EMEA FX Talking: Carry dominates fiscal concerns

- 15 September 2025

- FX Talking

Relatively high yields in the CEE region and ongoing interest in the carry trade mean that local currencies continue to perform well despite ongoing and new fiscal concerns in Hungary and Poland, respectively. We continue to prefer the Czech koruna in this environment. Carry traders look set to hold onto the Turkish lira for another month as well

Main ING EMEA FX Forecasts

| EUR/CZK | EUR/PLN | EUR/HUF | ||||

| 1M | 24.40 | ↑ | 4.25 | ↑ | 400 | ↑ |

| 3M | 24.35 | ↓ | 4.25 | ↑ | 403 | ↑ |

| 6M | 24.25 | ↓ | 4.25 | ↑ | 408 | ↑ |

| 12M | 24.20 | ↓ | 4.27 | ↑ | 410 | ↑ |

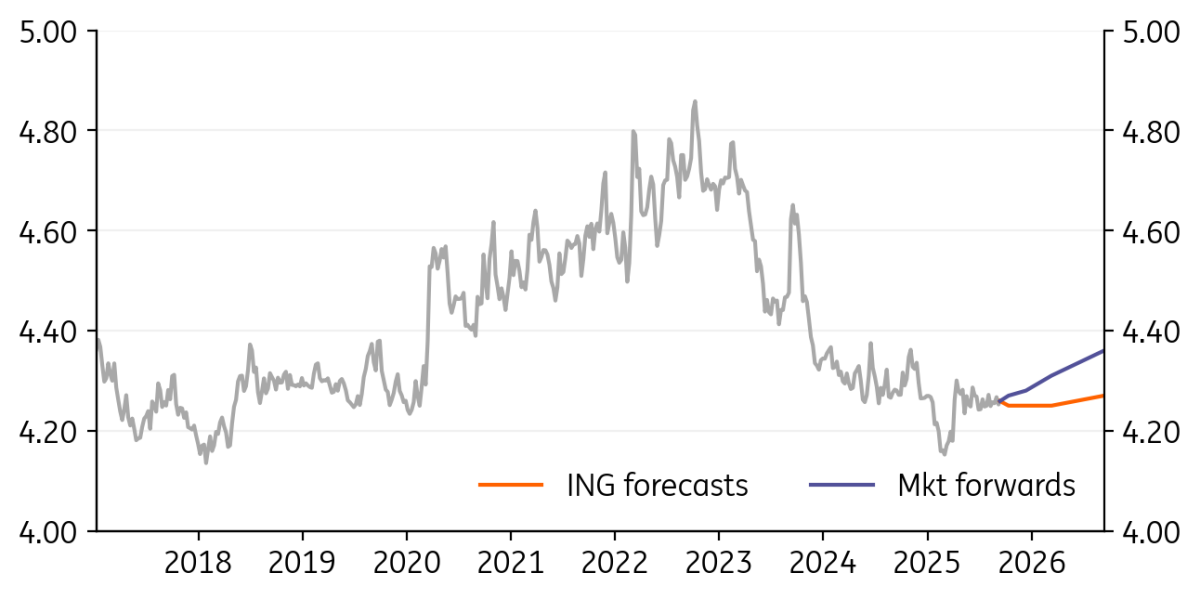

EUR/PLN: Rock-solid zloty

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.26

|

Neutral | 4.25 | 4.25 | 4.25 | 4.27 |

- As the global FX market (EUR/USD) remained stable over the past few weeks, the Polish zloty was stable in a range-bound trading (4.20-4.30). Neither signs of US labour market weakness, rising political risk in France, nor mounting threats from the Trump administration to the Fed’s independence triggered any significant market movements.

- The unexpected revision of Poland’s rating outlook (to negative) by Fitch, recent Russian military provocation, and a deteriorating fiscal position turned out insufficient to trigger a substantial sell-off of the zloty. The Polish currency remained resilient and stable.

- Still, a positive carry trade remains the main argument for PLN strength, along with a bit less dovish post-summer MPC rhetoric. The fundamentals of the domestic economy remain stable, with a solid growth outlook clearly outperforming the rest of the CEE region.

