EUR & ECB Crib Sheet

- 2 June 2020

- FX

The expected €500bn top-up to the ECB's PEPP should have a further stabilising effect on EUR, keeping the currency’s risk premium in check. But with EUR/USD trading modestly overvalued on a short-term basis, more is needed to push EUR/USD meaningfully higher. The main driver of further EUR/USD gains should be the unfolding dollar bear trend

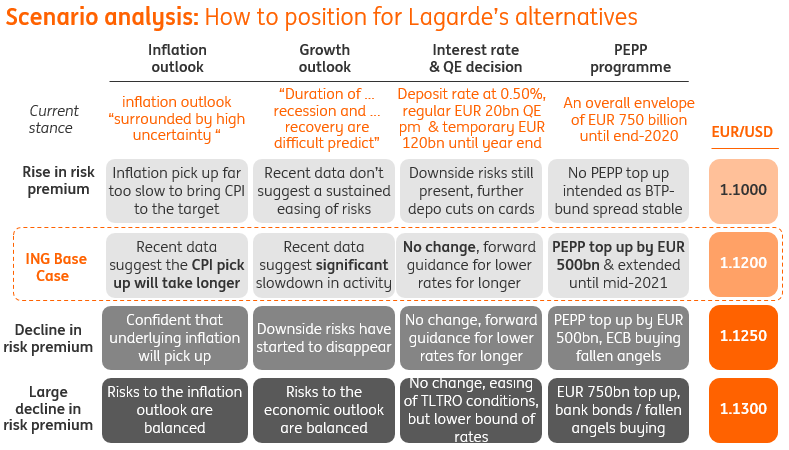

The top-up to the PEPP programme the main factor for the euro

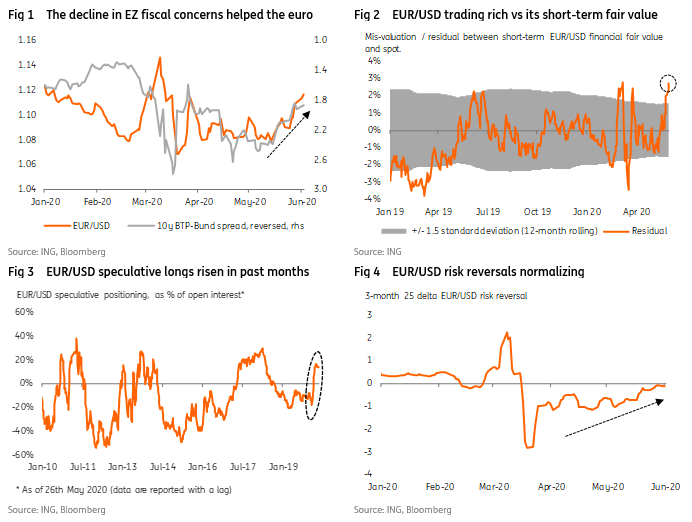

The main focus on the June ECB meeting (this Thursday) will be the expected increase in the size of the Pandemic Emergency Purchase Programme (PEPP). As per ECB Preview, we expect an additional €500bn top-up, to be spent until mid-2021. As has been the case since the start of the Covid-19 crisis, the ECB balance sheet expansion has not been seen as negative for EUR as the accompanying asset purchases and the subsequent stabilising effect on peripheral bonds has had a reducing risk premium effect on EUR, in turn benefiting the currency (Fig 1). The same should be the case this week.

EUR trading on the expensive side vs USD on a short-term basis

The €500bn PEPP top-up is the consensus expectation, meaning that its impact on EUR/USD should be limited. The prime upside risk stems from a possible larger top-up (ie, €750bn +) but this is not our base case. We also note that following (a) the ECB risk premium stabilising steps and the generous EC proposal on the Next Generation EU plan, and (b) the broad-based USD weakness of late, the EUR/USD trades in an overvalued territory based on our short-term financial fair value model (Fig 2). This may tamper a meaningful EUR/USD upside even if the ECB surprises with a more forceful PEPP response (ie, €750bn expansion vs €500bn expected).

Positioning and the option market show an improved sentiment towards the euro

The improvement in sentiment towards the euro is also apparent in the speculative positioning, which has increased sharply since the peak of the Covid-19 crisis (Fig 3) as the speculative community has pre-positioned for the USD bear trend. The option market also shows an improved sentiment towards EUR as EUR/USD risk reversal continues grinding higher (Fig 4) since the peak of the USD funding squeeze in mid-March.

USD bear trend the key driver for further EUR/USD gains

Still, with the ECB firmly containing risk premium in both the euro and peripheral bonds (the current level of 10y BTP being the case in point), this should allow for an ongoing move in EUR/USD higher in months to come as the USD bear trend extends further. The broader USD weakness already unfolded in recent weeks (see USD: Wake up and smell the (bearish) coffee) and with the USD no longer benefiting from its key advantage of past years (the vanished interest rate differential), more weakness is to come in 2H20.

But unlike the profound EUR/USD rally in 2017, this time the cross’ upside should be driven by the weak USD dynamics, rather than strong EUR. The ECB keeping the euro risk premium in check is a necessary condition for higher EUR/USD, but on its own it won’t lead to a meaningful appreciation of the cross in the absence of the ECB policy normalisation (which is highly unlikely any time soon). The weak dollar environment must do its part and we see EUR/USD breaking above 1.15 this summer.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more