EMEA FX Talking: Splits start to emerge in monetary cycles

- 8 August 2025

- FX Talking

Across the CEE, splits are starting to emerge in monetary cycles. The Czech National Bank has likely ended its easing cycle and looks ready to discuss tighter policy. Yet Poland and Hungary are still easing. Expect the Czech koruna to continue its outperformance, while we doubt the forint's rally has legs. Elsewhere, the lira and the rand can hold gains

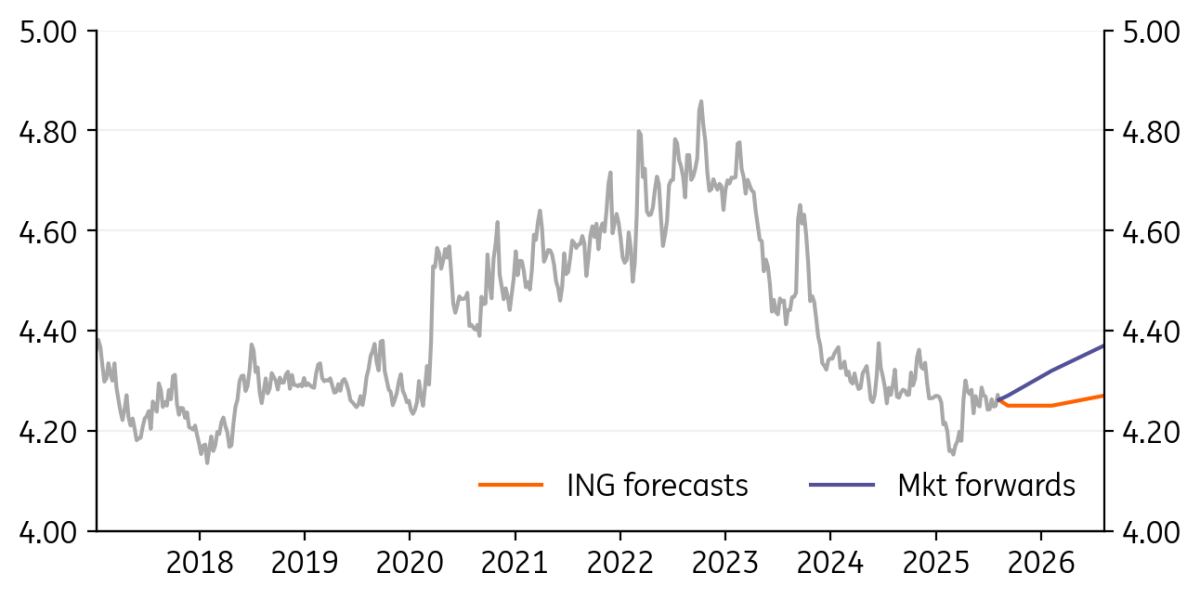

EUR/PLN: Zloty at risk from MPC stance after the summer

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.2615

|

Mildly Bearish | 4.25 | 4.25 | 4.25 | 4.27 |

- Despite volatility in the global FX markets due to the trade war saga, and with mounting pressure on the Fed to cut rates, the Polish zloty has remained relatively unchanged. Even the unexpected Monetary Policy Council decision to cut rates in July did not trigger a sell-off in the zloty. The EUR/PLN exchange rate is still around the 4.27 level in range-bound trading (4.23–4.30).

- The positive carry trade is the main argument responsible for PLN strength. However, as inflation drops close to the central bank’s target, we expect the MPC will continue to cut interest rates, making the zloty less attractive. The fundamentals of the economy remain solid, and the GDP dynamics should outperform the CEE region - but the high deficit and political spending race undermine the bid for Polish government bonds.

