EMEA FX Talking: CE4 easing cycles moving nearer

- 12 June 2023

- FX Talking

More evidence of disinflation across the CEE region is raising expectations that these will be some of the first central banks to cut rates. We do not think this will be enough to damage the high-yield appeal of CE4 currencies - even though long positioning is quite heavy. The rand will remain fragile on geopolitics and large rate hikes could slow TRY losses

Source: Shutterstock

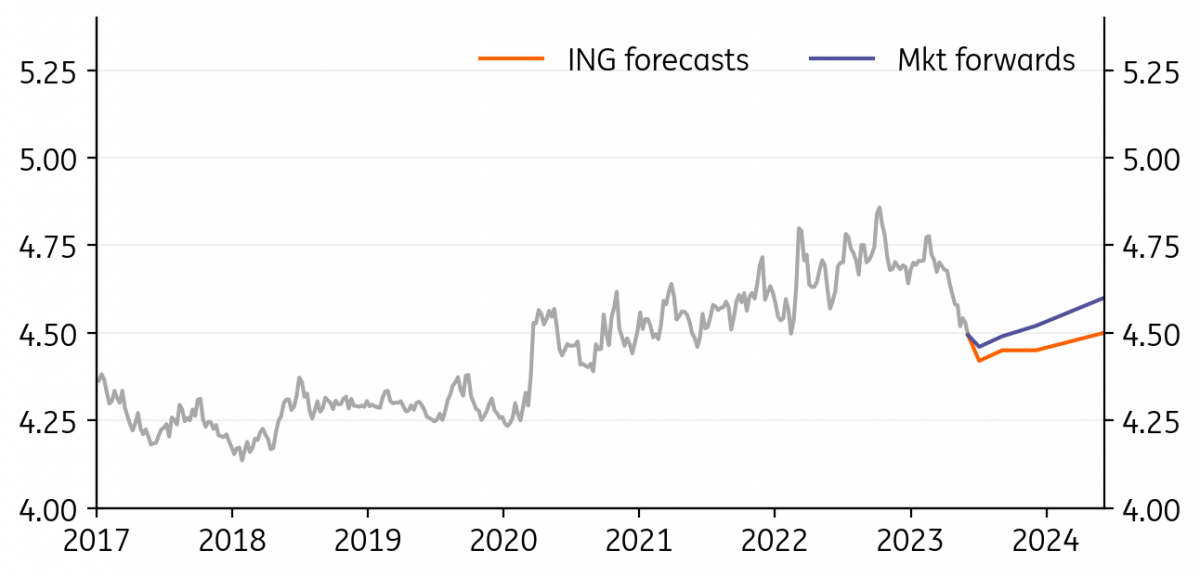

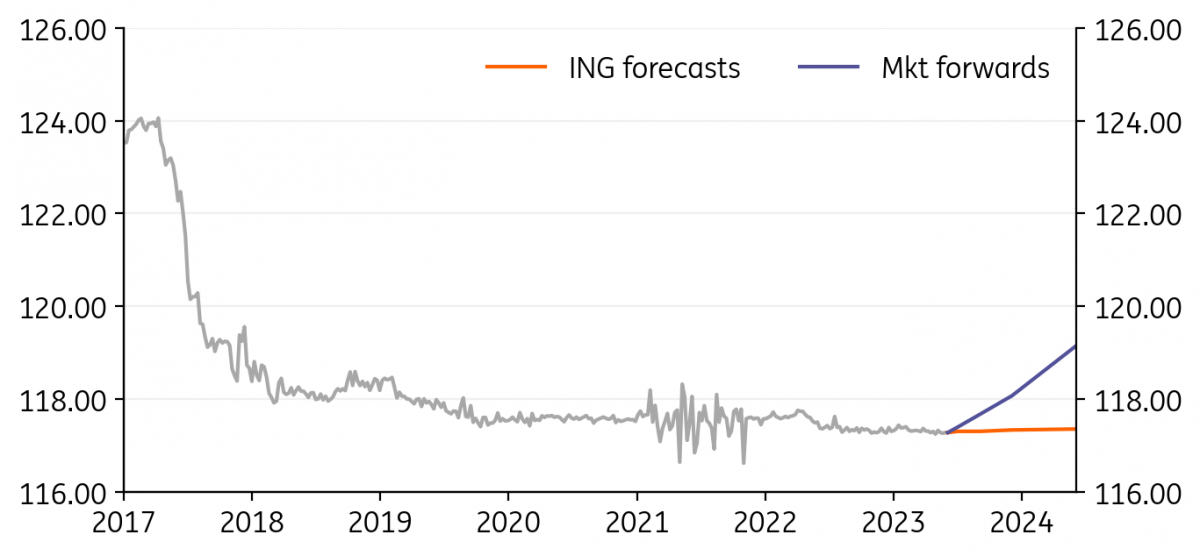

EUR/PLN: Improving fundamentals and market perception

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.4452

|

Mildly Bearish | 4.42 | 4.45 | 4.45 | 4.50 |

- The zloty significantly recovered in 2Q23 owing to a significant current account surplus and, perhaps, bets on a more market-friendly government after the general election. These factors are likely to persist over the remainder of the year.

- However, based on our estimates, the zloty is no longer undervalued against the euro. The National Bank of Poland has already effectively ended its tightening cycle and some MPC members are signalling prompt rate