EMEA FX Talking: Forint takes the spotlight into the election

- 10 February

- FX Talking

The Hungarian forint continues to perform very well as investors seemingly position for April's general election. We expect CEE currencies to largely hold gains, the Turkish lira to remain a popular carry trade target, and the South African rand to enjoy continued inflows into the commodities/China play

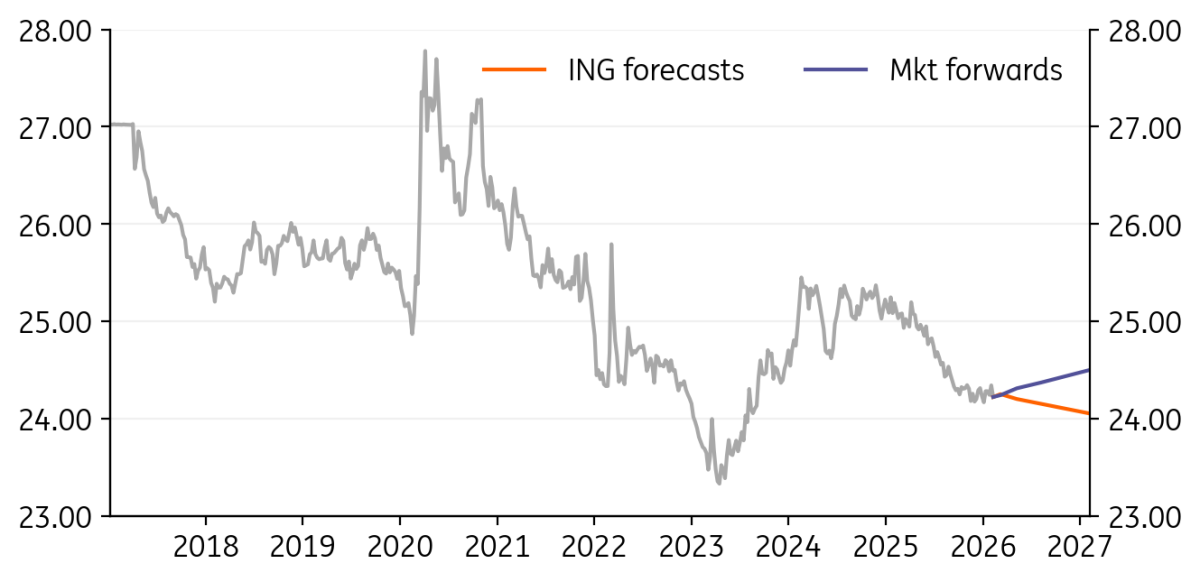

EUR/PLN: Further stabilisation of the zloty in early 2026

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.22

|

Neutral | 4.21 | 4.23 | 4.24 | 4.22 |

- The EUR/PLN exchange rate has hovered around 4.21 over the past couple of weeks. The zloty demonstrated resilience to both external factors (the sharp depreciation of the US dollar, historically positively correlated with CEE currencies) and domestic factors (expectations of a stronger disinflation trend in 2026).

- Nevertheless, the main driver behind zloty stabilisation is the strength of Polish economic activity. According to the latest GDP data for 2025, the economy is gaining momentum and outperforming the CEE region, with an even brighter outlook for this year.

- Current risks to the zloty remain linked to geopolitical factors (eg, military provocations in Europe), risk off in equity markets. In the medium term, the effectiveness of an ambitious local investment agenda and German stimulus is important for CEE currencies.

