GBP: Rocked by Brexit resignations, sterling could fall another 3 to 4%

- 15 November 2018

- FX United Kingdom

The resignation of the British Brexit Secretary, Dominic Raab, has increased the chances of a leadership challenge to Theresa May and a 'no-deal' Brexit. Investors can demand greater risk premia of UK assets, which could mean another 3 to 4% fall for sterling

Raab rocks GBP

After rallying on a brief period of optimism on the scope for a soft Brexit, GBP has today been hit hard by the resignation of Dominic Raab, the Brexit secretary. His resignation letter referenced two key concerns of the Withdrawal Agreement recently negotiated between London and Brussels, namely: i) the threat to the integrity of the UK posed by the proposed regulatory regime for N.Ireland and ii) the EU holding a veto over the UK’s ability to exit the back-stop of a customs union.

For the Brexiteers, the withdrawal deal offers too many concessions to Brussels. For the Remainers, they reject the proposition that it is a question of this (bad) deal or no deal at all. They would prefer another referendum or at least a delay in Article 50 to allow more time to negotiate a better deal.

Investors must weigh up two key challenges

International investors now have to weigh up the chances of a leadership challenge against the Prime Minister, Theresa May, in addition to the (seemingly declining) chances of the withdrawal deal being approved by UK parliament in December. On the former, the news cycle will be focusing on whether sufficient names are backing a no-confidence vote in May, which could potentially take place in the next few days.

For reference, our Chief International Economist, James Knightley and our UK economist, James Smith, both think that we won’t see a leadership challenge, arguing that one would merely delay negotiations and make an Article 50 extension and a Brexit delay more likely. So let’s see what happens within Conservative ranks over the next few days.

Not enough risk priced into GBP

For GBP, the question is how much risk premium should be priced in? Is enough priced in already? We would say not. Until there is some clarity on a leadership challenge, there is a risk that we end up with a more Brexit-leaning leader. Such an outcome would increase the chances of a No Deal, on the assumption that a new leader would be unlikely to secure any further concessions from Brussels. That is up for debate but would suggest a change in Conservative leadership - a scenario not in our baseline, nor likely in investors’ baselines either.

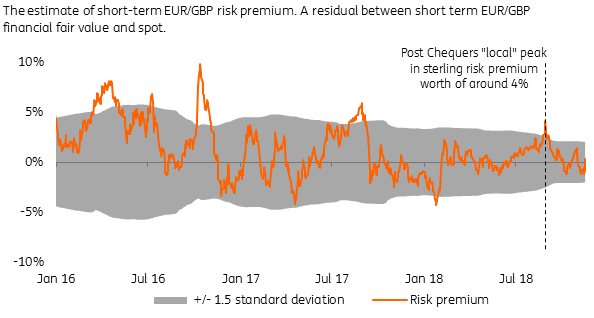

In determining how much risk premium is priced into GBP, we use a Financial Fair Value model (FFV) (see the chart below), which looks at which financial variables have done a good job of explaining where EUR/GBP should be trading. This morning we calculated that the risk premium was around zero – i.e. EUR/GBP was trading in line with short-term financial variables. But as recently as August, GBP traded with a 3-4% risk premium on the uncertainty around the Chequers deal and the Brexit supporting former Foreign Secretary Boris Johnson’s resignation. In other words, were the market to price in a more credible leadership challenge, GBP could potentially fall another 3-4% - sending EUR/GBP back towards the 0.91 region and GBP/$ towards new lows for the year near 1.23/24. That’s the risk.

EUR/GBP Financial Fair Value model suggests current risk premium is very modest

Investors are underweight UK, but can add to shorts

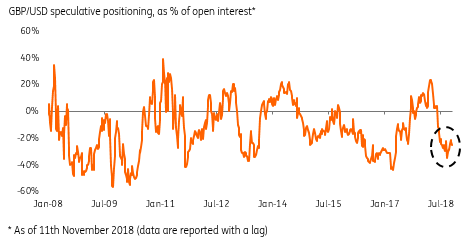

Perhaps one of the few supports to UK assets right now could be positioning. Is the market ‘limit short’ GBP such that there is no one left to sell? Well, speculative positioning data from the Chicago futures market (see chart below) suggests that while the market is undoubtedly short GBP against the dollar, it is not quite as short as it was in early 2017.

One of the few supports to UK assets could be positioning

In terms of equities, global equity investors remain substantially underweight as they have been since the Scottish referendum in 2014, but buy-side surveys suggest they are not as underweight now as they were in late 2017/early 2018.

Even though it is very hard to make baseline forecasts on GBP right now, we would say that GBP could fall another 3-4% unless the threat of a leadership challenge is quashed or there are clearer signs that the withdrawal agreement can garner more support in parliament.

Speculative positioning in GBP/USD

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Peak uncertainty

- This bundle contains 8 Articles