EUR: ECB making EUR a well-behaved passenger vs USD and GBP

- 4 June 2020

- FX

The ECB delivered and the €600bn PEPP expansion further helped to stabilise EUR. The euro risk premium is currently no longer an issue. If anything, EUR seems to be modestly front running its short-term fair value. The positive ECB effect on EUR now seems exhausted, with further EUR/USD and EUR/GBP gains to be driven by issues USD and GBP are to face

The ECB delivered and further stabilised the euro …

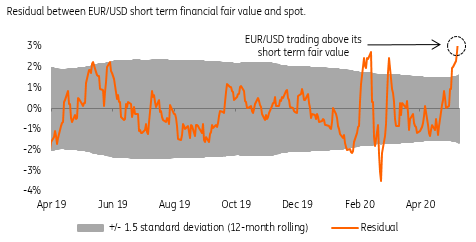

The ECB delivered and increased the Pandemic Emergency Purchase Programme (PEPP). The top-up was modestly higher than expected (€600bn announced vs €500bn expected) and the announcement that PEPP reinvestments will run until at least end-2022 is also seen as positive (see ECB Review for more), as both ensured a limited scope for a risk premium to return into the euro and the euro-denominated assets. However, as the euro has already been trading rich vs its short-term fair value (Fig 1), we see scope for further ideosyncratic euro gains as limited. In our view, and as we argued in the ECB Crib Sheet, the newly announced ECB measures are to have more of a stabilising effect on the common currency and should prevent euro weakness.

Figure 1: EUR/USD front running its short-term fair value

… but any further ECB induced EUR strength is unlikely any time soon

While the ECB is preventing an idiosyncratic EUR decline, its new set of forecasts also suggests that an ECB induced EUR strength is unlikely any time soon. The inflation forecast has been surprisingly downgraded throughout the forecast horizon and with the 2022 forecast pencilling CPI at 1.3% (well below the 2% target) the prospects of any monetary normalisation are almost non-existent at this point. Recall this was the key driver of EUR/USD in 2017 when the cross rallied largely on the back of the ECB QE tapering expectations.

Bearish USD and GBP prospects the key for more upside to EUR/USD and EUR/GBP

With the domestic induced EUR rally unlikely, we continue to see the continuation of the USD bear trend as the main driver of the expected EUR/USD upside. Indeed, the post ECB break in EUR/USD above 1.1300 coincided more with the renewed broad-based USD weakness rather than EUR strength (with the likes of NOK, SEK and CEE FX appreciating against EUR). We see EUR/USD above 1.15 this summer.

We see EUR/USD above 1.15 this summer.

The same dynamics also apply to EUR/GBP where the GBP side of the cross should be the main driver of the pair. As per Brexit returns as major headache for the pound, we target EUR/GBP 0.91 by end-June as the likely limited progress in the UK-EU trade negotiations and the no extension of the transition period should translate into further built up of risk premium into GBP.

For both EUR/USD and EUR/GBP near-term journeys, the euro shall remain a relatively well behaved passive passenger, more attractive than its more ugly two partners (USD and GBP), which are to actively decline.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more