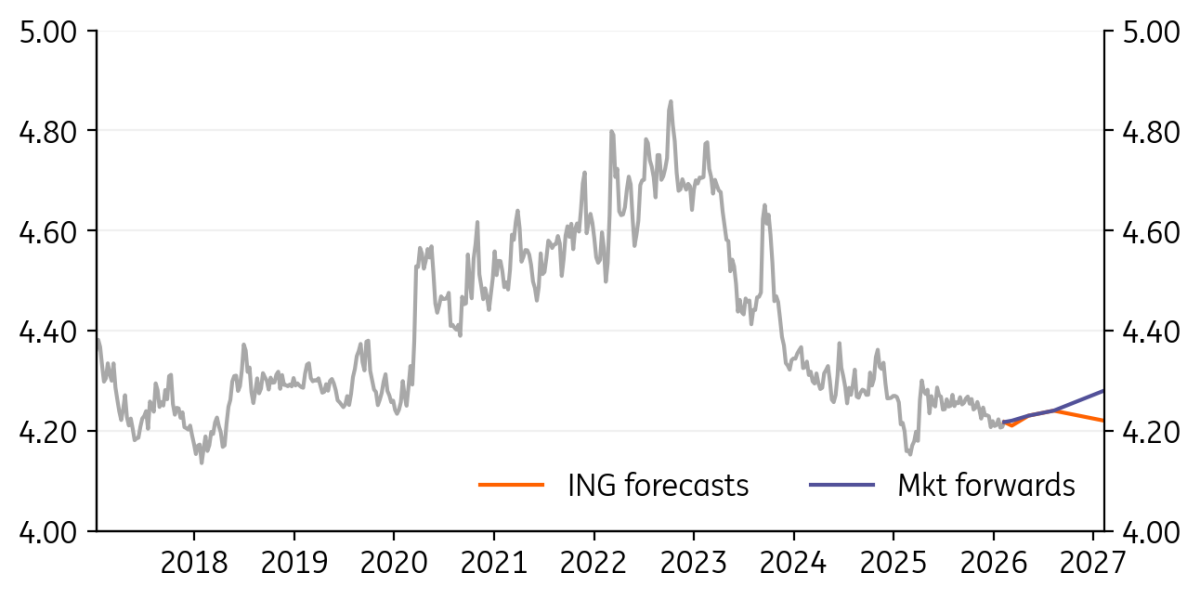

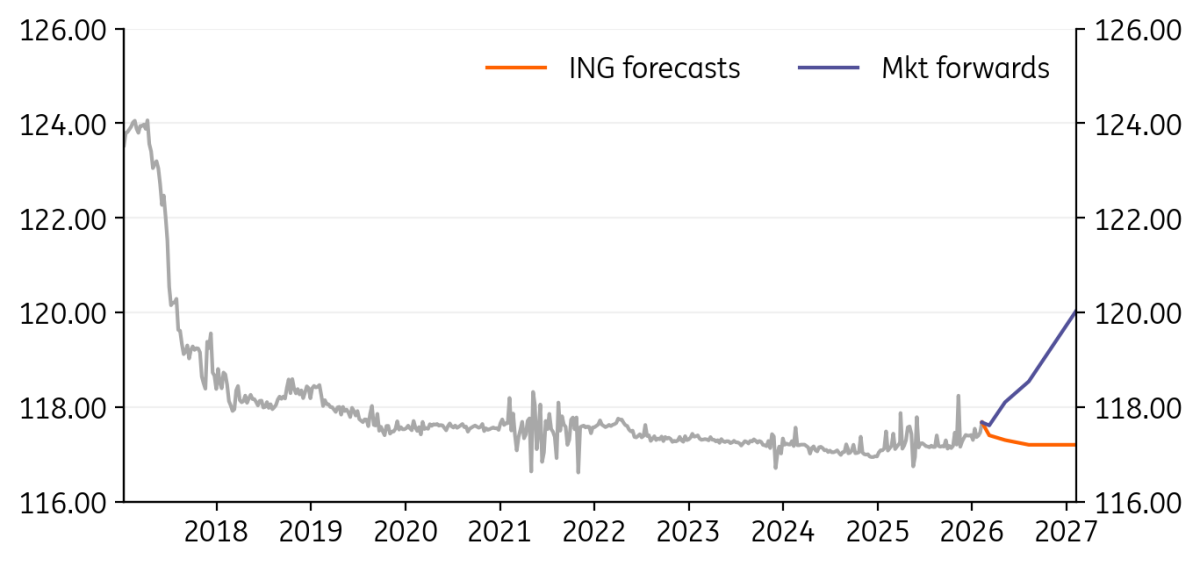

EUR/HUF: Range trading will continue amid rising volatility in HUF

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

378.00

|

Mildly Bullish | 380.00 | 385.00 | 383.00 | 380.00 |

- The dovish shift by the National Bank of Hungary resulted in the market pricing in a 100bp easing cycle in 2026. Following increased volatility, the EUR/HUF exchange rate returned to 380 – the level seen before the change in forward guidance.

- Though we wouldn't go so far as to label the forint as bulletproof, its resilience is clearly stronger than in previous years. The real test will be the upcoming general election and the related uncertainty, which is likely to prompt the EUR/HUF exchange rate to fluctuate based on headlines and investor sentiment.

- In general, many factors limit the upside and downside of the forint, ranging from monetary stance to fundamentals and positioning. Against this backdrop, we expect the forint to mostly remain within the 380–390 range over the coming quarters. We consider a peace deal between Russia and Ukraine to be the biggest event risk that could push the HUF out of this range.

