the project. It is therefore important for governments to develop programmes and advance partnerships to facilitate hydrogen trade. The Netherlands has one of the highest planned import volumes of hydrogen; the country has also identified ten criteria for the development of an international hydrogen market, including reliable certification for hydrogen, and the development of trade channels with standardised contracts, among others.

From a global perspective, a prerequisite for the international trade of hydrogen is trade infrastructure. First, pipelines will be needed for the in-land transport of hydrogen. A hydrogen pipeline network can come from repurposing natural gas networks or injecting hydrogen into a natural gas stream using the existing infrastructure, both of which will require substantial reconfiguration and adaptation. Hydrogen can also be transported via specialised intermodal (truck and train) tanks, but this kind of infrastructure, which remains limited currently, will also require substantial expansion. Additionally, ships will be needed for overseas trade. Hydrogen will need to be transported either via a carrier (such as ammonia) or in liquified/compressed forms. There have also been discussions about repurposing LNG infrastructure to transport hydrogen, in a scenario where a more rapid transition away from natural gas is facilitated.

Conclusion

- Hydrogen trade holds a promise in the global energy transition process.

- Governments have started to take the first steps in the development of future hydrogen trade.

- This is a prerequisite to put their economies on a pathway to net zero emissions.

- But we are still a long way from an international hydrogen market. And it is too early to tell whether the energy crisis in many parts of the world will speed up (green) hydrogen production as governments and corporates look for ways to become less dependent on fossil fuels, or delay the process as high energy costs drive up hydrogen production costs too.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Scream if you want to go faster

- This bundle contains 7 Articles