cuts. Simultaneously, markets are repricing the Fed and ECB rate paths. In tandem with elevated inflation in recent years, this has undermined to some extent the competitiveness of local companies and should limit the scope for EUR/PLN to drop to around 4.40.

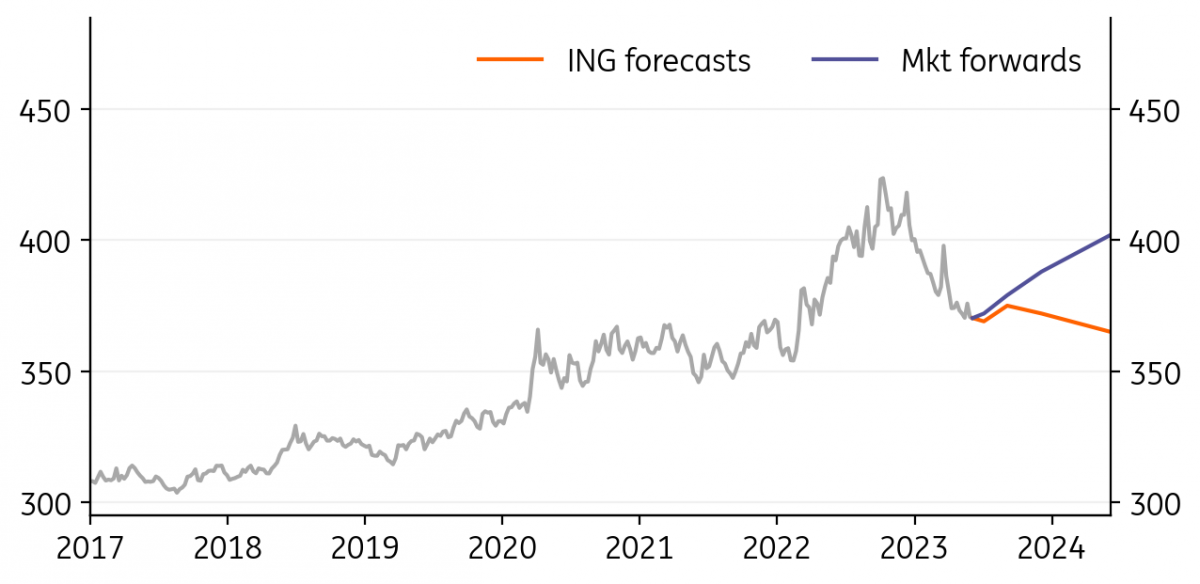

EUR/HUF: Forint to hover within a tight range in the summer

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

368.91

|

Neutral | 369.00 | 375.00 | 372.00 | 365.00 |

- Until the EU fund risk has been cleared, we see periods of weakness for the forint due to a lack of news on the progress of an EU deal and on seasonality in the summer. However, given the rather pessimistic market expectations already, we continue to see a working framework for the coming weeks in the 368-378 EUR/HUF range.

- We believe that the market will use weaker levels as a new entry point to build positions in the forint to benefit from a still very attractive carry. On the other hand, at the lower end of the range, bets will rise on more easing, limiting HUF upside.

- All of this should keep EUR/HUF in a rather tight range. We see potential for a positive breakout on an EU deal later this year.

