Fed hikes 25bp with many more to come

- 16 March 2022

- FX Rates United States

The fed funds rate has been increased 25bp with Federal Reserve officials forecasting six additional hikes this year and the rate peaking at 2.8% next year. Geopolitical tensions create uncertainty, but the Fed feels the need to step on the accelerator and it increases the likelihood we will see the Fed swiflty seek to shrink its balance sheet this summer

Fed goes for a 25bp hike

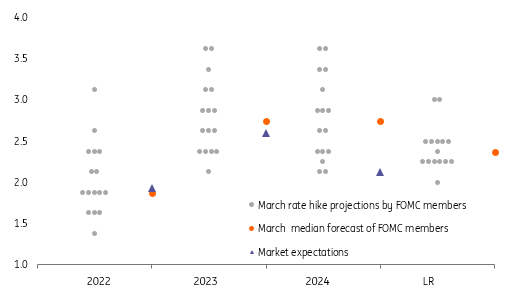

The Federal Reserve has voted to raise the Fed funds rate by 25bp to a range of 0.25-0.5%, which was the firm market expectation following Fed Chair Powell’s March 2nd testimony where he said this is what he would propose and support. It is going to be the first of many with the dot plot of individual FOMC members pointing to six further rate hikes this year, the same as the market. Interestingly, the Fed sees the momentum for higher rates continuing in 2023 with the median projection being for the Fed funds hitting 2.8% with them staying there until 2024 before moving lower to a long-run trend of 2.4% (previously 2.5%).

Fed funds rate and the assets on the Federal Reserves balance sheet ($tn)

A 50bp move in May looks possible

One member of the FOMC wanted a more aggressive 50bp move, namely St Louis Fed Chair James Bullard. He has been the most hawkish member of the Fed for some time and there was likely a lot of sympathy for his position given the economy is growing strongly, is creating jobs in significant number and is experiencing the fastest rate of annual inflation for forty years.

However, “uncertainty” caused by Russia’s invasion of Ukraine was highlighted as a key risk for the economic outlook. It will likely “create additional upward pressure on inflation and weigh on economic activity”, implying it was the key reason for the bulk of the committee backing a smaller hike. Should Russia-Ukraine talks reach a positive conclusion and tensions gradually ease we could see the potential for a 50bp hike in May. Calls for more aggressive, swifter policy tightening would certainly build if inflation remains up around 8%, there is more evidence of a de-anchoring of inflation expectations and the unemployment rate remains below 4%.

Fed dot plot points to aggressive hikes from here

Fed to be "nimble"

There are no guarantees that talks will succeed and there are huge uncertainties about how quickly supply chain strains improve in light of China’s zero Covid strategy, what happens to US domestic labour supply and how energy and commodity prices evolve. How this all then feeds back into economic growth, employment and inflation means that the Fed, as outlined by Chair Powell, will need “to be nimble in responding to incoming data and the evolving outlook”. Likewise, our projections for Fed policy – currently for seven further 25bp hikes – is subject to review and will almost certainly be revised higher.

Fed forecasts show expectations of weaker growth, higher inflation, higher rates

Balance sheet to do its fair share

How far and how fast they go on the policy rate will also be influenced by how aggressive they are in shrinking their $8.9tn balance sheet. The Fed didn’t say much about their plans today other than an annoucnement will soon come. We are currently expecting a June formal announcement with a July start.

As in 2017, this will come via phasing out the reinvestment of maturing assets, although the numbers will be larger than the initial $6bn Treasuries and $4bn agency MBS per month allowed to roll off back then. They eventually got up to $30bn and $20bn per month respectively and given the balance sheet has doubled in size during the pandemic we suspect that is where they could start this time before going up to $60bn and $40bn per month in September.

This would see the balance sheet shrink back down to $8.45tn by year-end and around $7.25tn by end-2023, still nearly double the $3.75tn level it stood at in 2019. That is a lot of notes and bonds that the market would have to absorb, which should apply some upward pressure on Treasury yields across the yield curve, which would translate more directly into higher borrowing costs for corporates and households via mortgage rates, for example.

Flatter curve led by a front end reacting to a 3%-handle in the Fed’s central forecast range

Impact reaction on the bond market has been a marked flattening of the 2/10yr curve, with the largest impulse coming from the rise in the 2yr yield. It’s just short of 2% now, a nod towards the upward revision to the dot plot, one that now features a 3% handle for the funds rate at the upper end of the central tendency range. The 2yr went into the meeting at quite an aggressive discount versus the funds rate anyway, one reminiscent of rate hike cycles that were typical before the great financial crisis, when 50bp hikes were not unusual. The 2/10yr spread is now below 25bp, which is a remarkably flat curve for the very beginning of the rate hiking cycle.

The Fed will be pleased with the fall in inflation expectations following their decision, with for example the 5yr breakeven down by some 10bp, to 3.4%. Real rates have matched that by moving higher, and thereby less negative. The path ahead should see inflation expectations continue to fall and real rates continue to rise. The net outcome should see nominal market rates remain elevated, with a 2% handle the norm right along the curve. The fact that the 30yr rate is now at 2.5% does signal that the debate now is whether a 2% handle can morph to a 3% handle for market rates in the months and quarters ahead. The inflation dynamic suggests yes, but system stability and ability to take rate hikes are key here.

Finally, the Fed also decided to keep things simple by hiking all key rates by 25bp. So not just the funds rate range, but also the rate on excess reserves to 40bp and the rate on the reverse repo facility to 30bp. That range between 30bp to 40bp is where the effective funds rate should sit post today’s hike. It is currently at 8bp. It should settle in the mid 30’s bp post the rate hike. The SOFR rate by the same token should settle at the floor of the funds rate at around 25bp. The Fed could have chosen to under-hike the rate on excess reserve (20bp instead of 25bp) so that it could sit on the funds floor and help take some of the size away from USD1.6bn going back to the Fed on a daily basis. It looks like this will be left to another day.

FX markets: Front-loaded tightening keeps the dollar in demand

The Fed has surprised hawkishly at today’s FOMC meeting. It has effectively matched the hawkish expectations of the market this year and exceeded them for 2023. For us in FX, this looks a clean dollar positive, where the terminal rate for Fed Funds in this cycle continues to be revised higher. That the median of Fed members now see the Fed Funds target range at 2.75-3.00% is remarkable.

The bearish flattening of the US yield curve – typically a mid to late cycle event – would normally start to see the dollar advance a little more against the commodity currencies on the view that the Fed is applying the monetary brakes and that the global economy will slow. Yet one of the many legacies of the tragic events in Ukraine is that commodity markets will probably stay bid for longer and commodity exporting FX will be more insulated than normal.

Instead, expect dollar gains to be expressed against the big fossil fuel importers whose central banks are yet to offer much of a hawkish offset to the Fed. It is therefore no surprise to see USD/JPY leading the dollar advance – a pair also with by far the highest positive correlation to US bond yields. 120 should be tested in short order.

And despite the advance in European FX today on the back of some movement in ceasefire talks, we expect EUR/USD to remain vulnerable. Europe remains at the mercy of the stagflationary shock and now faces a more hawkish Fed too. Francesco Pesole has also published a report today suggesting that the energy supply shock could have done some lasting damage to the Euro’s fair value. For the near term, we doubt EUR/USD will be able to sustain any gains to 1.11 and would not be surprised to see a retest of the 1.08 low.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more