Fed easing and the dollar: Necessary, but not sufficient

- 7 June 2019

- FX United States

There is a conviction that the Fed is going to have to cut rates to insulate the economy from trade wars. US rates are collapsing, but the dollar is holding up reasonably well. We suspect that is due to wide US yield differentials and uncertainty over overseas growth prospects. That said, expect defensive positions to build against the dollar

Markets are convinced the Fed will ease

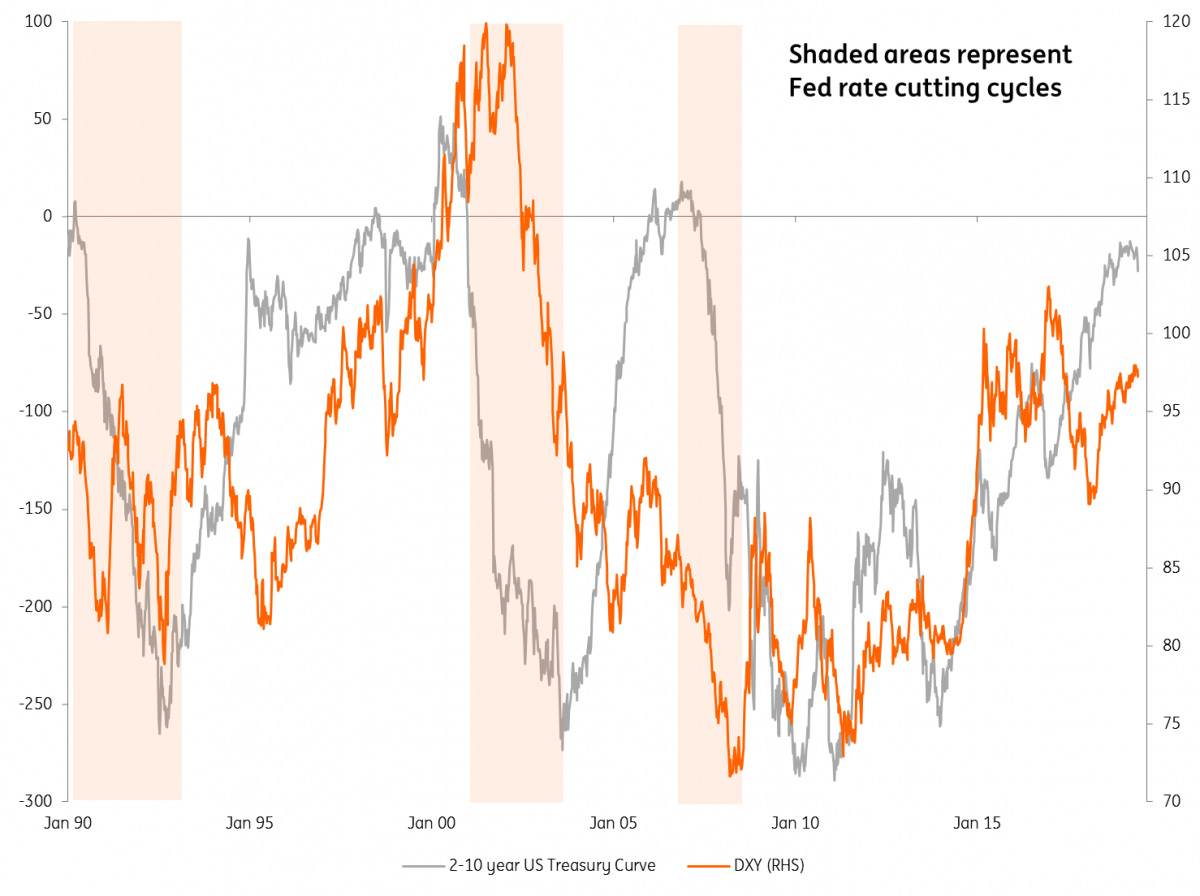

After all the discussion about whether the flat/inverted US yield curve portends the next US recession, it now seems the market is convinced that the Federal Reserve has to act. Beyond the aggressive pricing of Fed cuts (67bps by the end of 2019 and another 33bp by end 2020), we are starting to see a clear, bullish re-steepening of the US 2-10 year Treasury curve.

After all the discussion about whether the flat/inverted US yield curve portends the next US recession, it now seems the market is convinced that the Federal Reserve has to act

During the last three major Fed rate cutting cycles this curve steepened around 250bp as reflationary Fed policy filtered through the market. Typically a weaker dollar plays a role in reflationary US policy, but its decline is not always immediate. In particular, 2001-02 saw the dollar stay temporarily supported even as US interest rates crumbled.