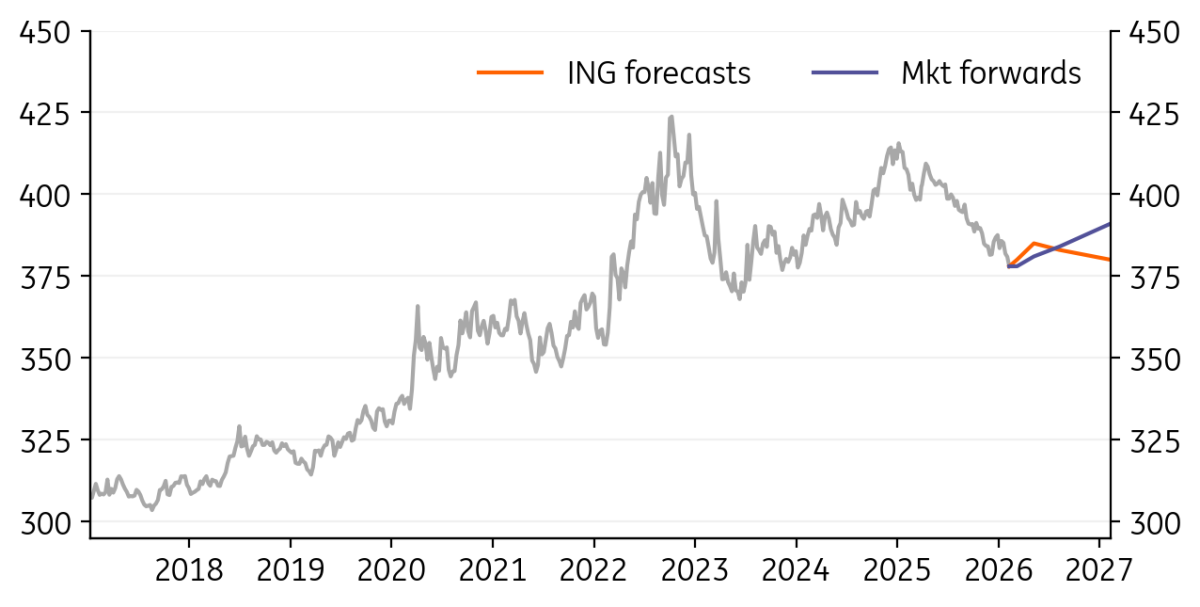

EUR/CZK: Solid expansion and hawkish CNB imply a strong koruna

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

24.25

|

Neutral | 24.25 | 24.20 | 24.15 | 24.05 |

- The Czech National Bank’s forecasts are likely to prop up economic expansion, real wage gains are set to remain upbeat, household budgets are growing more relaxed due to lower energy bills, and industry is coming out of the woods – all factors that could reduce the likelihood of monetary policy easing. Headline inflation is expected to hover below target over the year, but the fate of core inflation is shrouded in more uncertainty. It comes down to whether more discretionary spending raises the core rate or whether cheaper energy for both households and firms trickles down through the economy and weighs on other price segments with some lag. At this point, we are not sure which of the two counter-directional forces will ultimately dominate. However, with the output gap about to close, the temptation to not pass lower energy costs through to end-prices but to boost margins seems considerable.

- With such a setup, the Czech economy's growth advantage over the eurozone should prevail, as will the positive interest rate differential in both nominal and real terms vis-à-vis the euro. Should eurozone inflation drop further than expected below the ECB target, and the anticipated economic expansion of just above 1% prove to be wishful thinking, all the fundamentals behind the koruna's strong run could even grow more pronounced. In turn, we expect the koruna to continue in its gradual gains over this year.