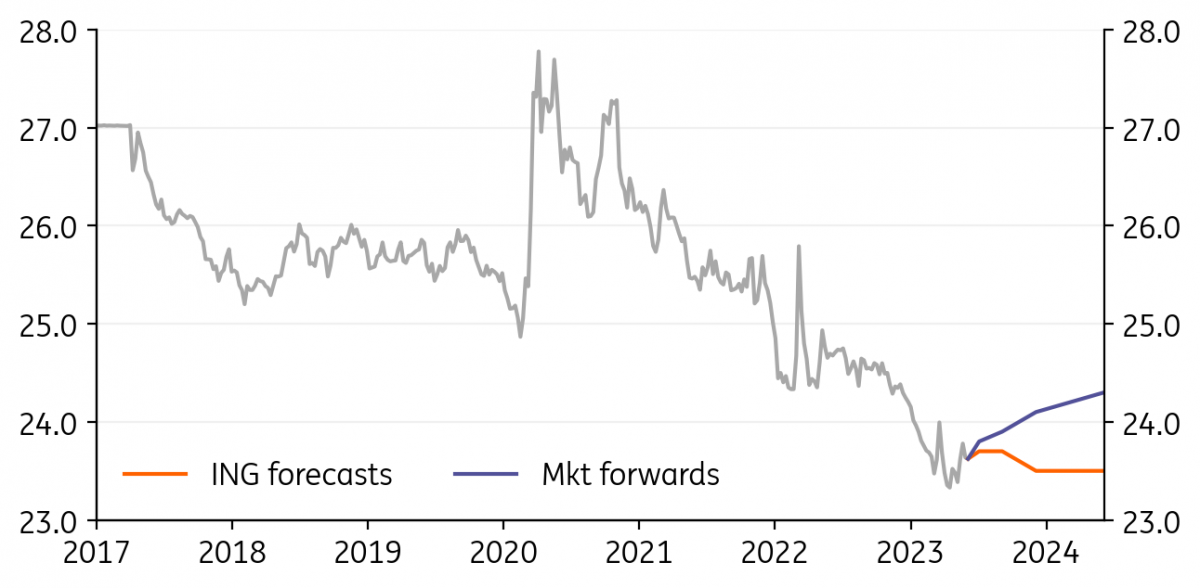

EUR/CZK: Waiting for rebound in EUR/USD

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

23.71

|

Neutral | 23.70 | 23.70 | 23.50 | 23.50 |

- The Czech koruna has lost market interest in recent weeks and attention has shifted within the region to the Polish zloty, which has more potential for a rally based on the local story.

- However, the CZK shows by far the highest beta against the US dollar within the region, still offers a solid carry and the central bank is ready to defend the koruna against depreciation in case of problems. Moreover, market positioning is not as heavily long as in the case of PLN and HUF.

- Thus, we believe the CZK is a good proxy view for the global story within the region. Thus, the koruna should benefit the most from an EUR/USD rebound to the upside.

