CNB preview: Rates set to stay on hold as Hormuz bites

- 30 April 2026

- Czech Republic

Inflation has picked up recently, while economic growth has slowed. The Czech National Bank will likely respond with no change in rates for as long as it can. Hawkish talk should suffice in our baseline scenario, yet should things turn uglier, one cosmetic hike would likely be due to reinforce the message. Still, no one wants to be seen as choking off growth

CNB can proceed lege artis

Czech policymakers will likely keep the policy rate unchanged at 3.5% at next Thursday’s meeting, though inflation has picked up and is set to increase further. The current turmoil in the Middle East will have twofold implications: higher prices on the one hand and weaker global economic performance on the other. The CNB knows the basic macroeconomic business rather well and finds itself in a relatively comfortable situation vis-à-vis the negative external supply shock, which allows it to wait things out as long as it can to see how the various effects compound.

As Jakub Seidler puts it: “I can still imagine that we will get through the current situation without the need to increase rates.” A call for restraint echoes across the board, for example with Eva Zamrazilova: “Rates are where they should be and have a real positive return. So, we really don't have to rush.” We are very much aligned with this way of thinking, as this type of negative supply shock is in essence beyond the CNB’s control, and central banks should ideally look through the current volatility as much as possible.

Protracted conflict means higher inflation

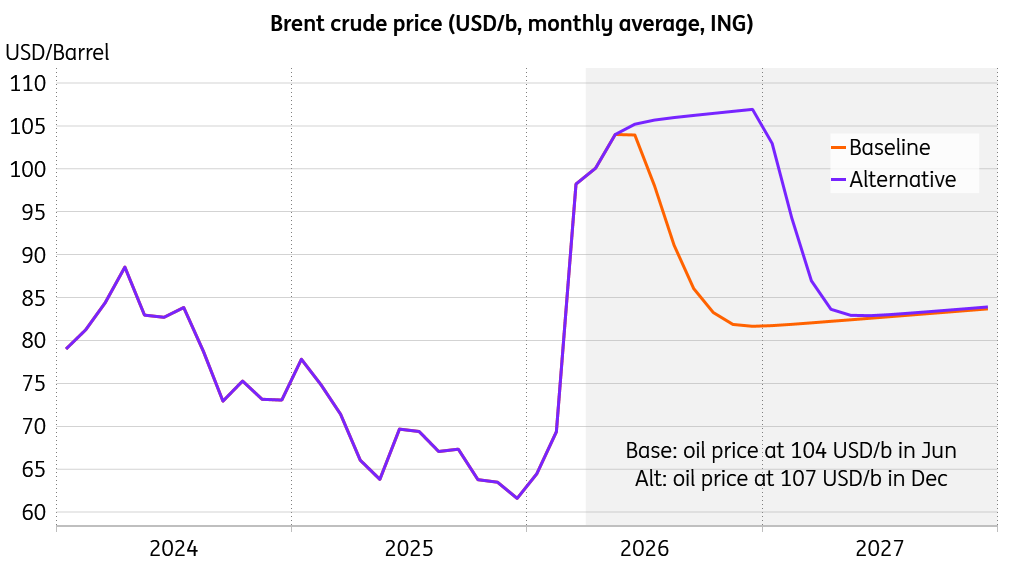

We have updated the Czech inflation path, the key macroeconomic variable for a forward‑looking central bank’s monetary policy. We currently assume that the conflict in the Middle East lasts until June in the baseline scenario, with Brent crude monthly average prices remaining at USD 104/bbl until that time. From July onwards, the situation may calm down, with Brent crude receding gradually to USD 82/bbl by November. A similar path is assumed for natural gas prices, while the koruna is expected to be weaker from May onwards compared with our previous forecast.