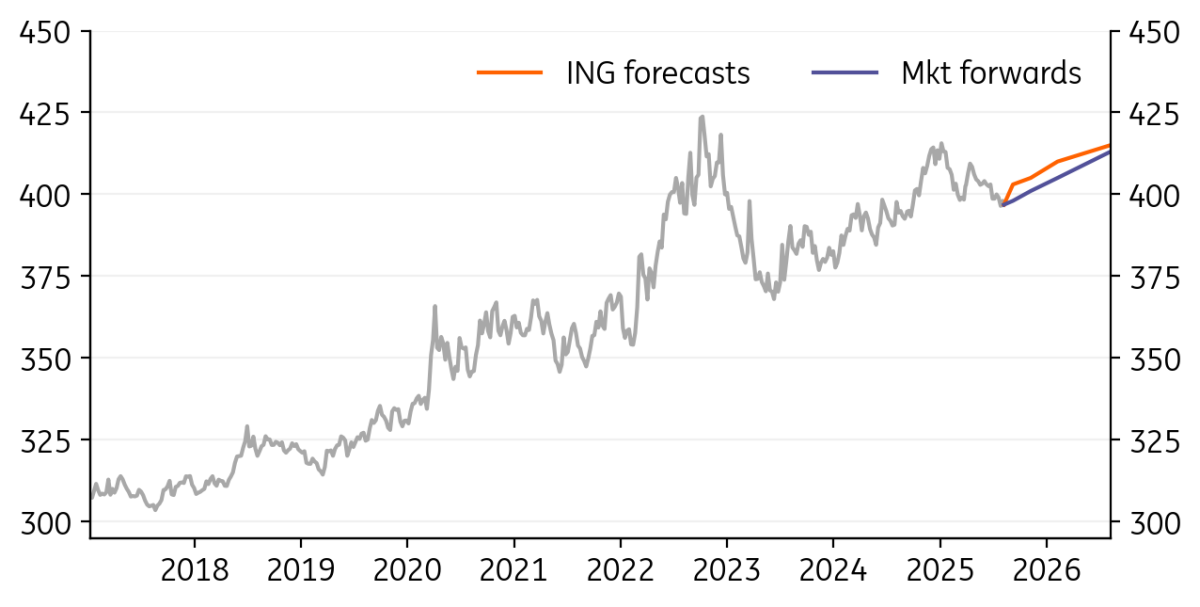

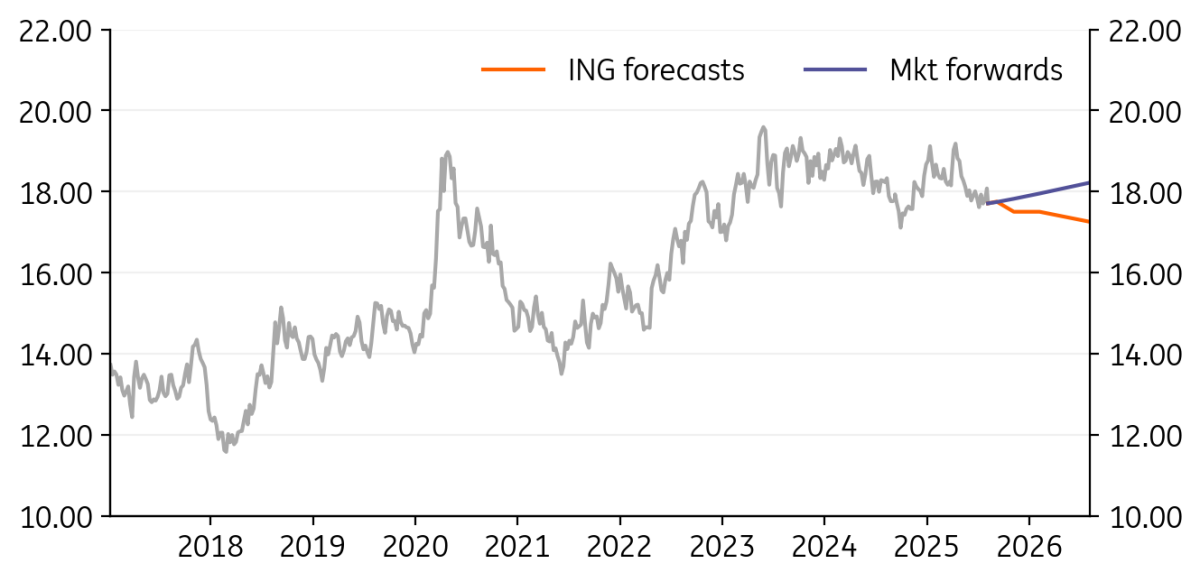

EUR/HUF: Summer calm supports forint, but risks loom ahead

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

396.80

|

Bullish | 403.00 | 405.00 | 410.00 | 415.00 |

- At the end of July, the forint enjoyed the lowest EUR/HUF levels since September 2024, and we have only returned to the 399-400 range because of the July rally in the US dollar.

- If markets return to a risk-on mood, we can't rule out further moves below 399 in the short term. However, the market has largely priced out rate cuts in recent weeks, supporting stronger FX, and we don't see room for another durable boost from this side soon.

- Conversely, the macro story suggests rather dovish market sentiment despite our flat base rate forecast. In particular, lower inflation prints over the summer will put pressure on EUR/HUF to return to the 405-410 level in the second half of this year.

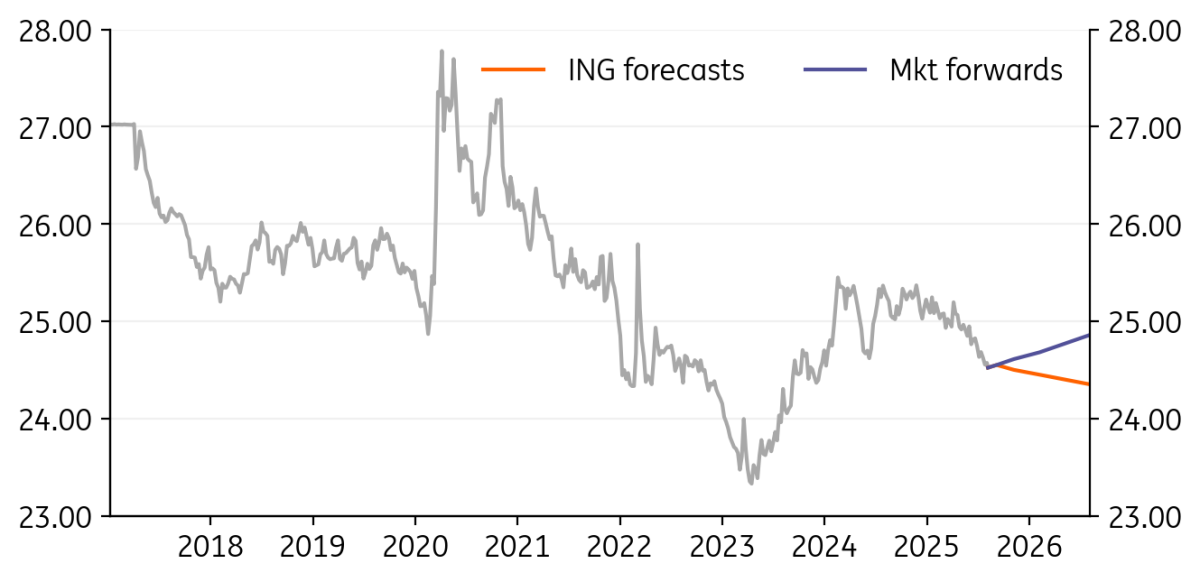

EUR/CZK: Growth performance and inflationary risks help CZK

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

24.52

|

Neutral | 24.55 | 24.50 | 24.45 | 24.35 |

- The economic rebound remains on track in the Czech Republic, despite the erratic impact of net exports. Consumption continues to be propelled by robust wage growth, and the construction boom will also help household budgets. Industrial production growth has remained in the black since February, suggesting that manufacturing has put the worst behind it. Growth outperformance will provide solid ground for the koruna.

- The Czech National Bank's easing cycle is likely over, as future inflationary pressures take centre stage. The possibility of overheating in the housing market, driving core inflation, and the potential for a German upswing, bring the next CNB hiking cycle into view. Both the real economy and monetary stringency point to further, yet gradual, koruna appreciation.