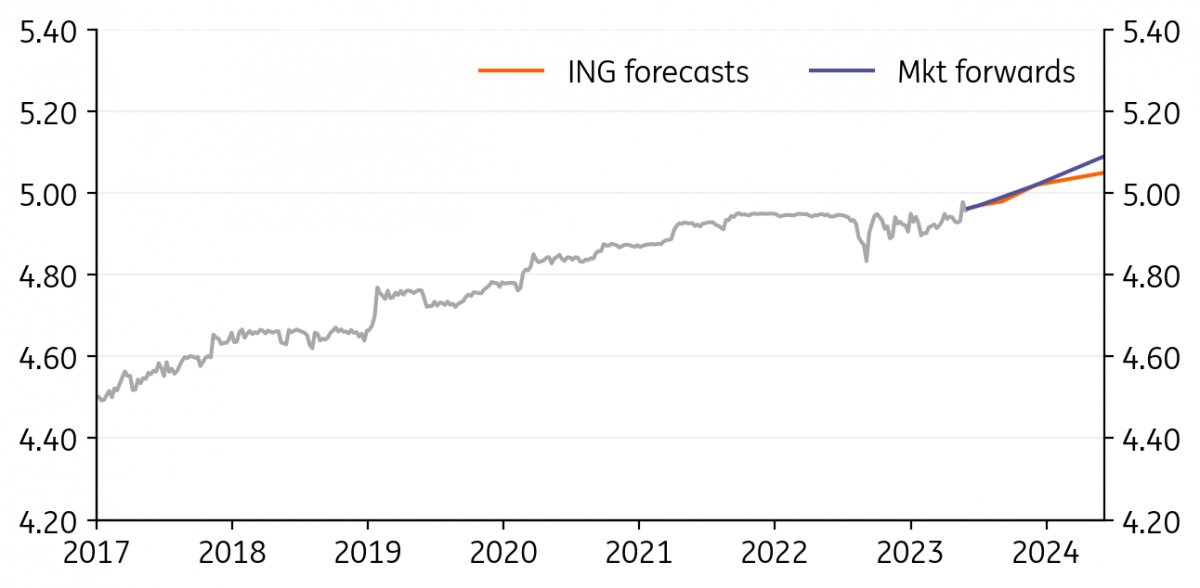

EUR/RON: A first upside move, but likely not the last this year

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

4.9549

|

Mildly Bullish | 4.97 | 4.98 | 5.02 | 5.05 |

- EUR/RON touched 4.98 in May, which seems like a new line in the sand for now. Considering the record level of excess liquidity in the market, we think this situation cannot suit the central bank.

- Seen from this angle, allowing the EUR/RON to go higher might be an attempt to increase upside market pressure and get some of the excess liquidity out of the system.

- The new temporary range is likely to be 4.94-4.98, with no expectation of moves to the lower levels we saw in the first quarter of this year, supported by massive demand for ROMGBs. We can expect at least one more upward shift this year and we maintain our 5.02 estimate for year-end.

EUR/RSD: No deviation from the tightly managed floating policy

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.25

|

Neutral | 117.30 | 117.30 | 117.33 | 117.35 |

- After raising the policy rate by 500bp to 6.00% in just over a year, the National Bank of Serbia seems to be taking its time now and contemplating the effects of past monetary tightening.

- We believe that the next policy decision will be a rate cut in 1Q24 when we will finally have positive real rates. We do not envisage headline inflation back within the NBS’s 1.5%-4.5% target range over the next two years.

- We maintain our expectations for an essentially flat EUR/RSD profile for the rest of 2023 and even through 2024, with FX intervention likely to occur in a rather narrow range around the 117.30 level.

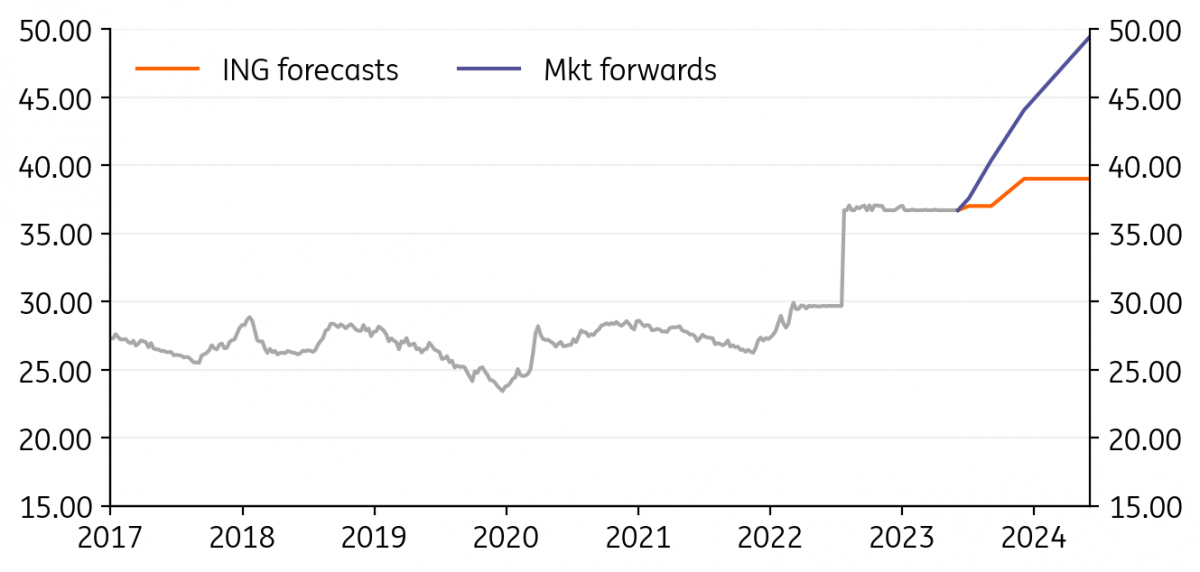

USD/UAH: Rising FX reserves provide stability

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

36.931

|

Mildly Bullish | 37.00 | 37.00 | 39.00 | 39.00 |

- Ukraine’s international reserves exceeded US$36bn in May for the first time since 2011. This reflected continued foreign aid and the lower monthly cost of FX intervention (around US$2bn in May, down from the monthly peak of US$4bn in June 2022). This significantly deceases the near-term odds of another devaluation, as the central bank may prefer a stable currency to combat inflation.

