EUR & ECB crib sheet: Euro may stay offered amid optionality conundrum

While unlikely to deliver any true policy action, the April ECB meeting could see President Lagarde giving some colour about the different policy options. We expect a reiteration of the current APP buying schedule, with the end-date set for 3Q. Market expectations are leaning on the hawkish side and might be disappointed, leaving the euro vulnerable

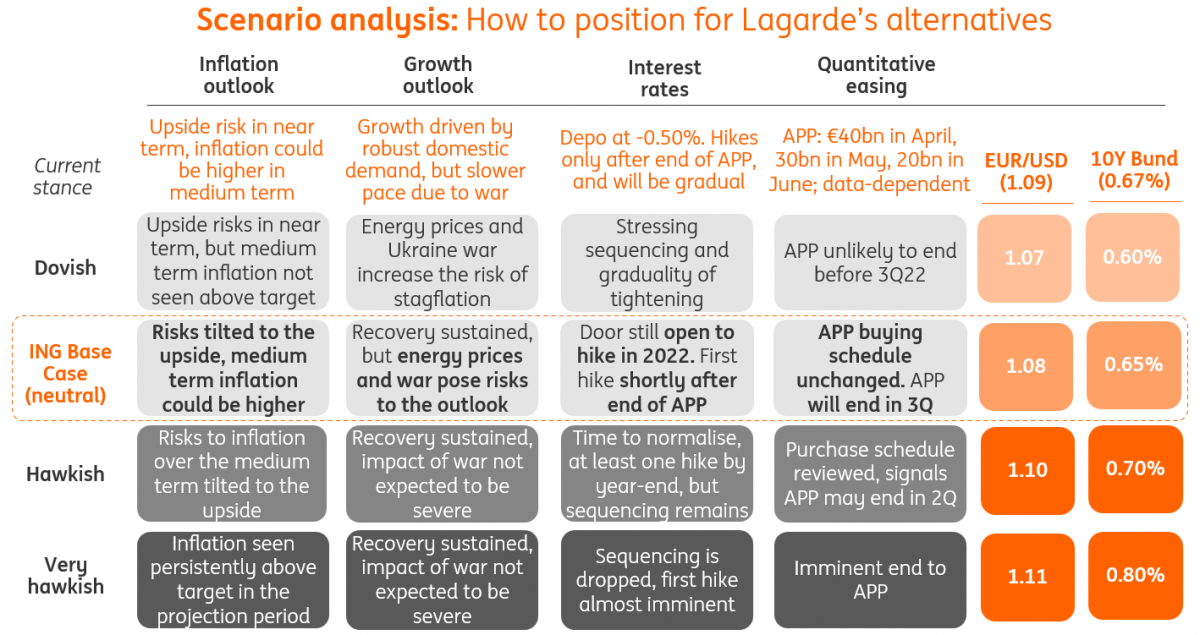

Four different scenarios

What to expect from the April ECB meeting

The ECB April meeting should not be one for major policy shifts, given the lack of hard data to judge the impact of the Ukraine conflict on the eurozone’s economy and lingering uncertainty around how the war will evolve. In our view, reiterating the Asset Purchase Programme (APP) scheduled reduction announced in March (€40bn in April, €30bn in May, €20bn in June), with a somewhat firmer commitment to end APP after June, as well as data-dependency, appears the only viable option for now.

President Christine Lagarde may, however, need to add some colour about the different policy scenarios ahead or even reduce the spectrum of optionality to fewer options. Still, as long as the notion of sequencing (hikes only after the end of APP) is reiterated and the plan for reduction in net purchases is kept unchanged, we doubt markets will be able to extract much hawkishness out of this meeting.

We explore different scenarios and the potential impact on the FX and rates market in the graph below. The forecasted levels for EUR/USD and 10Y Bund yields are based on the assumption that both trade at current levels in the morning of the ECB meeting.

EUR: ECB unlikely to offset other bearish factors

In the run-up to the ECB meeting, markets are pricing in around 115bp of monetary tightening over the next 12 months. This likely embeds some expectations about a hawkish tilt in the policy message this month. As discussed above, we do not expect many changes in the policy stance, and the risks are skewed towards a slightly dovish surprise compared to market expectations.

From an FX perspective, this means that the ECB may not come to the rescue of the euro, which is currently suffering from: a) its low-yielding character, at a time of sharp Federal Reserve hawkish re-pricing; b) fresh EU sanctions on Russia, which targeted energy exports (coal) for the first time; c) uncertainty around the French elections, as discussed in this note.

Despite many negative factors piling up, EUR/USD is not showing signs of undervaluation in the short-term (chart below), which is mostly due to the recent widening of USD-EUR short-term rate differentials on the back of rising hawkish bets on the Fed.

EUR/USD is not showing signs of undervaluation

Incidentally, the shock to the eurozone’s terms of trade caused by high energy prices has depressed the medium-term real fair value of EUR/USD.

All in all, we do not expect the ECB to deliver a hawkish enough statement to offset the unsupportive external environment and valuation of the euro. Our view is that a sustained recovery in EUR/USD is not on the cards in the current environment, and we expect the pair to trade in the 1.05-1.10 range into the summer months.

For our detailed European Central Bank meeting preview, please see: "How the ECB will spell optionality this week".

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more