Gold’s correction prompts a forecast reset

- 24 June

- Commodities, Food & Agri

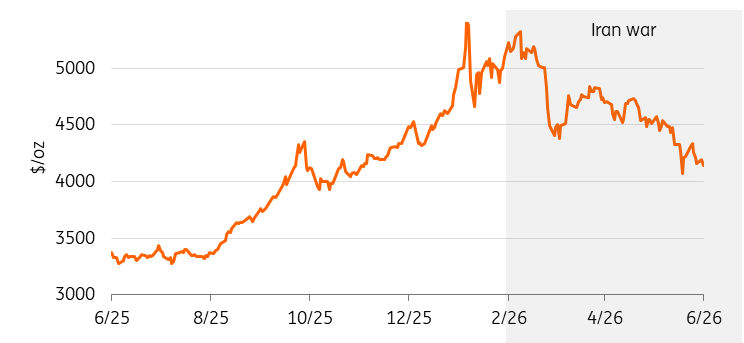

Gold’s correction has become increasingly difficult to ignore

After reaching record highs earlier this year, prices have fallen sharply, leaving gold in negative territory for the year. Rising Treasury yields, a stronger US dollar and weaker investor demand have weighed on the market, forcing investors to reassess the factors that drove the rally.

The sell-off may appear surprising given ongoing geopolitical uncertainty and continued central bank buying. However, gold’s weakness highlights the extent to which markets have shifted their focus from safe-haven demand towards the implications of higher interest rates and tighter financial conditions.

While we remain constructive on gold over the medium term, the near-term environment has become more challenging. As a result, we are lowering our gold price forecasts.

Gold struggles despite geopolitical tensions

We are lowering our forecasts

Higher yields, a stronger dollar and weaker ETF demand are likely to weigh on gold for longer than we previously anticipated.

We now expect gold to average $4,300/oz in the third quarter of 2026 and $4,600/oz in the fourth quarter, down from our previous forecasts of $4,850/oz and $5,000/oz, respectively.

While markets have become increasingly concerned that interest rates could remain higher for longer, our US economist continues to expect the Federal Reserve to remain on hold. Still, elevated yields and a strong dollar are likely to remain near-term headwinds for gold.

Markets have repriced the interest rate outlook

The primary driver behind gold’s recent decline has been a significant repricing of interest rate expectations.

Following recent Fed communication, investors have pushed back expectations for monetary easing, driving Treasury yields higher and supporting the US dollar. This has created a less favourable backdrop for gold, which typically struggles when real yields rise and the dollar strengthens.

At the same time, geopolitical tensions have failed to generate the type of safe-haven inflows seen during previous periods of uncertainty. Instead, markets have focused on the inflationary implications of geopolitical developments and what they could mean for monetary policy.

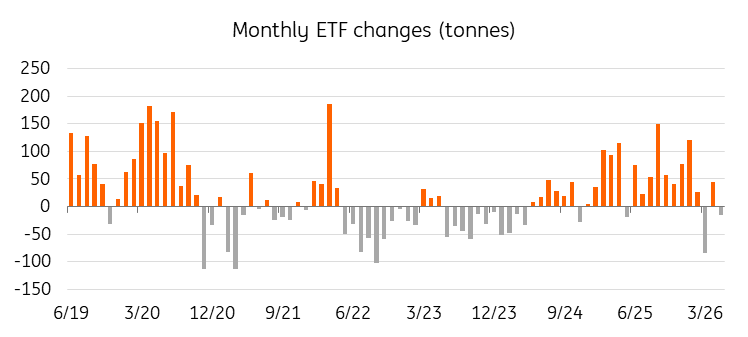

ETF demand has weakened

ETF investors were a major force behind gold’s rally at the start of the year, helping push holdings to their highest level since 2022.

However, sentiment shifted sharply in March as investors reassessed the outlook for US monetary policy. Rising yields and a stronger dollar triggered profit-taking, particularly among North American investors, leading to a reversal in ETF flows.

Global gold ETF holdings are now around 1.5% below where they started the year. While recent inflows suggest selling pressure may be easing, ETF demand is likely to remain less supportive than it was in 2025.

Gold ETF buying slows

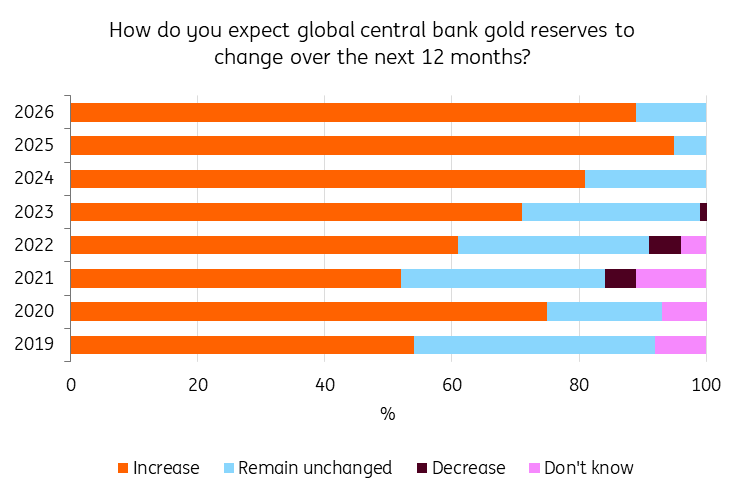

Central banks continue to provide support

While investor demand has weakened, central bank buying remains a key pillar of support.

Central banks and official institutions added around 244 tonnes of gold during the first quarter of 2026. Poland remained one of the largest buyers, while China extended its gold-buying streak to 19 consecutive months. Several other emerging-market central banks also continued to add to reserves.

The longer-term outlook for official sector demand also remains constructive. According to the latest World Gold Council survey, 84% of central banks expect gold to account for a larger share of global reserves over the next five years, while nearly 90% expect official gold holdings to increase over the next 12 months.

This continued appetite for gold reflects ongoing reserve diversification efforts and should help provide a floor under the market even as investor demand remains under pressure.

Central banks expect higher gold holdings

The longer-term story remains intact

The recent correction has been driven primarily by cyclical macroeconomic headwinds rather than a deterioration in gold’s structural fundamentals.

Central bank demand remains robust, reserve diversification continues, and geopolitical risks remain elevated. However, higher yields and weaker investor demand are proving more powerful headwinds than we previously anticipated.

Gold’s correction has prompted a reset in our forecasts, but not in our broader view of the market. We continue to believe the structural drivers supporting gold remain intact, though the path higher is likely to be slower and more volatile than we previously expected.

Silver's outlook has also weakened

We are also lowering our silver price forecasts. While the silver market is expected to remain in deficit, some of the strongest demand drivers are becoming less supportive. Growth in solar demand is slowing, while continued thrifting and substitution in photovoltaic manufacturing are reducing silver intensity per panel.

At the same time, higher yields, a stronger dollar and weaker investor demand are weighing on precious metals more broadly. We now expect silver to average $68/oz in the third quarter of 2026 and $74/oz in the fourth quarter, down from our previous forecasts of $79/oz and $84/oz, respectively. Despite the downgrade, we continue to expect silver to modestly outperform gold, supported by ongoing market deficits and broader electrification trends.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more