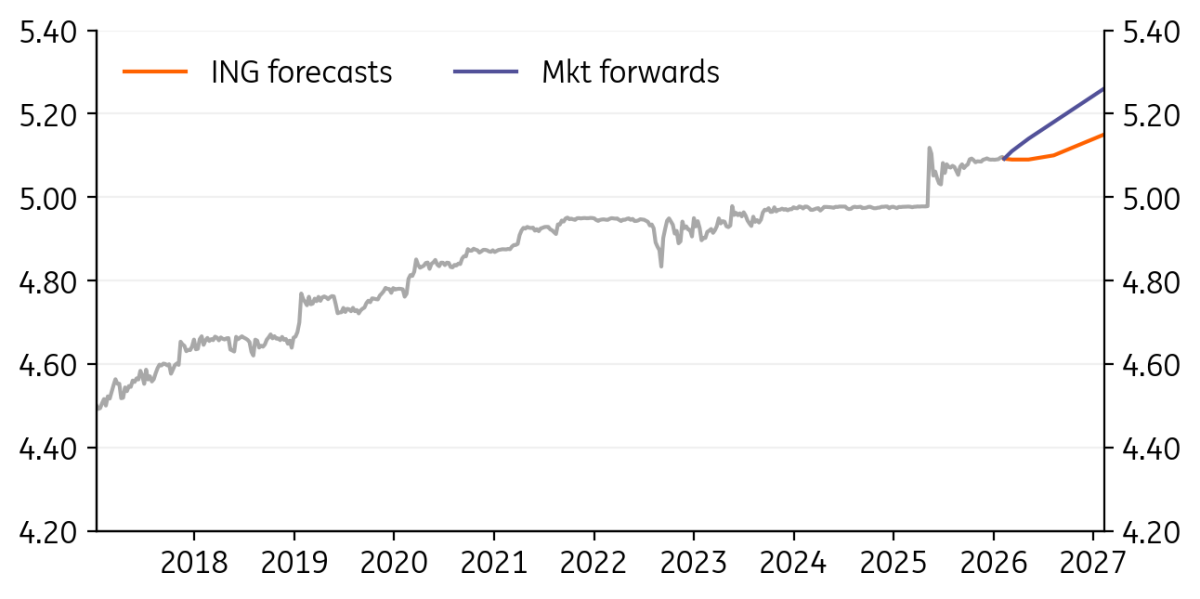

EUR/RON: No major changes expected in the coming months

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

5.09

|

Neutral | 5.09 | 5.09 | 5.10 | 5.15 |

- EUR/RON has been trading mostly sideways through the last month, with the pair continuing to remain in the 5.09-5.10 range. While some political noise and small upside inflationary risks remain in the picture, the outlook on the fiscal situation has improved visibly.

- The budget deficit stood at 7.7% at end-2025, well below the formerly agreed 8.4% target. The budget for 2026 is set to be adopted in the second half of February, while some targeted economic stimulus measures are in the making. The liquidity surplus in the interbank market rose sharply in January to RON41.9bn (Dec: RON29.5bn), likely linked to increased government spending and in line with the decline in money market rates.

- While we expect these ample liquidity conditions to persist due to large EU funds inflows, we also think that the National Bank of Romania would welcome some FX pressures that allow it to sell foreign currency and retain a degree of control on liquidity. We expect the pair to remain within its current range and close the year near 5.15.

EUR/RSD: RSD likely to continue sideways on a firm NBS grip

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.38

|

Neutral | 117.40 | 117.30 | 117.20 | 117.20 |

- EUR/RSD moves remained contained despite consequential events throughout the month. The pair sat mostly within the 117.30-117.60 range. The sale of the NIS refinery to MOL Group is now in advanced stages, with parties aiming to close the deal by end-March.

- In the background, the positive fundamentals backed by strong investments are still in the picture. A better-than-expected 2.6% of GDP result was recorded for the budget deficit (estimated: 3.0%), showing renewed signs of fiscal prudence. In late January, Fitch also kept Serbia’s rating at BB- with a positive outlook.

- At its January meeting, the National Bank of Serbia kept the key rate in place at 5.75%; despite a more certain inflation outlook, global uncertainties continued to rank high on policymakers’ radars. We continue to believe that FX stability should remain a key focus ahead – in 2025, the Bank sold €588m to keep the pair stable

USD/UAH: UAH under selling pressure

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

42.90

|

Mildly Bullish | 43.60 | 43.80 | 43.80 | 43.80 |

- The USD/UAH exchange rate broke above 43.0 – the highest level on record. Ukraine’s currency continues to face pressure due to ongoing war-related disruptions (prolonged power outages, destruction of production), as well as the National Bank of Ukraine’s decision to cut interest rates in January (for the first time since mid-2024).

- Taking into account the steady decline in inflationary pressures and lower risks related to external financing, the NBU decided to initiate an interest rate cutting cycle. At the end of last month, the key policy rate was reduced by 50bp to 15.0%.

- Factors supporting the hryvnia include international financial aid and ongoing trilateral peace negotiations. In 3Q25, the level of international reserves increased rapidly, reaching the highest level since the country’s independence.

USD/KZT: Strong start of the year

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

495.00

|

Mildly Bullish | 500.00 | 515.00 | 525.00 | 535.00 |

- The tenge opened the year strong, rising 0.7% vs the USD in January and pushing to 1.5-2.0% in early February, breaking below 500 per USD on the back of firm commodity prices and stronger currencies of the key trade partners (CNY and RUB).