Oil price flies high

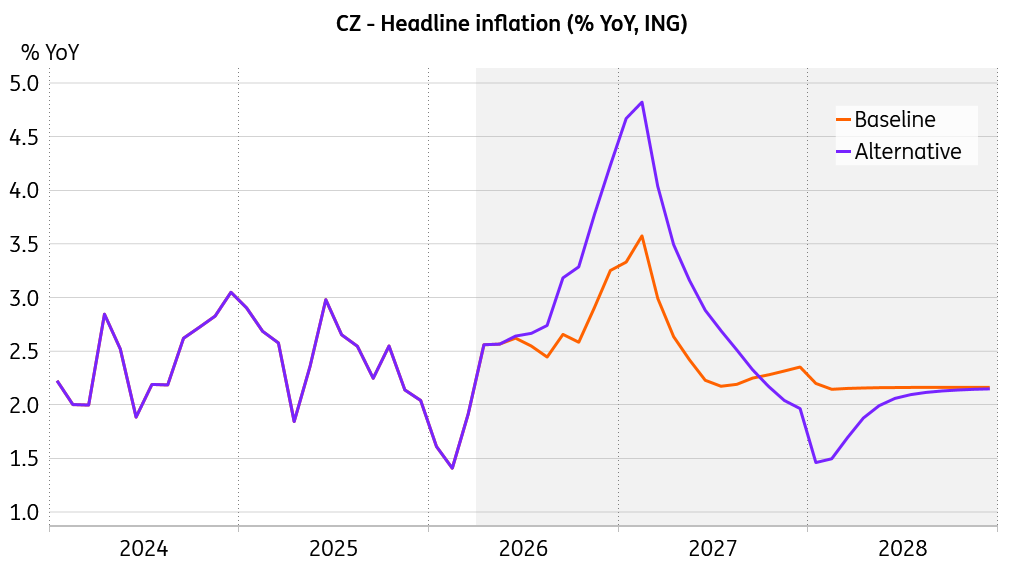

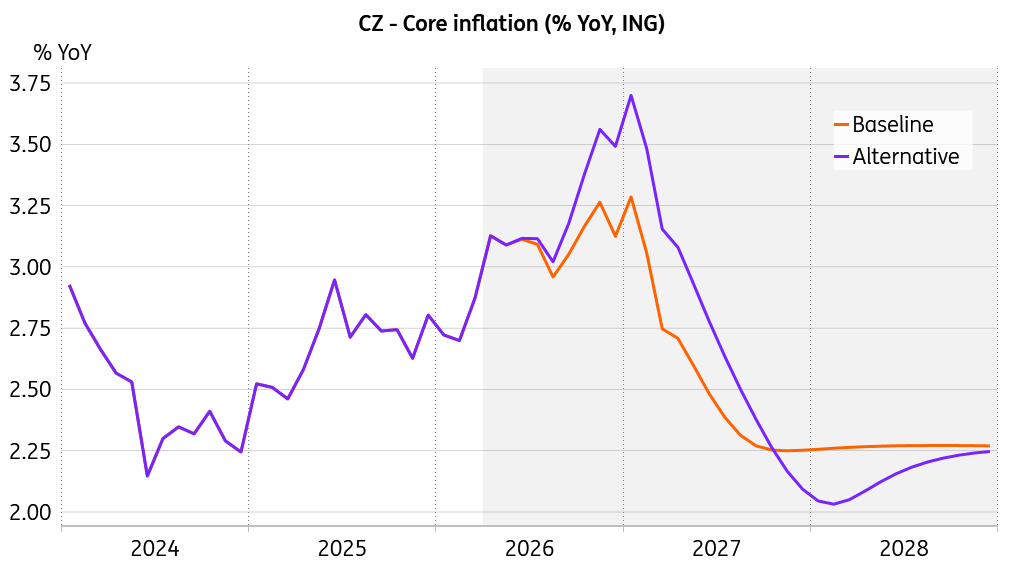

This assumes the conflict lasts two months longer than in our previous forecast, pushing average headline inflation to 2.4% this year and 2.6% next year. In such conditions, core inflation would average 3% this year and 2.6% next. Headline inflation is set to peak at 3.6% early next year with the core rate at 3.3%. I assume that the CNB would do the right thing and refrain from touching rates, given this is a negative external supply shock, and pressure for economic activity will follow suit.

Inflation set to peak early next year

Should the conflict drag on till the end of the year, and Brent crude crawl to a monthly average of USD 107/bbl in December, more non-linearities would kick in, while headline inflation would average 2.7% this year and 3.1% the next. Core inflation would average 3.1% this year and 2.8% the next. In such a case, the situation becomes more complicated for the CNB, as headline inflation would peak at 4.8% early next year and the core rate at 3.7%. Some members would likely vote for a hike to confirm the hawkish talk. However, economic growth would likely slow down to some 0.1% quarter-on-quarter in some periods. We therefore expect only a cosmetic hike from September onwards, signalling that actions can follow words. This would require a delicate balancing act in communication and forward guidance.