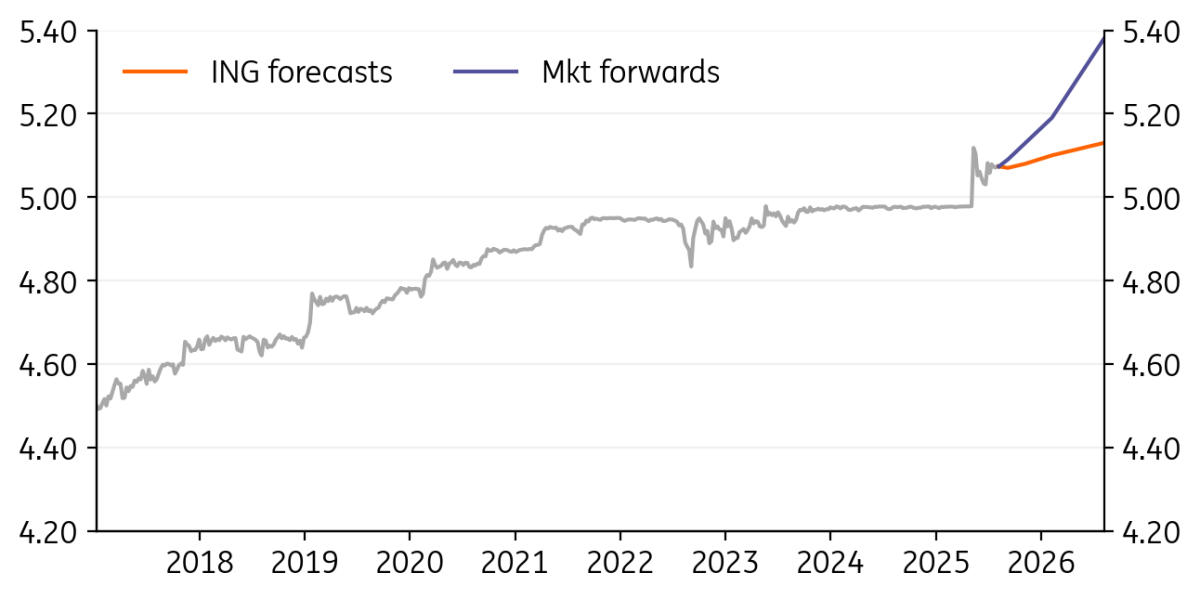

EUR/RON: EUR/RON steady as S&P reaffirms rating

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

5.0735

|

Neutral | 5.07 | 5.08 | 5.10 | 5.13 |

- EUR/RON continues to trade quietly within the 5.07–5.0850 range, suggesting a period of consolidation. This appears to be a comfort zone for the pair, with limited market catalysts and subdued volatility following the post-election normalisation.

- S&P reaffirmed Romania’s investment-grade rating (BBB-) with a negative outlook on 23 July, citing persistent fiscal risks despite recent consolidation efforts. The adoption of the fiscal package has helped ease short-term concerns, but structural imbalances remain a medium-term concern.

- The National Bank of Romania has kept its key rate unchanged at 6.50% in July, and we expect this stance to persist through year-end. Short-term moves in EUR/RON are likely to remain contained within the 5.05–5.10 band, with the pair seen ending the year near 5.10.

EUR/RSD: Policy caution supports dinar stability

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.15

|

Neutral | 117.18 | 117.20 | 117.20 | 117.21 |

- EUR/RSD has remained stable, trading in a tight 117.10–117.20 range through early August. This reflects Serbia’s robust macroeconomic fundamentals, including steady infrastructure investment and prudent fiscal policy.

- At its July meeting, the National Bank of Serbia held the key policy rate steady at 5.75%, maintaining its cautious stance amid global uncertainties. Headline inflation stood at 4.6% in June, printing just outside of the NBS’s 3±1.5% target band for the first time since January this year.

