High rates and commodity exposure preferred in FX

- 15 May

- FX

As the global energy shock continues to unfold, it seems investors are preferring exposure to those currencies with high interest rates and sitting on the right side of the energy import ledger. The euro does not tick either of those boxes, but EUR/USD could be lifted by the rising tide of a weaker dollar

FX volatility has been subdued

Looking across asset classes, it is fair to say that just like equities and credit, FX markets have traded with a ‘glass half full’ mindset. After a brief spike through March, FX traded volatility has sunk back to the lower end of the range seen over the last three years. As always, lower volatility encourages the search for yield and, across both developed and emerging currencies, high yielders are in demand.

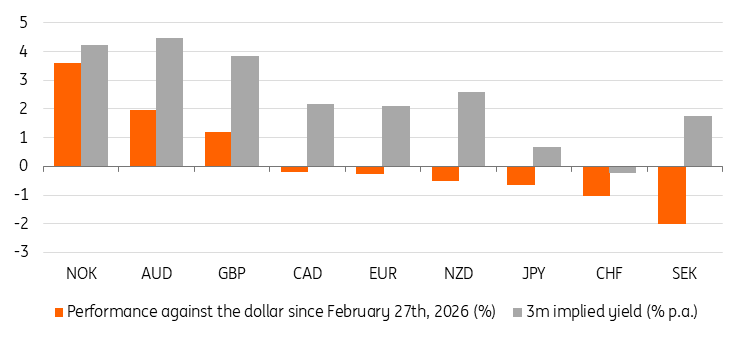

In the developed space, it has seen both the Norwegian krone and the Australian dollar outperform. Not only do both these currencies offer implied yields in excess of 4%, but also net positive exposure to the energy story. Both countries have seen their terms of trade improve markedly over the last eight weeks. And both central banks have already hiked during the crisis and are holding open the door for more tightening. We expect continued strength in these currencies.

At the other end of the spectrum are the low yielders and those threatened with a larger energy import bill. The yen stands out here – especially with the Bank of Japan dragging its feet with rate hikes and leaving real interest rates in deeply negative territory. So far, it looks like the Bank of Japan has sold around $70bn to defend the critical 160 level in USD/JPY. Intervention looks less fundamentally justified than in 2024 (when the Fed was preparing to ease). We suspect this is just the start of a long campaign of the BoJ battling the market at 160.

G10 FX performance against the dollar

What about the dollar?

Somewhat surprisingly, the dollar sits in the middle of the G10 FX pack when it comes to performance over the last eight weeks. In theory, the dollar should have done better given US energy independence and a challenging environment for risk assets. Holding the dollar back has probably been the global equity rally, where correlations between equity gains and dollar weakness are strengthening. That is certainly the case in emerging markets, where investors have held onto the long positions built between last summer and February this year.

We remain bearish on the dollar over a multi-quarter horizon as the Fed will eventually have the opportunity to cut rates back to neutral. We also note very little risk premia priced into the dollar currently – which could change in the run-up to the US Mid-term elections this November. Yet events in Iran will have a big say in the timing of the dollar sell-off. The longer energy prices stay high, the greater chance the Fed will have to sound hawkish in order to ride out the inflation surge. This could help the dollar and hurt risk assets.

For EUR/USD, this warns of further trading near the 1.16-1.18 range through the second quarter. However, the ECB has to hike in June and sound hawkish to keep real interest rates high during this period of elevated inflation. Later in the year, EUR/USD levels above 1.20 remain entirely possible, assuming the global economy can get back on track and the core investment theme of diversifying US risk resumes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Two anniversaries, one uncomfortable mirror

- This bundle contains 13 Articles