FX: In the dollar we do not trust

Given huge adjustments in financial markets, we are now being asked: ‘What’s mis-priced?’. 10-20% declines against the dollar argue that commodity and EM currencies have discounted a lot. When dislocation in USD funding markets is resolved and some calm returns to markets – probably over coming weeks – we will come to see that the dollar is overpriced

Two factors driving dollar strength, both temporary

Foreign exchange markets are normally described as the most efficient in the world meaning that, in theory, everything is the right price. Our job as FX analysts is to understand which factors are driving markets currently, how those factors will change and how currency markets will adjust in future.

Of the myriad factors at work in currency markets right now, we chose to focus on two: i) USD funding challenges and ii) a mass exodus in portfolio flows from emerging markets.

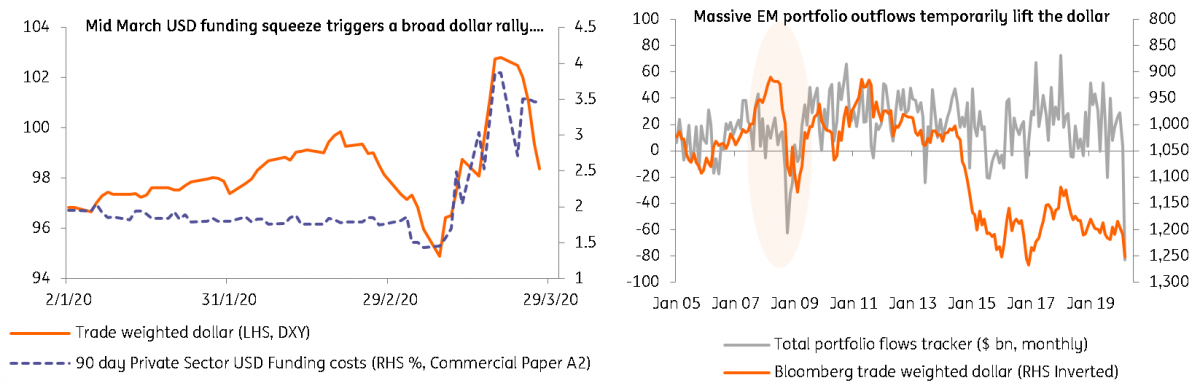

The first is the well-documented breakdown in the US Commercial Paper (CP) market, which occurred around 11/12 March. Credit risk became of paramount importance to investors around the world, including in the CP market. Investors switched money out of Prime and into government money market funds, preferring public over private-sector risk. The move deprived the CP market of its biggest buyers (Prime funds), shut one key source of short-term USD funding for banks and corporates and triggered a global hunt for dollars.

We expect the dislocation in dollar funding markets to improve over coming weeks. The Fed has addressed the international demand for dollars through new and enhanced USD swap lines with 14 central banks around the world. And more importantly, the Fed is in the process of directly supporting CP through a re-introduction of its Commercial Paper Funding Facility scheme in April. It may take some time for these measures to bear fruit, but the dollar rally on the back of this dislocation looks temporary.

On the second point, the Covid-19 shock has understandably triggered a mass exodus from emerging markets. The amount of portfolio capital leaving emerging markets since late February dwarfs that seen during the summer 2013 'taper tantrum' and looks to match that seen during the GFC crisis.

Sharp repatriation from emerging markets typically sees the dollar rally – on the assumption that dollar-based EM investors who revert to cash or redemptions from those funds need to be repaid in dollars. And looking at the events of the GFC, investors took portfolio (debt and equity) assets out of EM for three consecutive months (Oct-Dec 08) and only felt confident enough returning in April 2009 shortly after the Federal Reserve had expanded quantitative easing to include US Treasuries, and the G20 had ‘saved the world’ with a US$1.1 trillion rescue package, particularly targeted at trade credits.

When will investors feel confident enough to return to emerging markets? One cannot know for sure, but we suspect that investors will selectively return to emerging markets much sooner than they did during the GFC crisis. Though this is an unprecedented shock, policymakers have moved fast to flood the market with liquidity and design fiscal support packages to ameliorate the downturn. Investors will start buying into asset markets well ahead of the low-point in activity. And the Fed’s QE measures to drive investors out of the credit curve also contain the unwritten objective of driving investors out of the dollar.

In short, we think the fast and aggressive policy response will mean that it does not take investors six months to rekindle their interest in emerging markets. Instead, as 2Q20 progresses we suspect flows to emerging markets resume and upside pressure comes off the dollar.

USD funding problems and EM portfolio outflows temporarily lift the dollar

What’s cheap in G10 FX?

As above, some of the biggest casualties against the dollar over the last six weeks have been the commodity currencies. Based on our Behavioural Equilibrium Exchange (BEER) rate model, these now look cheap against the dollar. A slight caveat, however, in that this is a quarterly model and when the next set of terms of trade data is available and lower commodity prices are added in, the commodity segment will not look quite as cheap.

In any case, we would not be looking for the dollar to turn against the commodity FX segment first. Instead, the next move in this cycle should be a dollar depreciation against the defensive currencies such as teh Japanese yen, Swiss franc and euro. In fact, the yen and the franc were net stronger (albeit marginally) against the US dollar in 1Q20, which was quite an impressive performance.

As outlined in our BEER framework below, neither the JPY nor the EUR is particularly expensive against the dollar right now and we can see the USD/JPY and EUR/USD pairs embarking on moves towards 100 and 1.15+ respectively through 2Q20.

Sterling is probably caught somewhere in the middle between the defensive pairs and commodity FX. The UK’s large current account deficit and exposure to the financial sector do not help. But UK Gilts are proving one of the few safe havens in the fixed income world and if the UK’s transition arrangement with the EU is to be extended after all, then GBP/USD should be rallying into the summer as well.

ING's BEER model for medium-term FX valuation against the dollar

Download

Download article2 April 2020

Covid-19: The scenarios, the lockdown, the reaction, the recovery This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more