- The fundamental factors behind the hryvnia remain unsupportive though. Ukraine is running a significant trade deficit, as exports collapsed in 2022, while imports remained quite stable. With the central bank aiming to re-liberalise the FX market at some point this signals the risk of further devaluation in the future.

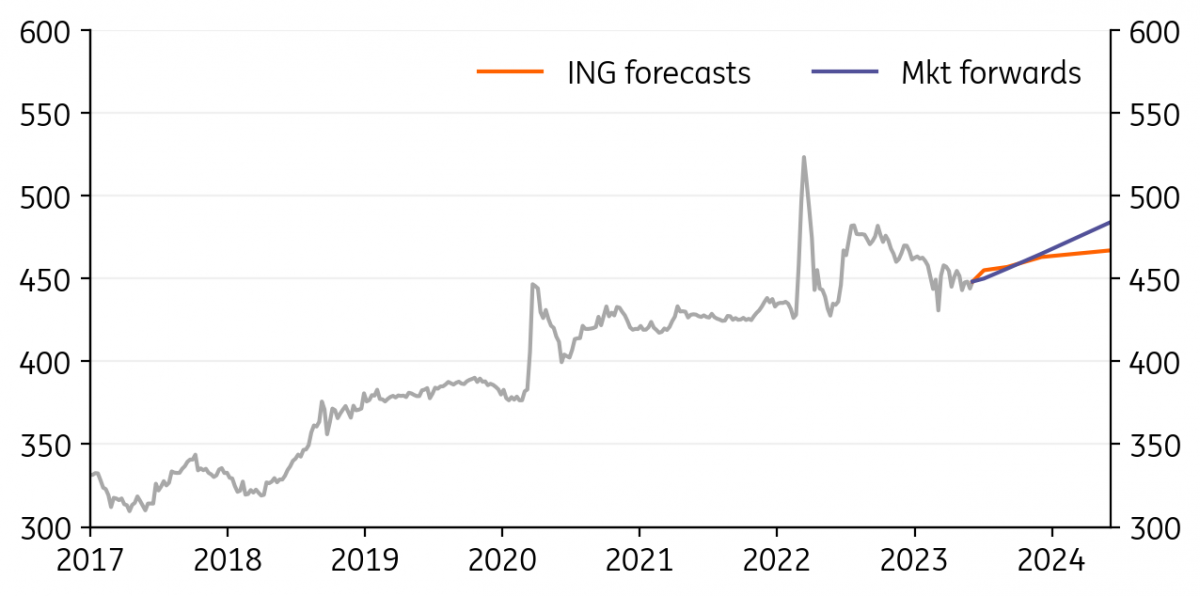

USD/KZT: Further appreciation is facing obstacles for now

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

446.05

|

Bearish | 455.00 | 457.00 | 463.00 | 467.00 |

- USD/KZT ended May very close to our 450 target, showing mild appreciation during the month amid range-bound oil prices and despite the stronger dollar environment. The recent OPEC+ extension should be supportive of oil, but the longevity is questionable.

- Kazakhstan’s current account returned to a $1.5bn deficit in 1Q23 after a $8.5bn surplus in 2022 and is likely to remain negative. KZT appreciation since 3Q22 was based on the atypical net private capital inflow of c. $3bn per quarter, which can prove volatile.

- The new fiscal rule assumes lower state sales of FX out of NFRK, the sovereign fund, suggesting the prospects for the tenge will be further tied to its dependence on volatile oil prices and capital flows.