- The earlier 8% KZT rally in 4Q25 was driven by accelerating private capital inflows, which, combined with portfolio inflows into the state bond market, offset the continued decline in the trade balance, according to preliminary 4Q25 balance of payments data.

- January CPI unexpectedly slowed by 0.1ppt to 12.2% YoY despite a 4ppt VAT hike, reducing the likelihood of further rate increases from the current 18.00%. We remain constructive on the KZT in the near term on portfolio flow prospects, while remaining cautious later in the year given structural headwinds.

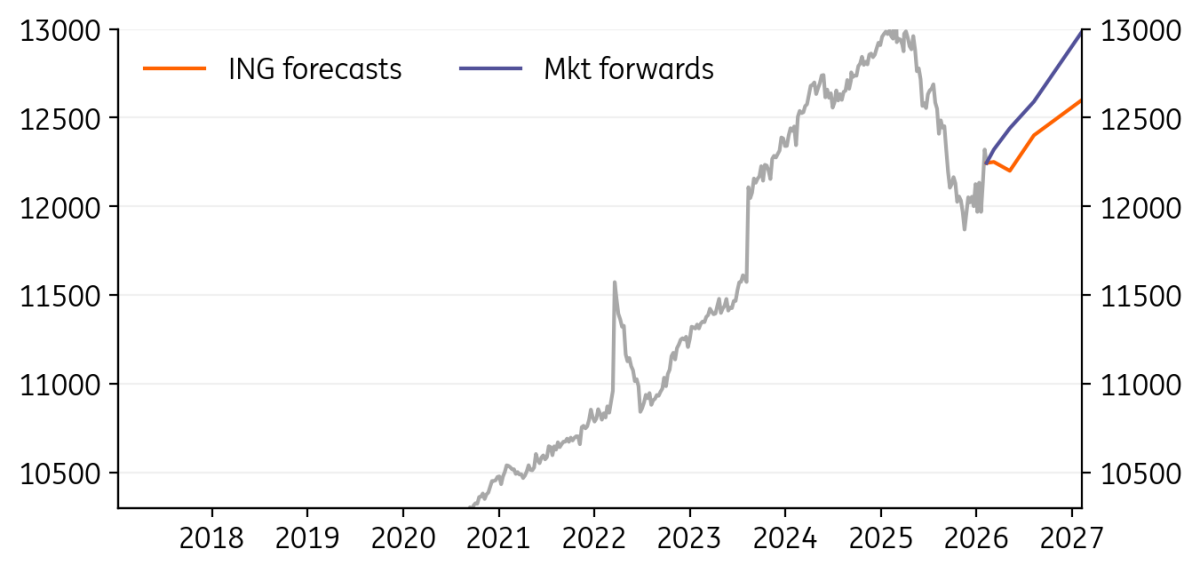

USD/UZS: Tactical retreat after a strong gold-related rally

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

12303.00

|

Mildly Bearish | 12250.00 | 12200.00 | 12400.00 | 12600.00 |

- After an exceptionally strong 7% appreciation vs USD in 2025, the Uzbekistani soum has corrected by over 2% to 12,300/USD since the start of the year. The move began even before the late‑January decline in the gold price.

- Uzbekistan’s gold exports paused in 4Q25 after shipping 85mt in 9M25, consistent with the government’s usual approach of spreading sales over time. Combined with fast import growth, this contributed to a US$2.5bn YoY widening of the trade deficit to US$18bn in 2025, pressuring the soum.

- Given Uzbekistan’s annual capacity to export roughly 100mt of gold – generating around US$4bn in export proceeds for each US$1,000/oz in the gold price – we remain constructive on near‑term UZS prospects. However, a lasting improvement in the country’s twin deficit (external and fiscal) and CPI dynamics is needed to avoid a return to the longer‑term depreciation trend seen in previous years.