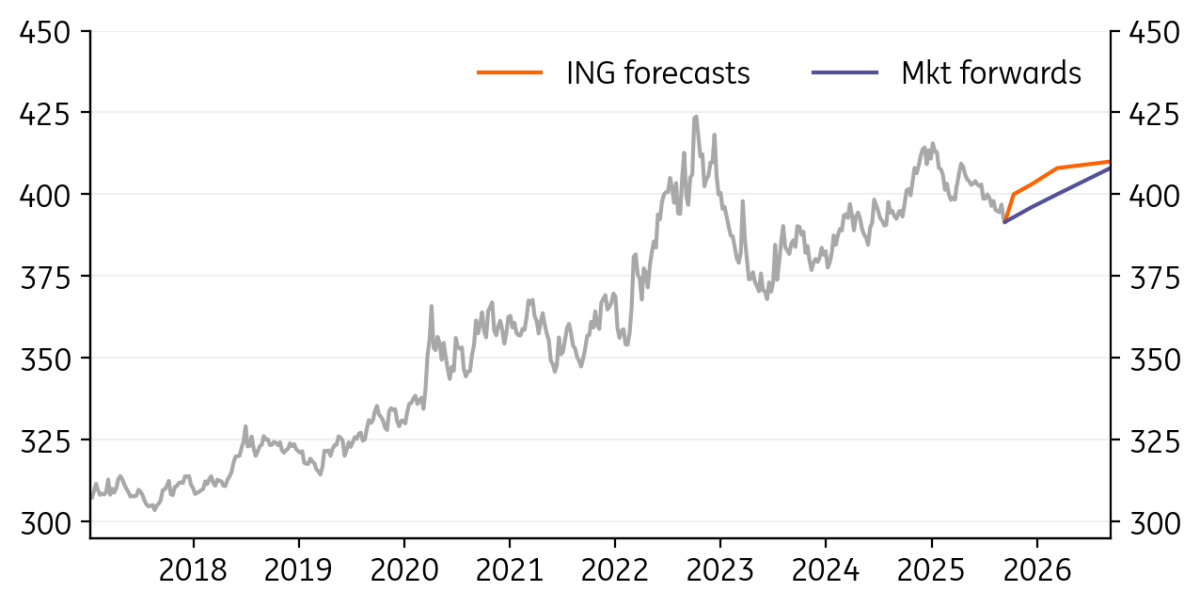

EUR/HUF: Sentiment can quickly turn against the forint

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

391.51

|

Bullish | 400.00 | 403.00 | 408.00 | 410.00 |

- The Hungarian forint had an unusually strong summer, with the EUR/HUF exchange rate falling to 392 by early September. This is not a surprising development; the dollar has gradually weakened, combined with a high-risk premium on local interest rates.

- While positioning is becoming increasingly crowded, we are slowly but surely eyeing a level that could prompt some market players to consider a shift in monetary policy towards opportunistic easing, which could turn the tide for the forint.

- But other risks are looming, too. We think these will eventually lead to a change in trends. Fear of further fiscal spending and uncertainty surrounding the upcoming general election in spring 2026 are favouring a bearish turnaround in the forint.