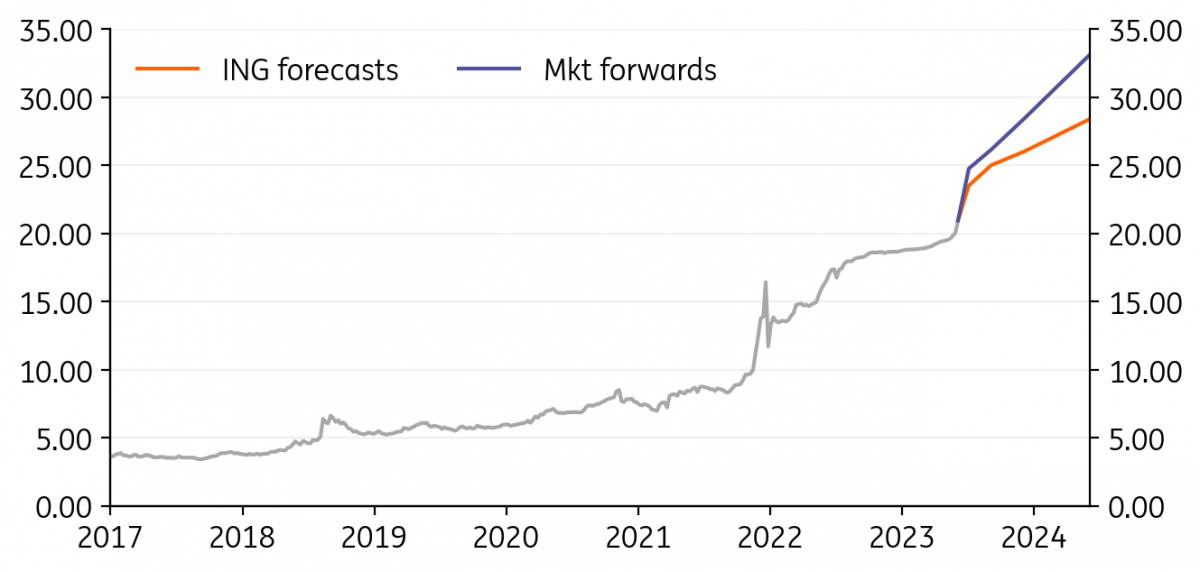

USD/TRY: Higher pace of TRY depreciation

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

23.649

|

Neutral | 23.50 | 25.00 | 26.00 | 28.40 |

- Under the existing Central Bank of Turkey policy, gross FX reserves have been under pressure since the beginning of this year. Gold reserves are also on the decline, as the CBT directly matches gold demand. Accordingly, total reserves fell below the US$100bn threshold. However, excluding swaps with banks and other central banks, the CBT’s net reserve position is at US$-60.5bn, an all-time low.

- Since the run-off elections, which reduced the extent of indirect intervention, the CBT has allowed an increase in the pace of the lira’s depreciation.

- Given new names in the economy management team after the elections, any CBT signal on a policy shift will be closely watched by the market.