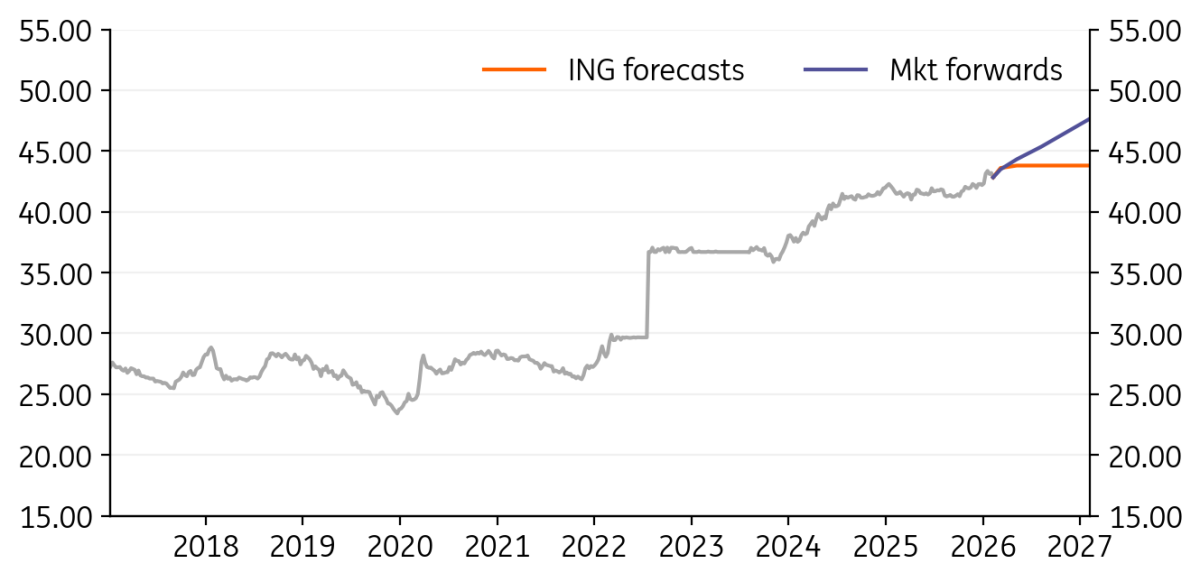

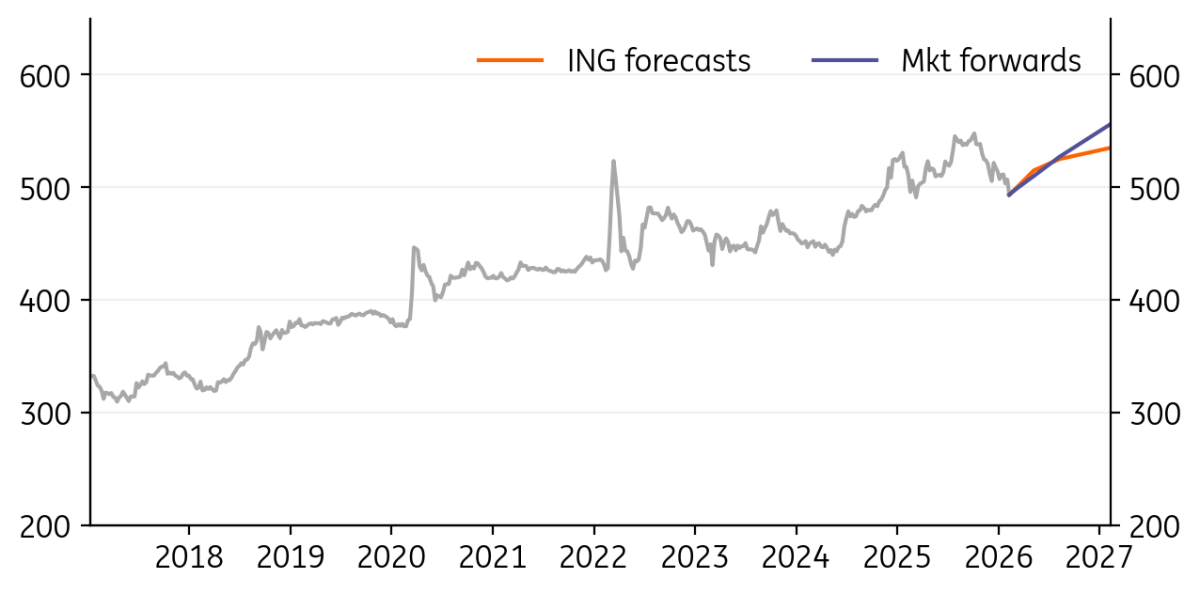

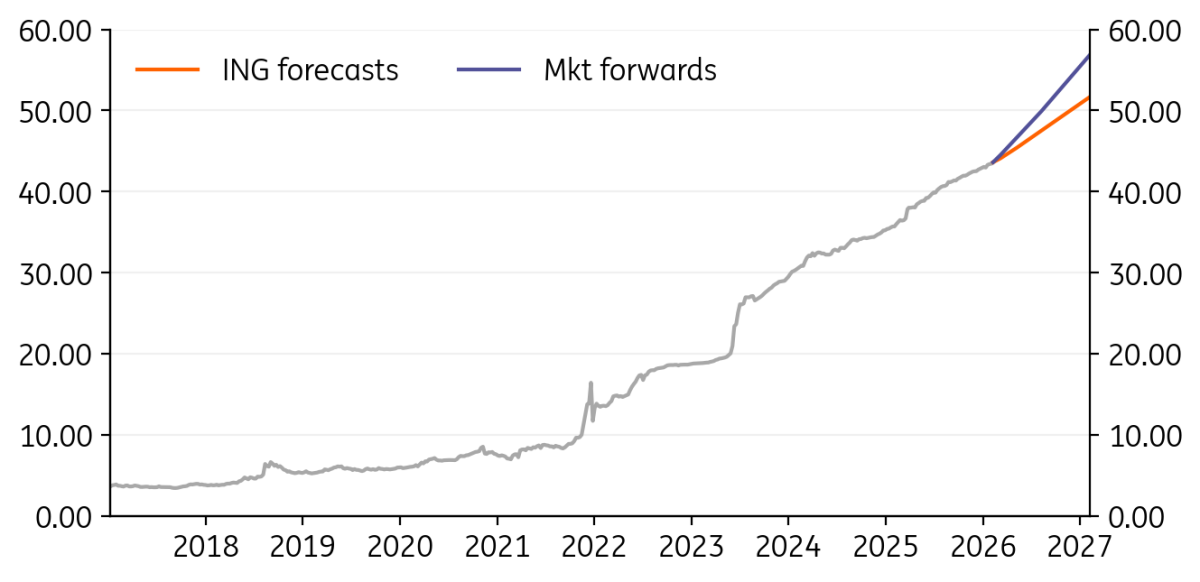

USD/TRY: CBT likely to remain cautious with inflation risk

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

43.60

|

Mildly Bullish | 44.10 | 45.40 | 47.50 | 51.70 |

- At 4.84% MoM, January inflation came in above consensus, while annual inflation has maintained its downtrend with a further decline from 30.9% to 30.7%, thanks to a supportive base. We’ve revised our end-year inflation from 22% to 23%, above the Central Bank of Turkey’s forecast range of 19% in the November report.

- Pricing pressures and the recovery in demand conditions have prompted the CBT to act more cautiously, slowing the pace of its rate cuts in the January MPC and implementing coordinated macroprudential measures with the BRSA. It will continue to closely monitor inflation, demand conditions, international reserves and depositor behaviour to determine the pace of cuts.

- Given upside risks to inflation with uncertainty surrounding heavy-weight food and energy prices, the CBT will maintain its cautious stance in its current rate-cutting cycle. We expect the bank to bring the policy rate to 28% by end-2026, with risks on the upside.