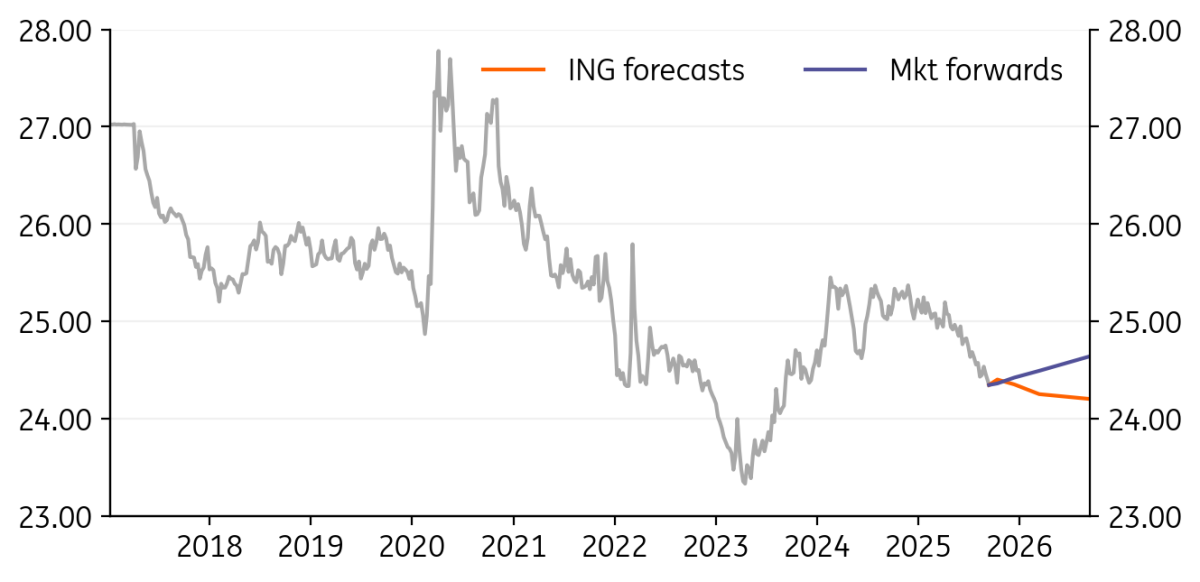

EUR/CZK: Increasing real rates differential supportive for CZK

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

24.34

|

Neutral | 24.40 | 24.35 | 24.25 | 24.20 |

- The Czech economic expansion is entering a more solid ground, with consumption, construction, and the recent rebound in industry providing support. The labour market is expected to shift into a re-tightening mode in early next year, creating a favourable milieu for robust wage increases, with wage dynamics becoming a candidate for upward surprises in 2026. Such a setup, along with persistent price growth in the service sector and upward inflation risks associated with the 2027 ETS2 implementation, suggests that the rate-cutting cycle is over. Rate stability is the optimal take for now; however, we see risks to both higher inflation and rates, stemming from the red-hot housing market and upbeat spending on services.

- With that in mind, the Czech real interest rate of 1% in August makes the koruna an attractive asset to hold. Meanwhile, the real rate for the euro drifted to zero in the same month, making the rate differential pretty punchy in real terms. Understandably, we view such a setup as beneficial for holding the koruna, and we stand on its side with an outlook for further gradual gains vis-à-vis the single currency. That said, the US real interest rate has only gradually softened to 1.6% in August, and we expect more stability in USD/CZK looking ahead.

