Hawkish shift opens the door to Fed rate hikes

- 20:41

- FX Rates United States

A clear hawkish shift from the Fed sees the committee split down the middle on whether they will hike rates or not this year. Sharp energy price falls are good news though, and we think an extended pause is the most likely outcome

Markets acknowledge the prospect of higher policy rates

The Federal Reserve has left monetary policy unchanged at Kevin Warsh’s first meeting as Chair. It was a unanimous decision given that arch-dove Stephen Miran had made way for Warsh to join the Board of Governors, while the clear adjustment to the tone of the much cut-down press release was sufficient to bring the three hawkish dissenters from May onside. In a message to leave no doubt in investors’ minds over the inflation fighting credibility of the central bank, the statement concluded: “the Committee will deliver price stability”.

The even more obvious hawkish shift was seen in updated Fed forecasts. The new “dot plot”, has 9 of 18 members pencilling in a rate hike versus zero in March, which shows the Fed has gone well beyond signalling “two-way risk” on interest rates, to a clearly more hawkish position.

One member is, in fact, predicting three 25bp hikes over the coming six months; five members are going for two hikes and three are going for one hike. Eight expect no change with just one forecasting a rate cut this year. There are only 18 dots versus the usual 19. As broadly expected, Kevin Warsh decided not to enter a prediction having said in the past that the Fed's record was "abysmal" and that he saw little value in it. He added at the press conference, “I can’t give you any guidance on what we’re going to do next."

As such, the median is now for one hike this year, but then a cut next year with a further cut in 2028 before settling at a 3.0-3.25% range over the longer term.

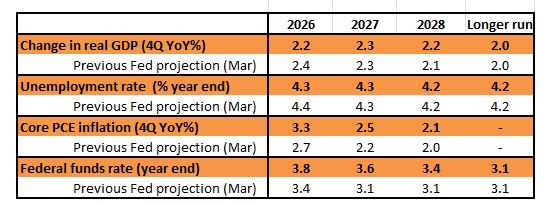

Fed projections versus the previous expectations from March

The table above shows the Federal Reserve's updated median forecasts versus what they were saying in March. They are a little more upbeat on GDP growth for fourth quarter 2026 than the consensus (2.2% versus 2%), but more worried about inflation than the consensus (core PCE deflator at 3.3% versus the 3.1% consensus).

Kevin Warsh, appointed by a President demanding rate cuts, may well face some criticism after this. Nonetheless, his emphasis on needing to prevent second-round price effects will help to keep the long end of the yield curve anchored. This is, in fact, more important for the President’s growth strategy by keeping a lid on mortgage and corporate borrowing costs while also limiting the upside for government interest costs.

An extended pause from the Fed remains our call

Markets are now pricing 32bp of rate hikes this year, with a cumulative 42bp by this time next year, versus 19bp and 33bp respectively ahead of the release. Nonetheless, we look for an extended pause of perhaps 12 months.

With a deal set to be signed imminently to reopen the Strait of Hormuz, energy prices have fallen sharply. $76/bbl WTI oil is consistent with gasoline prices falling to $3.75/gallon after having peaked at $4.60. That should help lead to an outright month-on-month % drop in headline prices for June. It will also relieve pressure on airline fares and freight rates within the inflation data, while also easing the squeeze on household spending power.

While recent jobs numbers have been firmer, consumer confidence is rock bottom in an environment where real household disposable incomes are languishing. Consumer and market inflation expectations remain in tolerable ranges and slowing housing rents, weak wage growth and a waning influence from tariffs should, we believe, gradually ease the concerns of the Fed.

The Treasury curve shifts higher and flatter, but the curve structure remains benign

Impact reaction to the FOMC outcome was a flatter curve, led by the front end. That bit is straightforward, given the change in tone from the FOMC as a whole, and the upshift in the median dots. The 10yr yield is up, back to the 4.45% area, and rising. What’s interesting is the breakout of this, as the breakeven inflation rate fell, while the real rate rose. The aggregate rise in the 10yr yield came from a bigger pop in the real yield versus the fall in breakeven inflation.

This has been a key theme in the past few months – ongoing upside to real rates, alongside falls in inflation expectations. In fact, breakeven inflation is on aggregate quite tame. Printed inflation is in the 4% area, while the 10yr breakeven is just under 2.3%. And in fact, breakevens remain tame right along the curve. Our bottom line view from all of this is that long-dated yields are liable to remain sticky to the upside (breakevens are already tame and real yields are on the rise, or at the very least holding steady).

The hawkish tilt is classically not good for the front end, and theoretically, it can be a calming influence for the back end, on a theory that the Fed is showing some preparedness to take action, if needed, to help tame inflation. The overall outcome of a flatter curve based on this is straightforward. We still worry that the 10yr yield can drift higher from here, to the 4.5% area and above. That said, the 5yr area has richened further slightly, showing the market is not fully bought in on rate hikes being a dominant theme in the coming quarters.

Beyond that, we had expected something on balance sheet management, but little to nothing on this. The bill-buying programme continues, and the ample reserves environment is sustained. It seems that the balance sheet reduction project is all being left to another day.

Dollar enjoys commitment to price stability

After this week’s large fall in energy prices, FX markets probably went into today’s FOMC meeting with a neutral bias. In the end, the outcome was clearly hawkish with a slimmed-down statement refocusing on price stability, a rate hike in the dot plot and a few references to the Fed having missed its inflation target for five years running.

The dollar took its cue from the 10bp bearish flattening in the US yield curve and rallied around 0.5% on the news that the Fed is prepped to tighten. Also welcome for the dollar is the read-out for US asset markets, where stability at the long end of the bond market and equities reversing intra-day losses suggest buy-side investors appreciate the renewed commitment to price stability.

That commitment also serves to deflate interest in the dollar de-basement trade, which last year had seen gold, bitcoin and the likes of the Swiss franc rallying on the view that a captured Fed could go soft on inflation. That looks far less likely after today’s FOMC meeting. Gold is off 2.5% on the news and USD/CHF up around 0.7%. These trends can extend.

A hawkish Fed can keep EUR/USD pressing 1.1500 this summer, with the risk of a temporary break lower should any US activity or price data briefly push market expectations towards 50bp of tightening this year. Japanese authorities must now be bracing for higher levels in USD/JPY – perhaps into the 162/163 area – before another round of intervention is due. But the already slim chance of effective dollar selling intervention just got slimmer.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more