- We expect the NBS to maintain its focus on exchange rate stability. With no major shifts anticipated in EUR/RSD, consistent policy and strong fundamentals should keep the pair anchored near current levels.

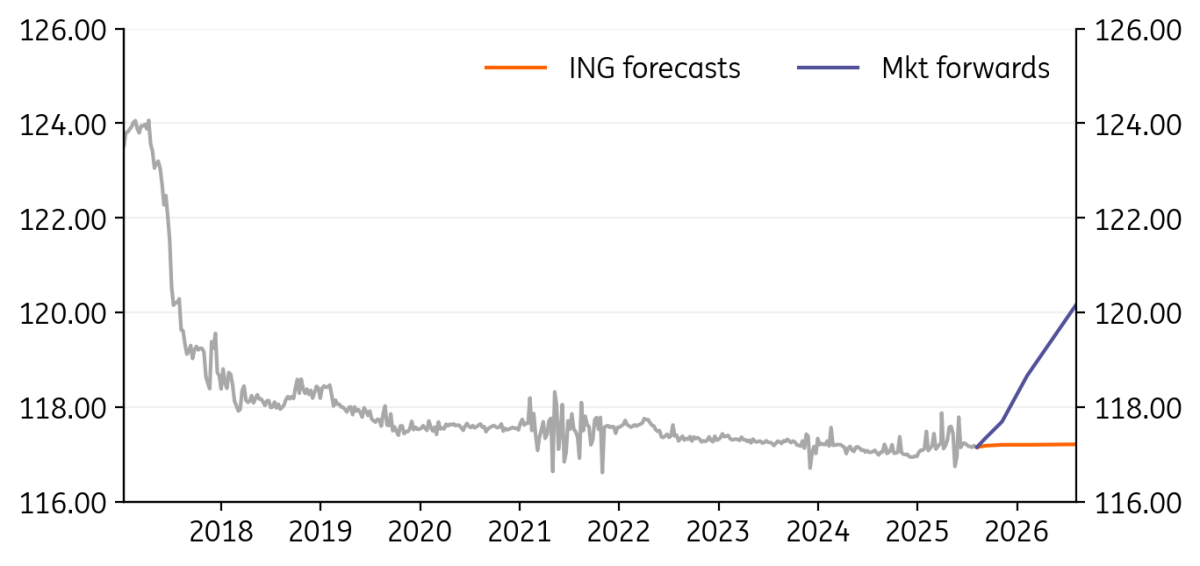

USD/UAH: Another month of insignificant hryvnia fluctuation

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

41.46

|

Mildly Bullish | 41.80 | 41.70 | 41.60 | 41.30 |

- For another month, the hryvnia exchange rate against the dollar remained broadly stable (tight range of 41.0–41.8) thanks to inflows from international aid. According to the National Bank of Ukraine, this year alone, Ukraine is expected to receive external financial assistance in the amount of around USD$54bn, of which the country has already received less than half.

- Although the NBU left interest rates unchanged in July, the central bank’s previous efforts to tighten monetary policy have contributed to the stabilisation of the hryvnia. Notably, the latest NBU forward guidance - reflecting the revised macroeconomic forecast - indicates a sustained pause in the key policy rate at 15.5%, its highest level since 2023.