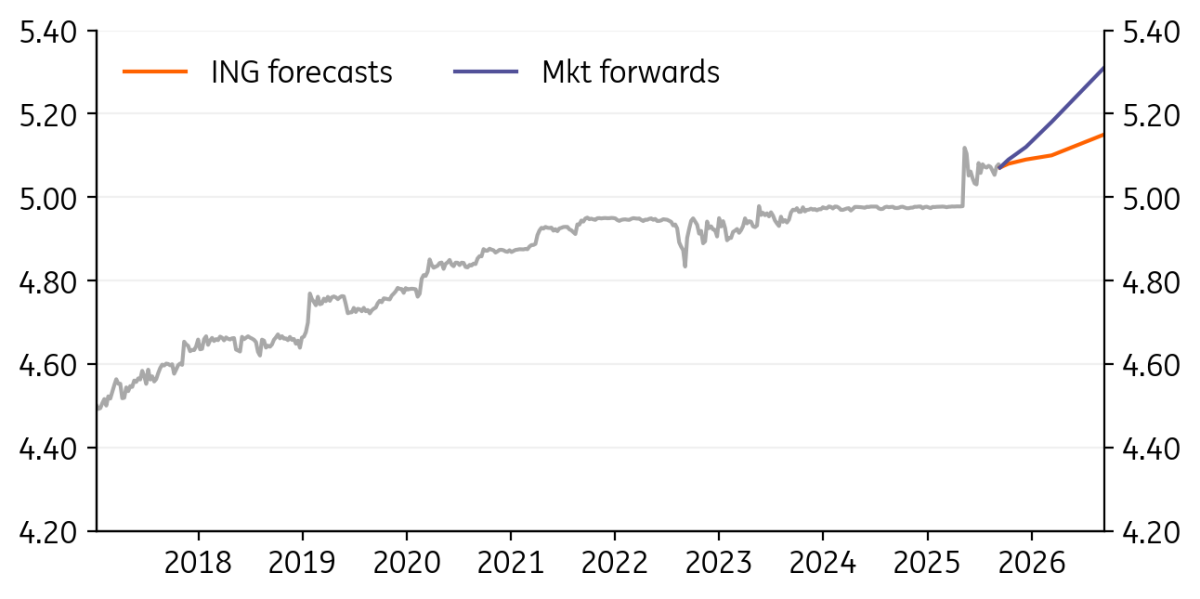

EUR/RON: No sharp moves in sight for EUR/RON

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

5.07

|

Neutral | 5.08 | 5.09 | 5.10 | 5.15 |

- EUR/RON has remained stable in the range of 5.05–5.08, carrying on with what looks like a consolidation period. The catalysts for stronger developments on the pair have been limited so far, and volatility has remained low in September.

- Further fiscal reforms and governing stability remain key ahead for the rating agencies, as well as the country’s ability to mitigate its structural imbalances through the medium term. The current slowdown in consumption could take a toll on budget revenues, but on the flipside brings lower depreciation pressures stemming from trade developments.

- Given the recent inflation spike, we think that the National Bank of Romania will keep the key rate unchanged at 6.50% until the second quarter of 2026, and we expect policymakers to continue to hold a firm grip on the currency, with short-term moves contained within the 5.05–5.10 band and the pair ending the year near 5.10.

EUR/RSD: Dinar stability to remain in place through the near term

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.14

|

Neutral | 117.21 | 117.20 | 117.19 | 117.18 |

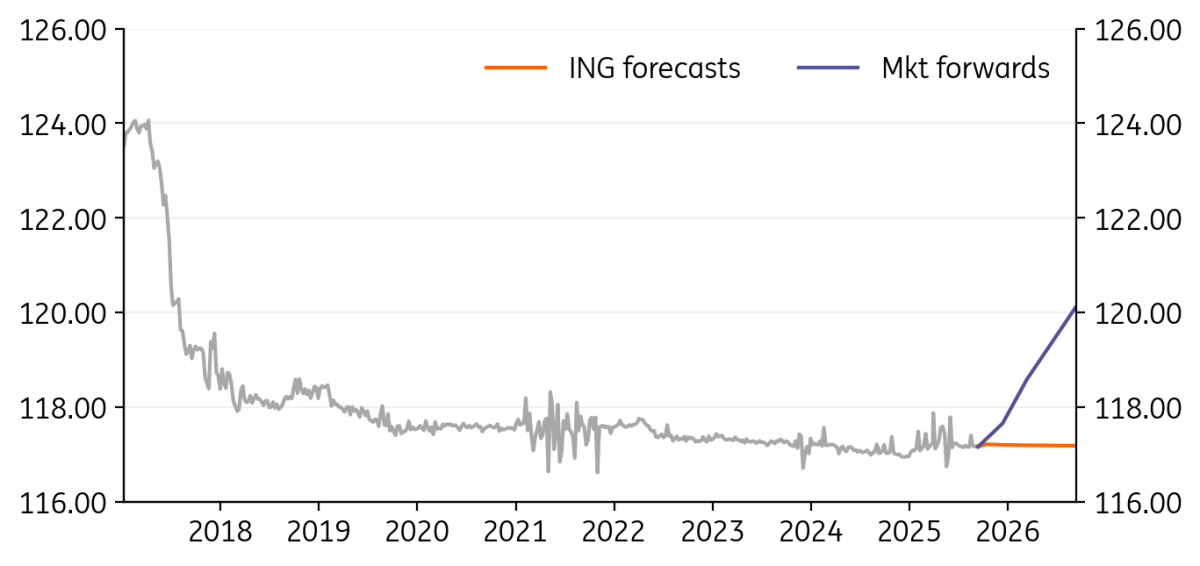

- EUR/RSD continued trading in a tight 117.10–117.20 range through early September. At this stage, Serbia retains its robust macro fundamentals position, with continuous infrastructure development and prudent fiscal policy taking centre stage.