What will it take to sink the dollar now? We think a dollar decline will have to come through two clear, but related channels: i) interest differentials and ii) growth differentials. The former drives fundamental FX hedging (corporates) and investment (FX reserve manager) decisions. The latter drives broader portfolio (debt and equity) allocations and at some point will pressure-test widening US deficits, commonly seen as the Achilles heel of the dollar.

Bullish re-steepening of the US curve is normally a dollar negative

When will yield differentials hit the dollar?

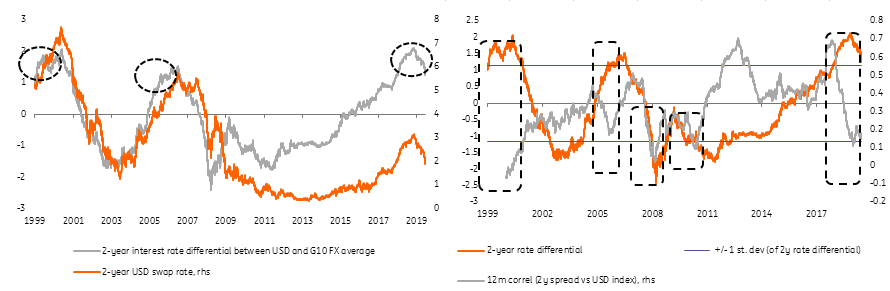

Despite the material decline in US Treasury yields and the US – G10 FX rates spread, dollar losses have been fairly muted. The dollar is down by 1.1% against G10 FX basket (equally weighted) and 0.9% against the euro since 27th May (with UST yields down by 38bp). The limited reaction of the dollar here is partly explained by the historically low correlation of the dollar crosses to the interest rate differential. This phenomenon has been in place for the past few quarters.

In our view, the low correlation of USD crosses towards interest rate differentials is currently due to the simple fact that US rates are still significantly above those of its peers

In our view, the low correlation of USD crosses towards interest rate differentials is currently due to the simple fact that US rates are still significantly above those of its peers. Even though US rates have fallen, the differential remains very high which in turn reduces the need for investors to rotate from the still high yielding dollar. For the private sector, it means that it is still too expensive to hedge US investments and USD receivables. For FX reserve managers, US 2-5 year yields are still well above those available in other high-grade sovereigns.

In the right-hand figure below we show that when the USD-G10 FX interest rate differential reaches extremes versus its historical standard deviation bands, the sensitivity of the dollar crosses to it declines. As per above, if the rate differential is too high, even a decent decline (from a very high starting point) doesn’t make it attractive for investors to rotate meaningfully out of the USD. Equally, when the rate differential is substantially negative, even some marginal increase in the dollar’s favour is not meaningful enough for investors to go long USD.

We estimate that the market would have to price in one more (independent) 25bp cut by the Fed (while keeping interest rate expectations for cuts for the G10 peers unchanged) for the current rate differential to fall into the one standard deviation band and two independent cuts for the rate differential to be comfortably within this band. Only then is the dollar likely to react more meaningfully (on the negative side). This suggests then that the bar for a more meaningful USD decline remains high, at least from the rate point of view.