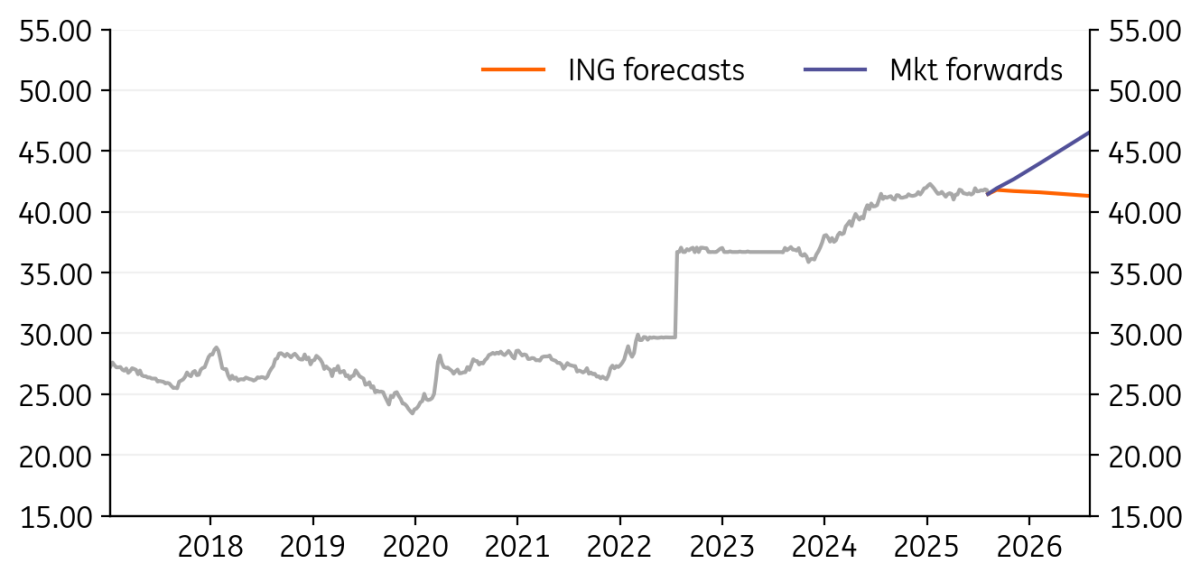

USD/KZT: State capital flows fail to support FX market

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

539.03

|

Mildly Bearish | 530.00 | 535.00 | 540.00 | 550.00 |

- The tenge weakened by 3.9% to 541 per US dollar in July despite a benign macro backdrop, triggering emergency FX interventions of US$126m. The total net government net FX sales went up to US$1.4bn in July from US$1.0-1.1bn in the preceding months.

- The balance of payments for 2Q25 shows that the state capital inflows are being increasingly outweighed by the mounting current account deficit and weakening private capital inflows.

- The double-digit growth in oil production in the second quarter, including 18% YoY in June, may eventually be converted into exports, potentially supporting the tenge in the near term. But longer-term strengthening is less likely given the structural BoP challenges.