- At its September meeting, the National Bank of Serbia held the key policy rate steady at 5.75%, choosing again to remain cautious in the wake of still-high global uncertainties. Headline inflation picked up to 4.9% in July, going even further outside the NBS’s 3±1.5% target band.

- We continue to expect FX stability to remain a key focus for the Bank moving forward. Moreover, the country’s strong macro fundamentals should prevent policymakers from having major difficulties in maintaining the pair around the current levels in the near term.

USD/UAH: Further stabilisation for the hryvnia

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

41.28

|

Mildly Bullish | 42.00 | 42.00 | 42.00 | 42.00 |

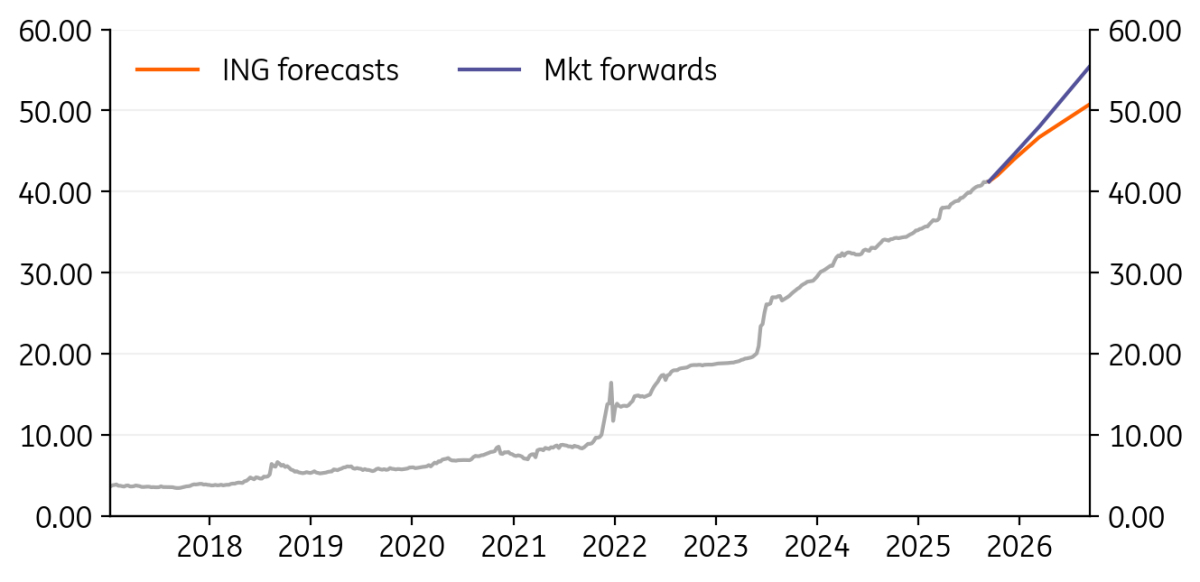

- The hryvnia exchange rate against the dollar remained broadly stable for another consecutive month (a tight range of 41.0-41.8), partly due to the National Bank of Ukraine’s previous efforts to tighten monetary policy – the key policy rate was raised by 250bp in less than a year – but also thanks to the inflows from international aid.

- Despite the ongoing war and the failure of peace talks between the US and Russia, the Ukrainian economy is slowly improving. According to the NBU, economic growth is recovering and inflation is stabilising, while leading indicators point to a gradual improvement and adaptation to geopolitical uncertainty. As a result, the hryvnia is also supported by improving economic fundamentals.