USD yield differentials narrowing, but still near extremes

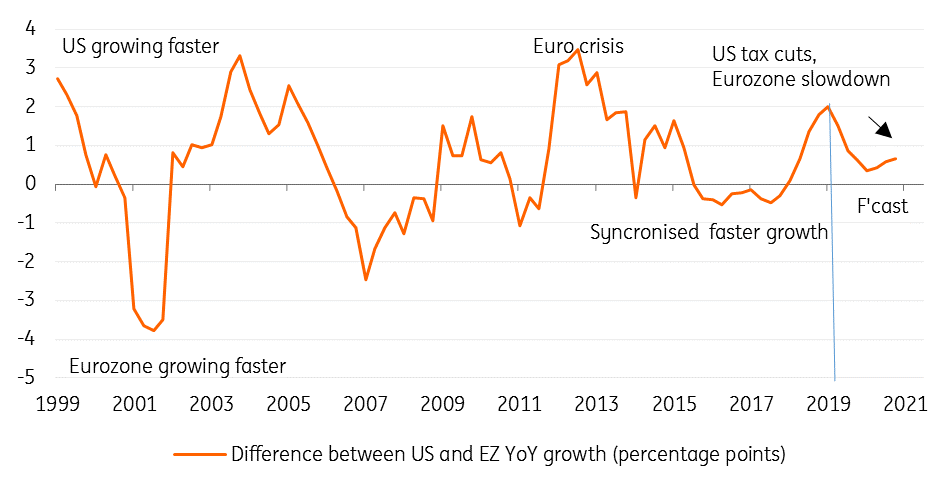

The jury's out on growth differentials

As we highlighted in early May, 5 Reasons why we’re medium term EUR/USD bulls, we feel growth differentials will turn against the dollar over the next couple of years. Yet the conviction levels on this story right now, especially US versus European growth, are low given the nature of the current shock - trade wars - and the eurozone being a very open economy (one of the most open in the G10 FX space). This and the delicate position in European politics - think Italy and Brexit suggest the EUR will struggle to fully participate in a dollar decline – even if the Fed were to deliver an early easing cycle.

Our eurozone macro team also highlight the risk of the Eurozone’s ‘Japanification’, which may limit the ECB’s scope to hike rates. This recalls the events of 2000-2001 when fears over ‘eurosclerosis’ prevented EUR/USD from immediately participating from the collapse in dollar rates as the US Dot Com bubble burst.

For this reason, we're in no hurry to revise our end 2019 EUR/USD forecast of 1.15.

US versus Eurozone growth differential: peaking?

Defensive positions against the dollar

Even though short term US interest rates already deeply discount a Fed easing cycle and may not go that much lower in the short term, we still expect the market to adopt defensive positioning against the dollar. We say this because our trade team’s baseline view is that the US trade war with China and the EU will escalate over the next three to six months. We suspect that means that US recession fears will build.

Given the risks, we expect investors to increasingly look to express a bearish dollar view via USD/JPY. Also expect the CHF to remain in demand

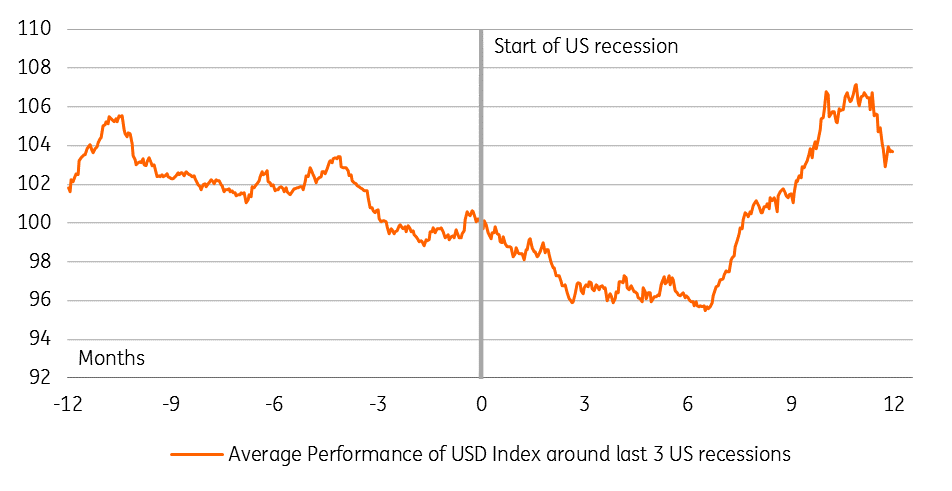

If the above is indeed the case, investors will want to position defensively against the dollar. In particular, historical analysis of the USD trade-weighted index performance around the last three recessions (1990, 2001 and 2008) suggests that - on average - the greenback peaked around 11 months before the start of the economic downturn. Then, the dollar index gradually decreased in value and bottomed around seven months into the recession. As noted above the dot-com bubble crisis in 2001 represents an exception.

Given the risks, we expect investors to increasingly look to express a bearish dollar view via USD/JPY. That means USD/JPY could be trading at 100 far earlier than the late 2020 window in our current forecasts. We also expect the CHF to remain in demand – especially if the risk of Italian elections and auto tariffs emerge this autumn. This will keep the Swiss central bank busy intervening to hold EUR/CHF above 1.10/11, but could see dollar pessimism evolve into a preference for short USD/CHF positions should EUR/CHF surprise the market and break under 1.10.

USD index performance around last three US recessions

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

What’s happening in Australia and the rest of the world?

- This bundle contains 8 Articles