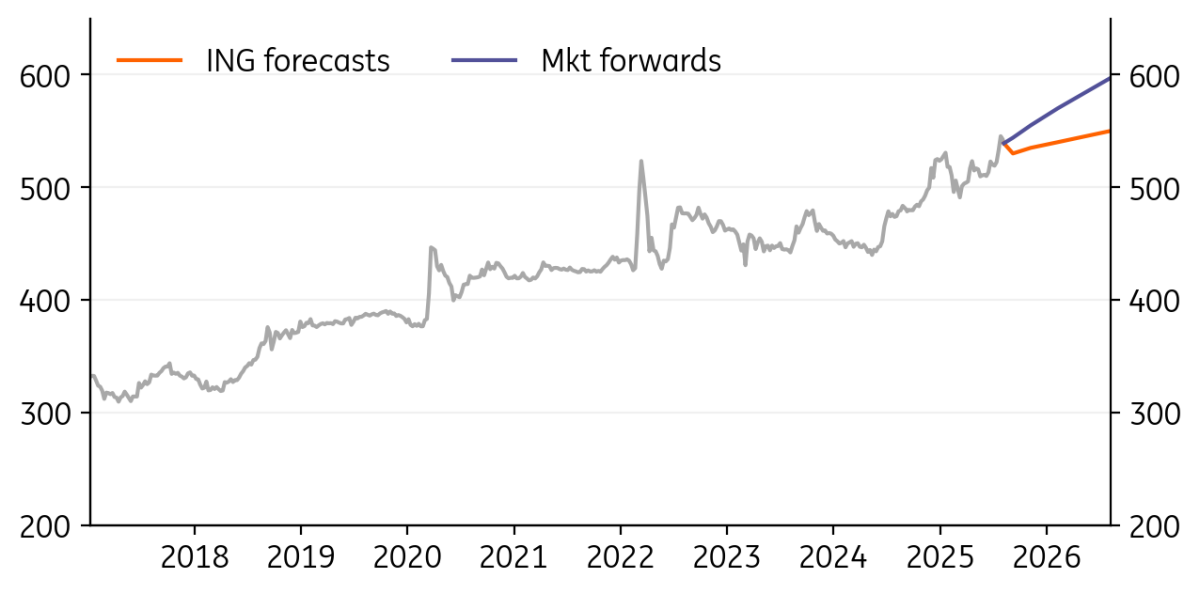

USD/TRY: A more rapid TRY depreciation recently

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

40.64

|

Mildly Bullish | 41.70 | 43.60 | 45.90 | 50.25 |

- Recent movements in the USD/TRY exchange rate suggest a quicker pace of lira depreciation, with an average monthly increase of 1.8% in the last three months. The depreciation is even more pronounced when looking at the FX basket (50:50 EUR/USD), which saw increases of 2.9% in June and 2.6% in July.

- Accordingly, the lira’s real effective exchange rate has turned more supportive for Turkey’s competitiveness. In fact, the CPI-based REER has declined from above 75 in January 2025 to 69.4 as of July. The possibility of the Central Bank of Turkey accelerating its interest rate cuts could weigh on the lira. Even in such a scenario, relatively high real interest rates and ongoing de-dollarisation tendencies will continue to support the lira.

- Additionally, the CBT is not likely to allow a rapid TRY depreciation, as this would undermine its disinflation strategy and could potentially trigger renewed dollarisation. We think the CBT appears prepared to manage any potential FX pressures that might arise from a faster pace of rate cuts in the coming months.

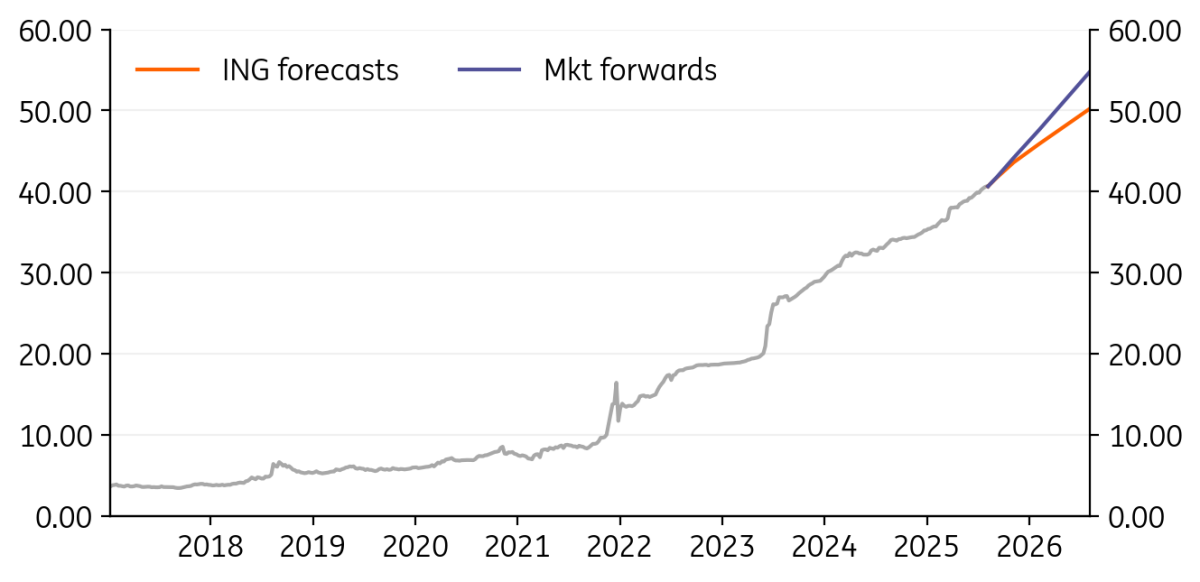

USD/ZAR: SARB unilaterally shifts to new 3% inflation target

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

17.71

|

Neutral | 17.75 | 17.50 | 17.50 | 17.25 |

- At its meeting in late July, it seems the South African Reserve Bank has unilaterally taken the decision to shift to a 3% inflation target from a 3-6% range prior. In theory, this decision should have been taken in conjunction with the Finance Ministry but may well get confirmed in October.