USD/KZT: Signs of stabilisation after mid-summer weakness

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

540.77

|

Mildly Bearish | 530.00 | 535.00 | 540.00 | 550.00 |

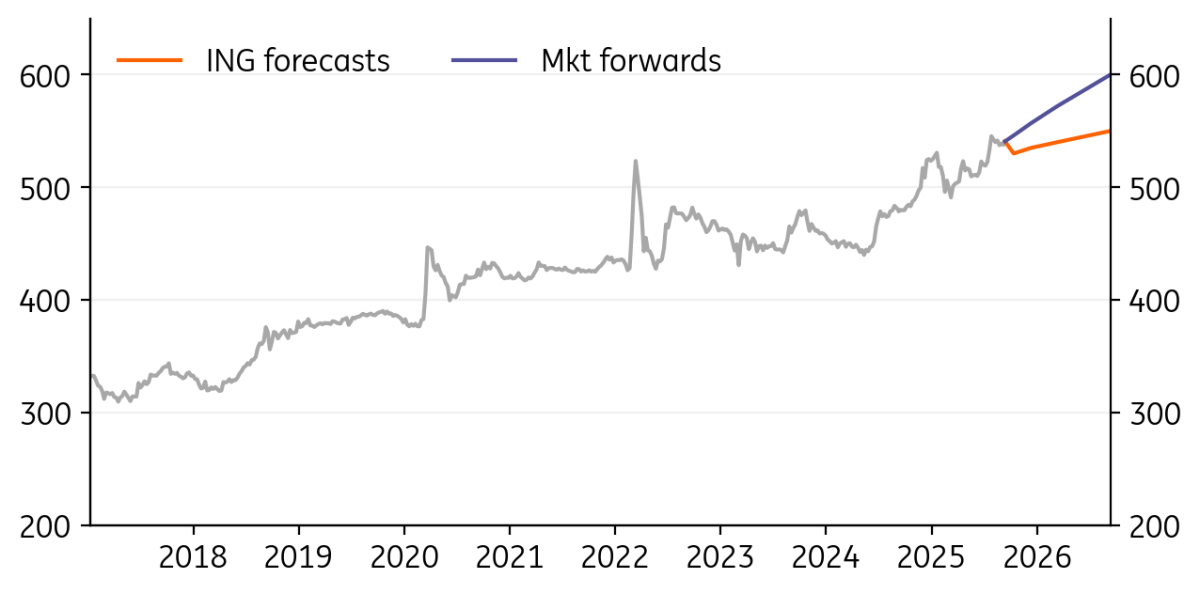

- The tenge appreciated by c.1% to 535-540 per US dollar. Although this slightly falls short of our near-term expectations, the general direction aligns with our view that, following summertime weakness, the tenge should eventually find support from the recent double-digit growth in oil production and exports.

- Net FX sales by the government and the National Bank of Kazakhstan are expected to amount to around $1bn in September, slightly higher than the August volume. This suggests moderate support for the FX market.

- The recent pick up in CPI to 12.2% YoY in August exceeds the NBK’s expectations, meaning a high likelihood of a hike in the key rate from the current 16.50% at the upcoming meetings.

