Eurozone still set for divergence despite fiscal support

- 20 April 2021

The chances of a swift recovery remain in favour of the old “core” eurozone countries, while the periphery remains at risk of a prolonged slump. The EU recovery and resilience grants do seem to target the countries most in need, but are unlikely to fully prevent further divergence

In June last year, we took a look at which eurozone countries would be most vulnerable to a prolonged slump. This analysis examined how deep the crisis could become and the factors that play a role in the speed of the recovery. With the economy set to rebound in the second quarter, as the vaccination pace picks up significantly, we deemed this a good time to take another look at the vulnerabilities - this time to determine which country is most at risk from a weak recovery after the initial reopening bounce.

We update our index with the latest insights on economic developments, taking the depth of the crisis as a given and looking ahead to factors like sectoral vulnerability, fiscal stimulus withdrawal, labour market developments, structural strengths and the savings build-up over the course of the crisis. The aim is not to predict which countries experience the quickest or strongest rebound when economies reopen, but to see which countries are expected to fully recover the quickest.

Again, the northern eurozone economies are set to perform best

Our Vulnerability Index, which measures the risk of a weak economic recovery, shows that the traditional North-South divide in terms of economic strength is very apparent. That was already the case when we did the exercise last year and remains the case now that more information about the nature and depth of the recession has emerged. Those with improved prospects are the Eastern European eurozone countries, which have much lower GDP declines than expected and also score well on newly-included variables. Scoring more negatively is Austria, which ranks the lowest of the core countries in terms of GDP impact so far but also scores poorly on fiscal support and increased savings while being more exposed sectorally to prolonged restrictions.

The risk of delayed recession effects is key for the recovery phase

While the countries with a sharper decline in GDP in 2020 could experience a stronger short-term rebound, the risk of a longer recovery phase back to pre-crisis levels gives rise to substantial negative side effects. Northern economies have performed better so far. Economies like Ireland, Luxembourg, Finland and the Baltics have closed the gap or are very close to pre-pandemic levels, while the southern eurozone economies are still around -6% or worse compared to pre-pandemic levels. While a rapid bounce back is possible, the risk of a longer recovery and more lasting damage to the economy is far larger for countries that have experienced a deeper downturn.

Think of the potential increase in bankruptcies. Currently still at historic lows in most eurozone countries, the risk of a significant increase at the end of the crisis seems higher in most peripheral eurozone economies. The ones that stand out are Spain, Portugal, Italy, Greece, Slovakia and Latvia. The sectoral composition of their economies works against them, with a larger percentage of GDP impacted by lasting lockdowns than in the core eurozone economies. The share of SMEs in the economy is also higher on average, and the financial position of corporates was weaker on average moving into the crisis, resulting in an overall higher risk of businesses struggling even when economies have reopened. The share of vulnerable workers is also larger for most periphery countries, which leads to increased worries about higher unemployment when furlough schemes end.

Government support will boost weaker economies, but will it be enough?

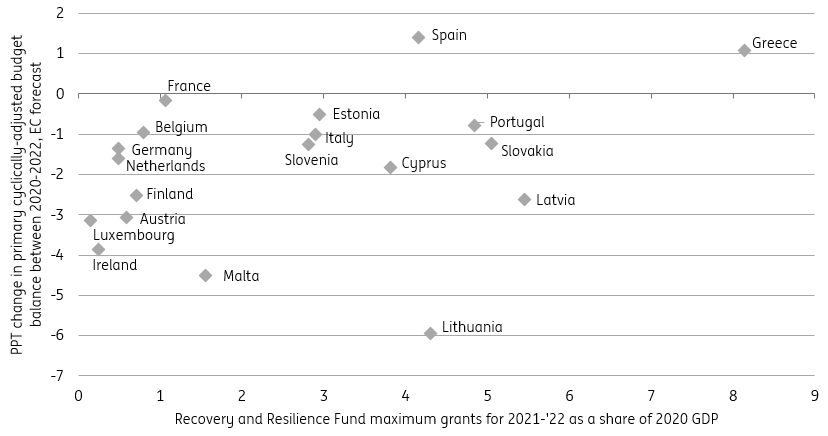

The big mitigator for reopening risk is fiscal stimulus. Stimulus packages have so far mainly focused on immediate crisis fighting, but a cold turkey withdrawal is likely to lead to the effects described above, which would prolong the economic slump. Across eurozone economies, budget plans have so far been more modest for 2021 and 2022 compared to 2020, meaning that budget deficits are set to fall. This puts the eurozone at risk of falling behind countries like the US that have put ample stimulus in place for the recovery phase, but there are differences between countries in the degree of stimulus provided for the coming years. The good news is that stimulus is set to be withdrawn the fastest among the better performing countries, while the weaker economies will leave accommodative policy in place for longer. The same holds true for the recovery fund, which is set to benefit weaker economies more substantially than the stronger ones. This mechanism is therefore set to generate some form of convergence in terms of recovery prospects.

Most vulnerable countries are set to benefit from a larger fiscal impulse

But structural forces weigh on recovery prospects for the periphery

The chances of going right back to the old normal seem low at the moment. A transition phase is likely, which works against peripheral economies. The digital readiness of core countries remains far better, which boosts working from home prospects and helps serve economies that have shifted more online. In addition, tourism is unlikely to see a full recovery by the summer. Clearly, this is more important for the peripheral economies and the ones more dependent on summer holidays than the ones dependent on winter holidays like Austria. Nevertheless, all tourism related activity is likely to remain uncertain for some time, causing extra risk of prolonged weakness.

The risk of divergence increases despite fiscal efforts

Despite historic efforts by European leaders to boost convergence in terms of economic recovery, it does look likely that the structurally stronger economies are moving further away from the weaker ones. This doesn't mean there is no convergence to be seen; the surprising performance of the Baltics indicates that there will probably be ongoing convergence between the core countries and the newer participants of the monetary union. The problem lies more with some of the weaker performing southern economies, which are at risk of falling further behind.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more