- The SARB models that a 3% target will deliver a stronger ZAR and allow policy rates to be cut another 125bp – far more than if a 4.5% CPI target were retained. This story has been helping flows into the local bond market – SAGB yields are at a three-year low.

- 30% US tariffs will be a hit to the SA auto and agricultural sector and will likely keep growth low and unemployment high.

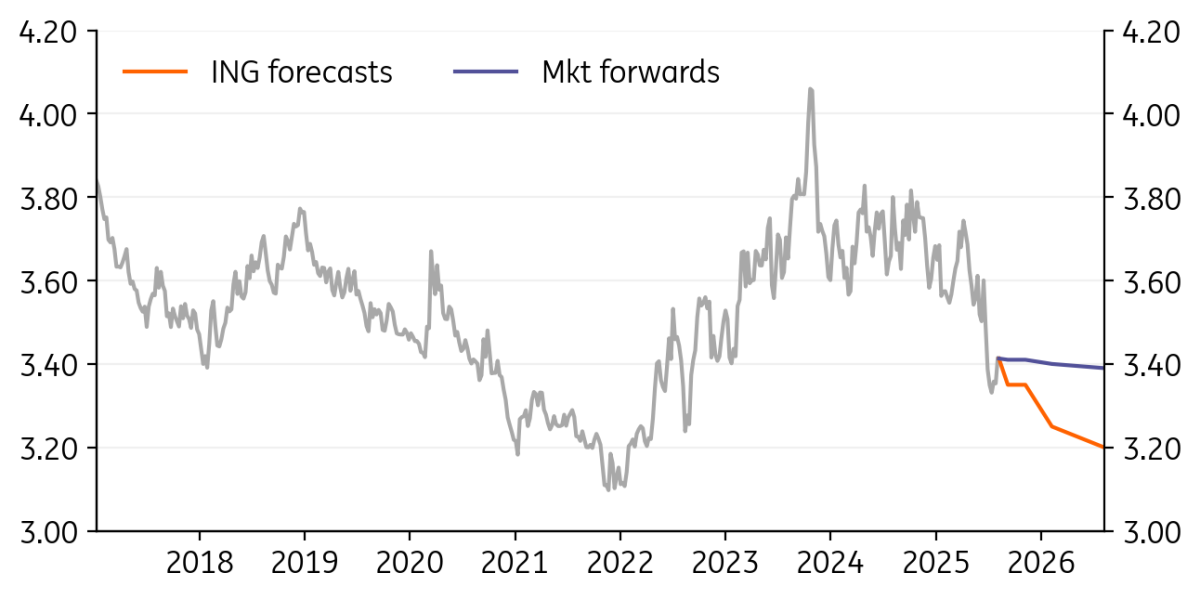

USD/ILS: Shekel holds onto 2025 gains

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.413

|

Mildly Bearish | 3.35 | 3.35 | 3.25 | 3.20 |

- USD/ILS has corrected alongside the dollar complex in July and should presumably drop again if we’re right about a weaker dollar in August. Reduced sovereign risk premia after the joint US/Israeli attack on Iran is still helping and any ceasefire in Gaza will be viewed through the lens of improving Israel’s supply side challenges – particularly with the stretched labour force.

- Last month, the Bank of Israel kept rates at 4.50% and seemed to welcome the strong shekel in weighing on inflation. The market prices a 75bp easing cycle over the next year.

- USD/ILS has in the past been a high beta trade on the global dollar trend and should be back on the lows at 3.25/30 by year-end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

FX Talking: Cracks in the dollar’s shield

- This bundle contains 6 Articles