USD/TRY: Real currency appreciation likely to continue

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

41.24

|

Mildly Bullish | 42.00 | 44.00 | 46.70 | 50.80 |

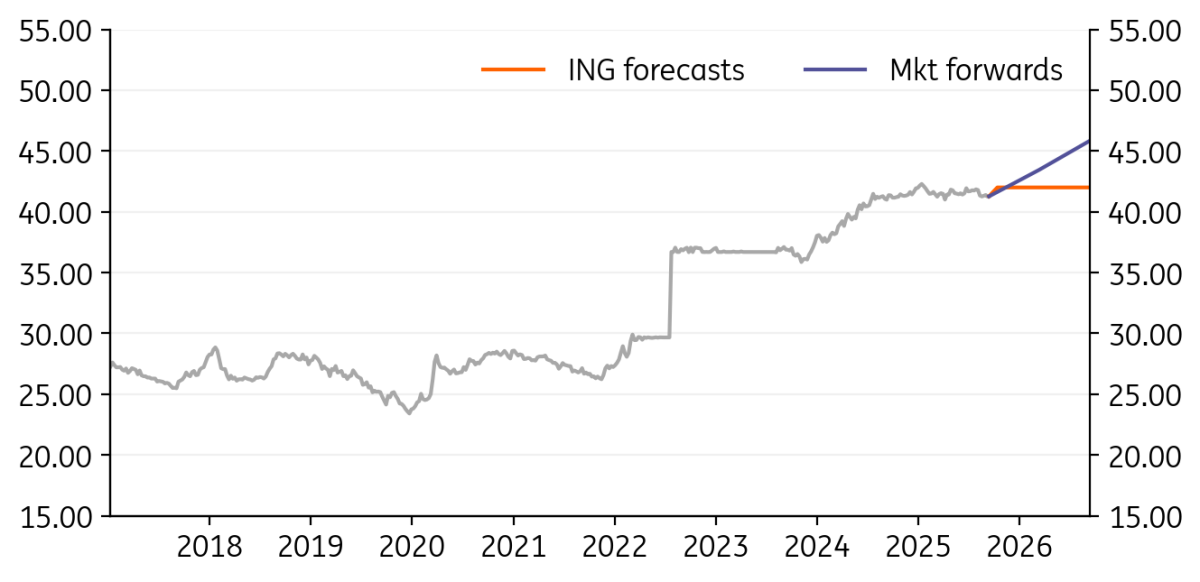

- The Central Bank of Turkey acknowledges that recent data supports continued easing given: a) a slowdown in the underlying inflation trend despite food and services price-related upward pressure, b) weak final domestic demand in 2Q, despite higher-than-expected GDP growth and c) demand conditions at disinflationary levels based on recent data.

- The Bank has signalled no changes to its macroprudential framework and continued rate cuts (the size of which will depend on the inflation outlook) and considerations regarding dollarisation and reserves, as we could potentially see more market volatility around court hearings in the coming period. Given this backdrop, the policy rate will be at 35.5% if the CBT maintains 250bp cuts, while a drop to 200bp cuts would pull it to 36.5% at year-end.

- The central bank also considers the real appreciation of the lira a natural outcome of its tight monetary stance, which increases demand for the currency. While we may not observe consistent appreciation in the short-term, i.e., on a month-to-month or quarterly basis, it is highly likely that the lira will experience cumulative real appreciation over a longer period, according to the CBT.

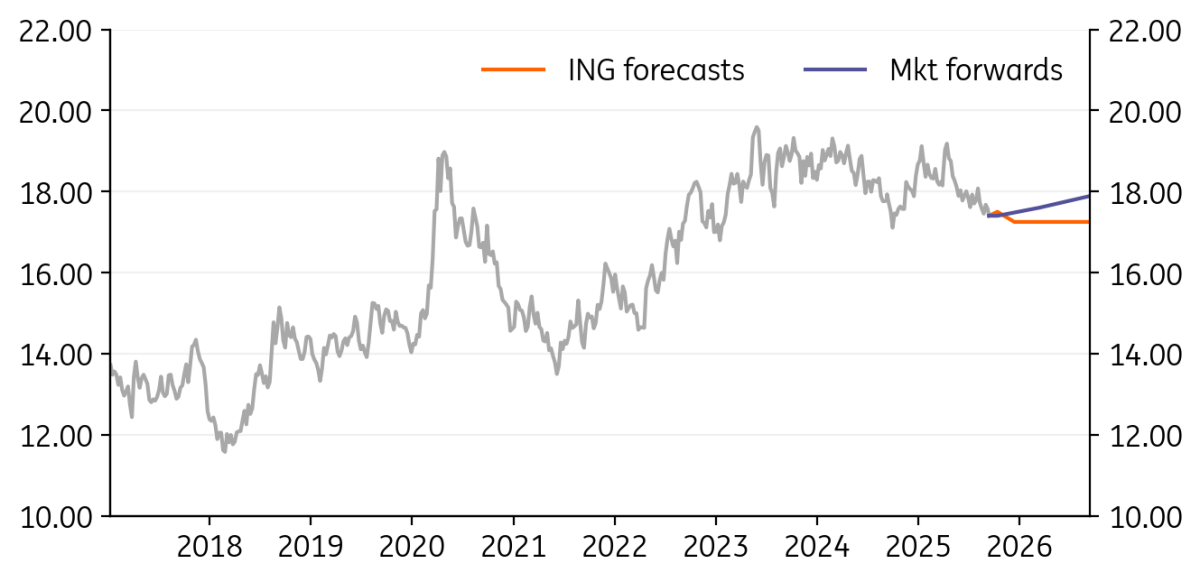

USD/ZAR: A healthy environment for the rand

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

17.40

|

Neutral | 17.50 | 17.25 | 17.25 | 17.25 |

- The rand continues to hold gains, and both the external and domestic environments look constructive. On the external side, lower US rates are good for global growth, and rising commodity prices are good for South Africa’s terms of trade. China also seems to be engineering a stronger renminbi, which is good for the rand too.