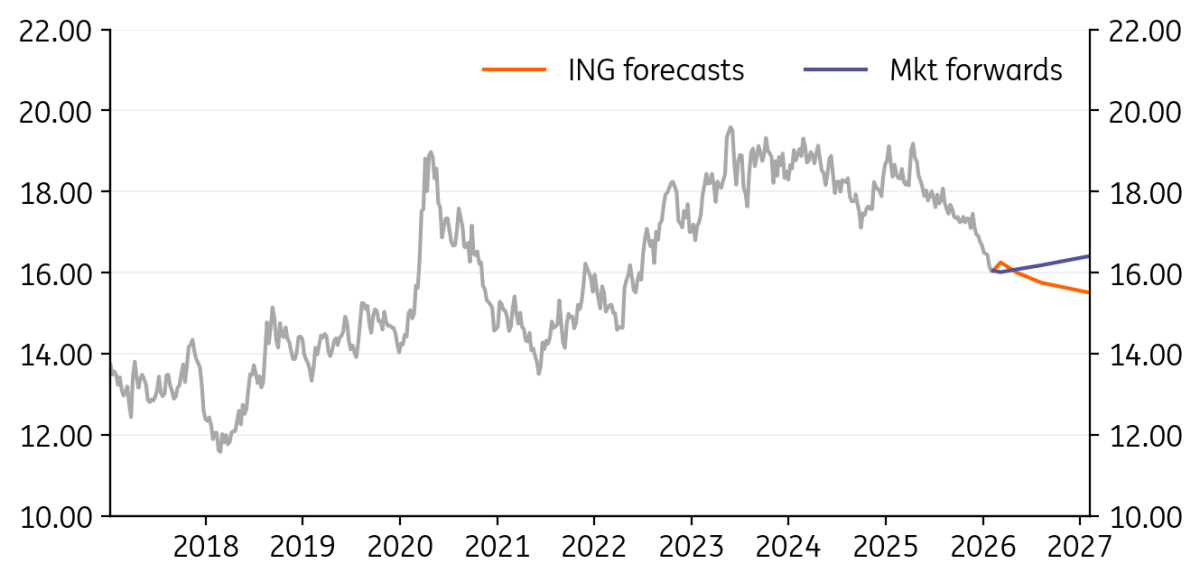

USD/ZAR: Supportive rand environment continues

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

16.04

|

Mildly Bullish | 16.25 | 16.00 | 15.75 | 15.50 |

- The rand remains one of the most popular emerging market trades in the world today. Its 6.5% implied yields are not especially spectacular, but the rand is backed by South Africa’s precious metal exports, including gold. Gold has proved central to the dollar debasement thesis. The terms of the trade story will remain a major support to the rand this year.

- Domestically, South Africa’s growth picture is turning more sustainably supportive. Inflation is contained, consumption is picking up, and the South African Reserve Bank could cut another 50bp to 6.25% if conditions remain benign.

- A narrower current account deficit suggests ZAR is not overvalued.

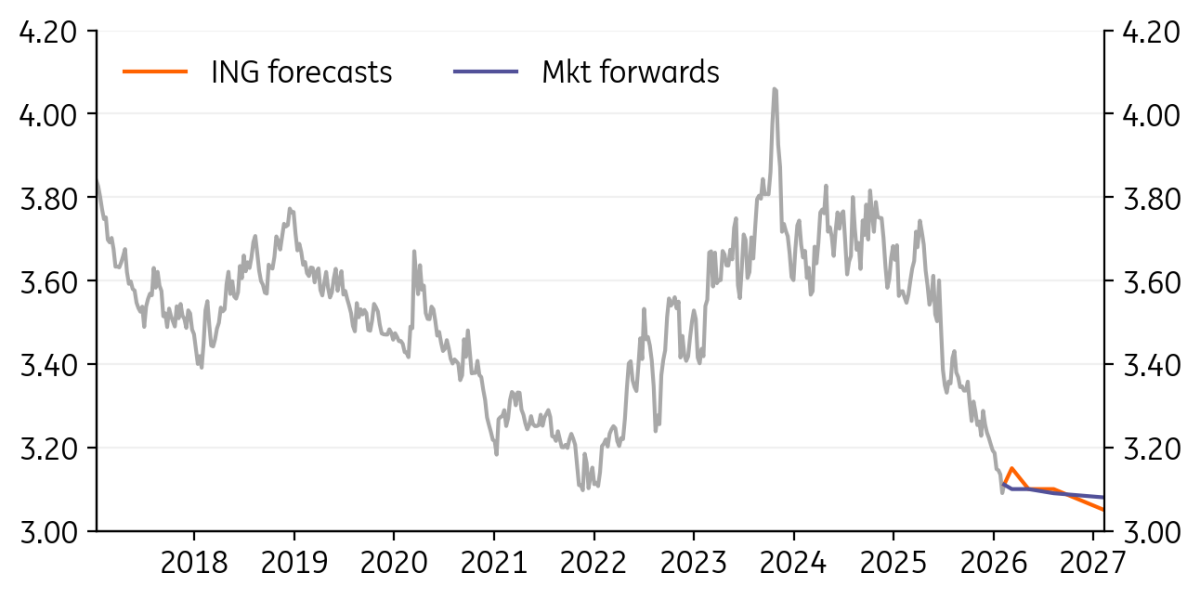

USD/ILS: BoI rate cuts will have to replace intervention

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.12

|

Neutral | 3.15 | 3.10 | 3.10 | 3.05 |

- January’s broad sell-off in the dollar has carried USD/ILS close to the 2021 low at 3.04. Typically, the Bank of Israel has been a very FX interventionist central bank and would have been buying a lot of FX by now. But heavy scrutiny from the US Treasury on trading partners preventing their currencies from appreciating may now be tying the hands of the BoI.

- If it cannot intervene, monetary policy will have to take the strain. That is why the BoI is priced to cut the 4.00% policy rate by a further 125bp this year.

- US tech shocks are normally ILS negative – hitting potential tech FDI into Israel – another reason why USD/ILS may not trade sub-3.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

10 February

FX Talking: Dollar appetite erodes

- This bundle contains 6 Articles