Core inflation about to gain pace

Economic expansion at risk

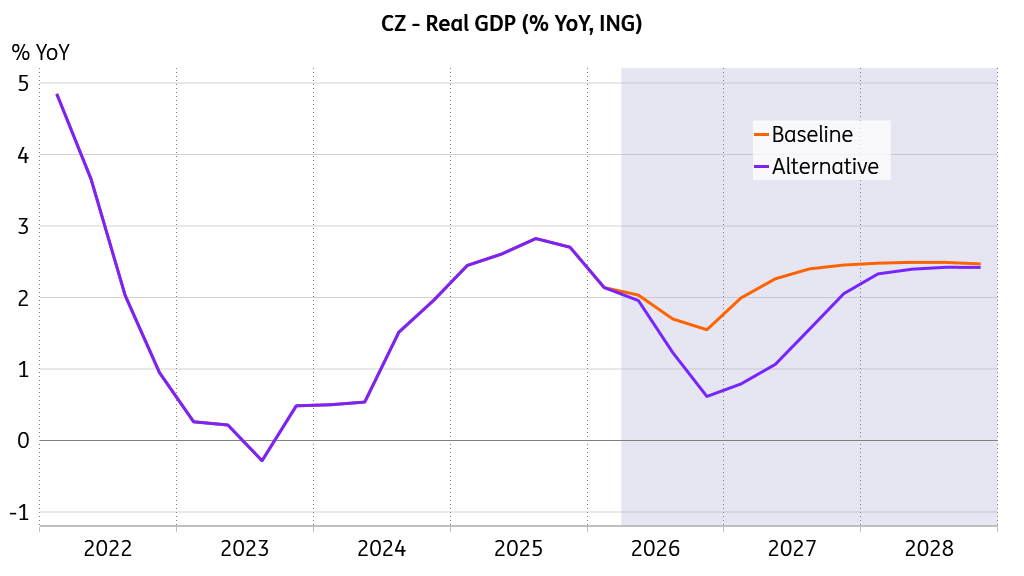

Czech real GDP gained 0.2% QoQ in the first quarter, according to preliminary estimates, implying 2.1% annual growth. The quarterly expansion was positively affected primarily by growing gross capital formation, yet we assume that an increase in inventories made a considerable contribution. We expect that firms will postpone or alter their investment plans due to increasing energy prices and uncertainty in the coming quarters, but let’s wait for the 1Q26 detailed breakdown. The foreign trade balance made a negative contribution to quarterly GDP growth. Such an outcome aligns with the quarterly increase in gross value added being driven by the service sector, while industry recorded a negative impact. Employment remained unchanged in quarterly terms and added 0.7% from the previous year.

Inter arma silent musae

The reading came in well below market expectations, as Hormuz is likely starting to bite. This is consistent with our position that the Middle Eastern turmoil will have tangible negative consequences for economic activity. We just didn't assume such a stark impact would be felt so soon. Still, we must wait for the expenditure breakdown to proceed with a solid analysis. Overall, we maintain our position that the current negative supply shock will have tangible implications for the global economy, and we still believe that most institutions are underestimating the pressure. Taking on board the latest GDP figure, we lower our Czech economic expansion pace to just below 2% this year and to 2.3% next year in the base case scenario. However, in the adverse scenario, GDP growth might only reach 1.5% this year and 1.4% next.

Hard to play without accessible energy

With Czechia representing an industrialised, energy-intensive, export-driven economy, this is not good news either right now or when looking ahead. The European Commission president's observation that the cheapest energy is unused energy is peculiar to put it mildly, as opportunity costs should always be at the top of policymakers' minds. I believe that the opposite is ultimately true. If you cannot proceed as usual in tough times, you only demonstrate your weaknesses, and your competitors will eat you alive. The old saying holds for Europe once again: Vanitas vanitatum et omnia vanitas.

For sure, the CNB is an experienced institution and knows how to proceed lege artis during an external negative supply shock, which is far beyond its control. We will hear plenty of hawkish talk around an unchanged base rate, as nobody wants to push the economy to its knees. A silver bullet of a single hike would show that policymakers are prepared to walk the walk and back hawkish rhetoric with action, with words doing most of the work until late in the cycle. In an adverse scenario, policy could take on a full‑metal‑jacket stance in terms of holding the line. Should the European Central Bank give in to temptation and enter the waters of a potential monetary policy mistake by raising rates ante portas, the CNB is not likely to follow suit.

Our market view

The Czech koruna has been trading in narrow ranges since the beginning of the US-Iran conflict, and we have not seen much pressure to weaken. Despite the fact that the conflict has dragged on, FX remains stable, and we have seen EUR/CZK bouncing in the range of 24.250-550. This suggests limited central bank focus on the exchange rate and provides a buffer for any potential ECB hike or escalation of the conflict. At the same time, we do not see much reason to expect a stronger koruna under current conditions. The market is pricing in almost 100bp of rate hikes, so the CNB can't surprise too much on the hawkish side. We therefore expect EUR/CZK to remain range-bound for a longer period of time with potential upside risk in the short term if the US-Iran conflict escalates and the CNB refrains from hiking rates for a longer period of time, opting not to follow the ECB.

The rates market, on the other hand, was where the whole story unfolded. It seems that the market views the CNB as both the most sensitive to ECB moves, and, traditionally, the first central bank in the region to react to rising inflation. As a result, the CZK market is pricing in the largest number of rate hikes in the EMEA region, together with South Africa.

At the moment, we do not expect rate hikes from the CNB, but at the same time, we do not expect the market to fully unwind all expectations even if the conflict were to end immediately. First, hawkish pricing at the ECB level is likely to keep CNB hikes in play for longer. Second, the second-round effects, including higher food prices later on and already elevated core inflation, will sustain at least some hope of a CNB hike.

That said, pricing in four hikes still looks stretched relative to CNB rhetoric. Assuming at least some near‑term de‑escalation, the front end of the curve should go down first as part of a relief trade. Over time, we would then expect further flattening due to the economic slowdown and a CNB that remains “ready to hike.” This should make the long end of the curve attractive, both in IRS and in CZGBs, given current elevated levels.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more