- Domestically, the government looks to be playing catch-up with the South African Reserve Bank’s shift to a 3% inflation target. Local government bonds are still in demand, where 10-year yields have dropped 150bp.

- 6%+ yields will help in the rand in a carry-friendly environment, and SA’s 0.5/0.7% of GDP current account deficit looks ok.

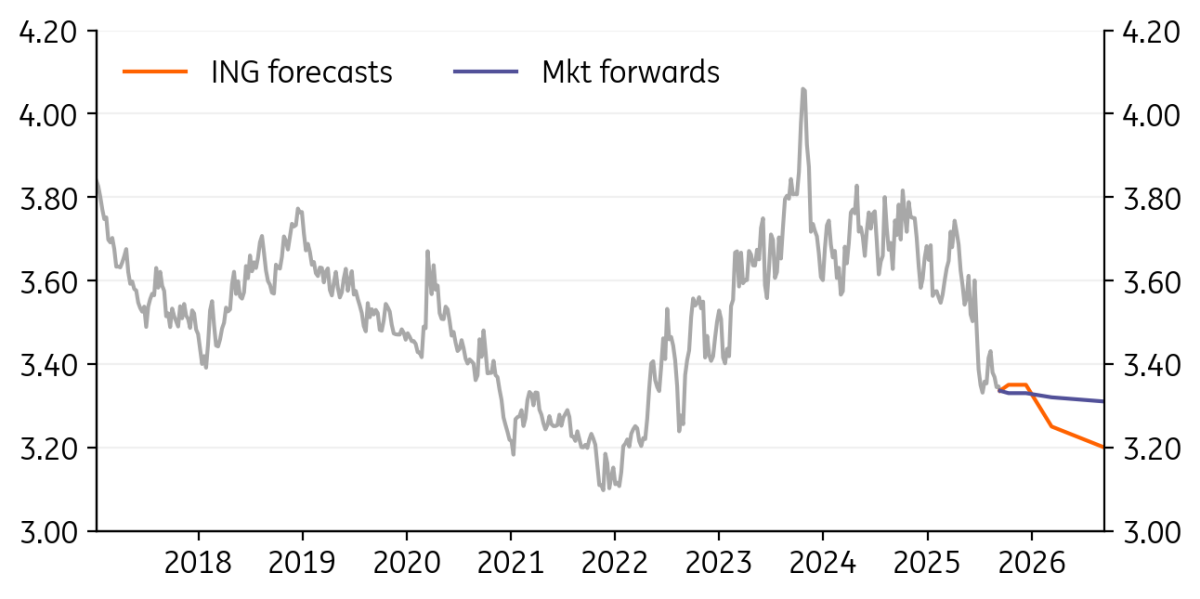

USD/ILS: Capital raising from tech companies helps ILS

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.34

|

Neutral | 3.35 | 3.35 | 3.25 | 3.20 |

- In spite of the current conflict and its threat of broadening in the region, the shekel remains relatively bid. Economic activity is expected to bounce back in the third quarter, where domestic demand trends look strong. Typically, Israel runs a large current account surplus on the back of its services industry. The balance of payments picture also looks to be helped by capital raising from Israeli tech companies. These were worth $5bn in 2Q and are expected to be at $3bn this quarter.

- With inflation a little above the top of the Bank of Israel’s 1-3% target range, the policy rate has been left on hold at 4.50%.

- The soft dollar environment favours USD/ILS to 3.10/20 next year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

FX Talking: Fed-powered rally has legs

- This bundle contains 6 Articles