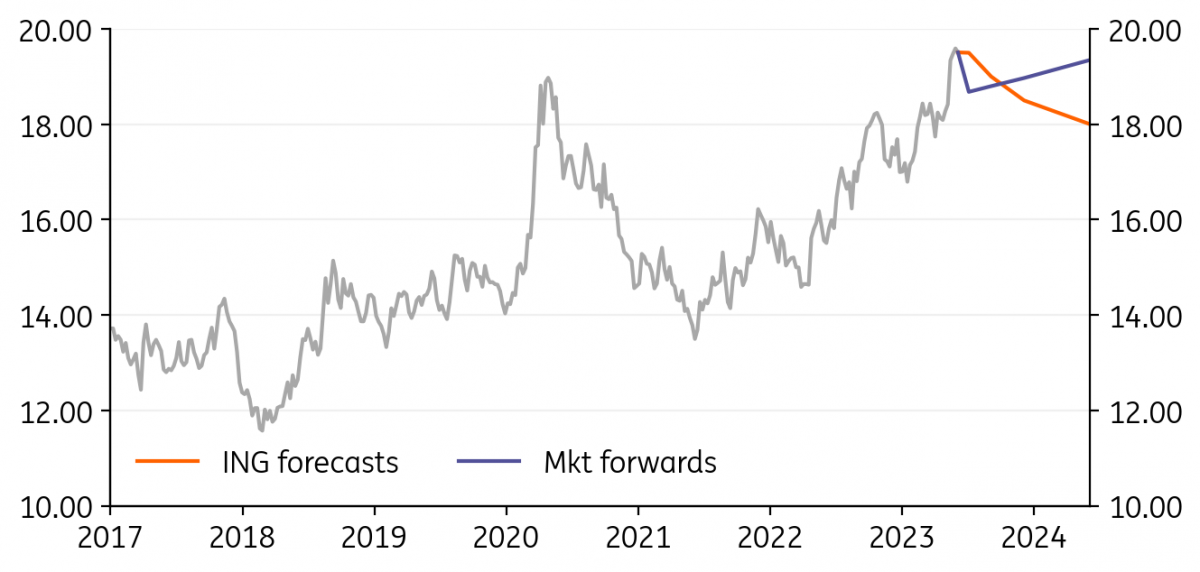

USD/ZAR: Geopolitics recommends caution on the rand

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

18.627

|

Bullish | 19.50 | 19.00 | 18.50 | 18.00 |

- The rand has recovered well after USD/ZAR nearly hit 20.00 in early June. Positive real rates are back in fashion in emerging markets, where the rand offers something like 3% (policy rate 8.25%, core inflation 5.3%). However, the benign international environment has certainly helped i.e. low volatility conditions.

- Geopolitics may discourage investors chasing rand gains. In August, South Africa hosts a summit of BRICS leaders. Expect to hear more on the story of possible South African arms sales to Russia – and US Congress questioning trade ties.

- Weak growth (0.5-1.0% over coming years) and a current account deficit in the 2-3% of GDP area will hold ZAR back.

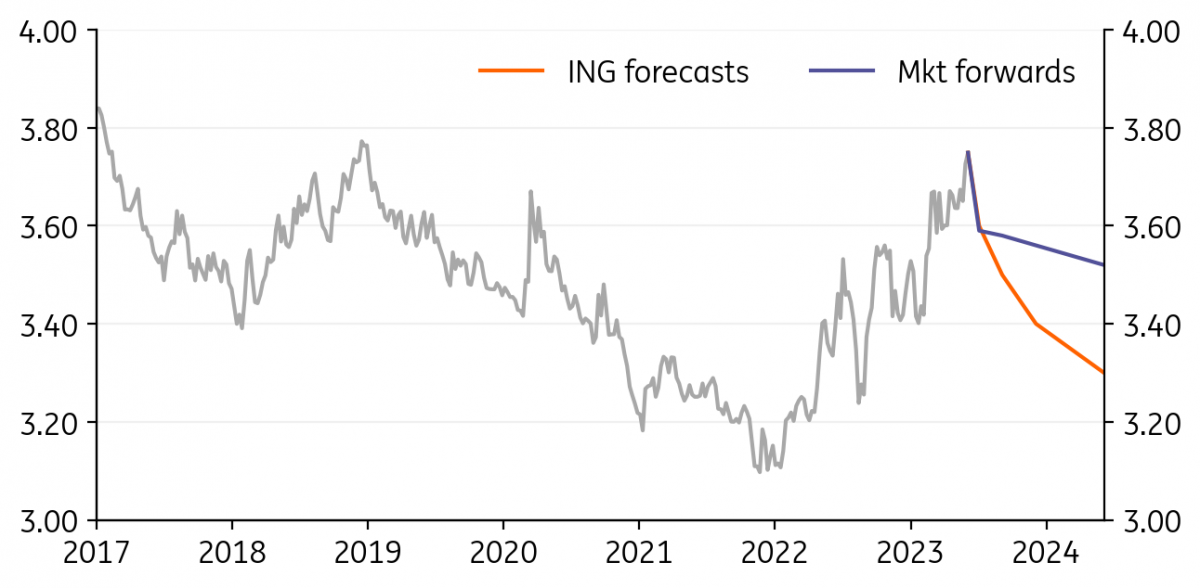

USD/ILS: ILS losses reverse. Politics and central bank help

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.5891

|

Neutral | 3.60 | 3.50 | 3.40 | 3.30 |

- Three factors have probably helped USD/ILS reverse sharply from the 3.75 area: 1) The central bank saying in late May it would have to hike more if the shekel weakened any further. 2) An interim agreement in parliament to try and diffuse controversial judicial reforms and 3) the more benign global environment.

- It will be interesting to see whether the sharp drop from 3.75 to 3.60 has been assisted by FX intervention. We will learn more in early July. The better news on politics could easily reverse as well – warning against chasing shekel strength too soon.

- If we’re right with our bearish dollar call and the furore over judicial reforms can settle – USD/ILS can trade 3.40/50 later in 2023.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more