Czech National Bank Minutes: domestic factors require tight monetary policy

- 25 June

- Czech Republic

Solid wage dynamics, elevated core inflation, and lofty credit growth are the main reasons behind the Czech National Bank's latest rate increase. Our inflation forecast suggests a rather benign profile when looking ahead, which leads us to favour no change in rates for some time. Should core inflation get out of hand, another hike would become more likely

Labour market and credit are pro-inflationary

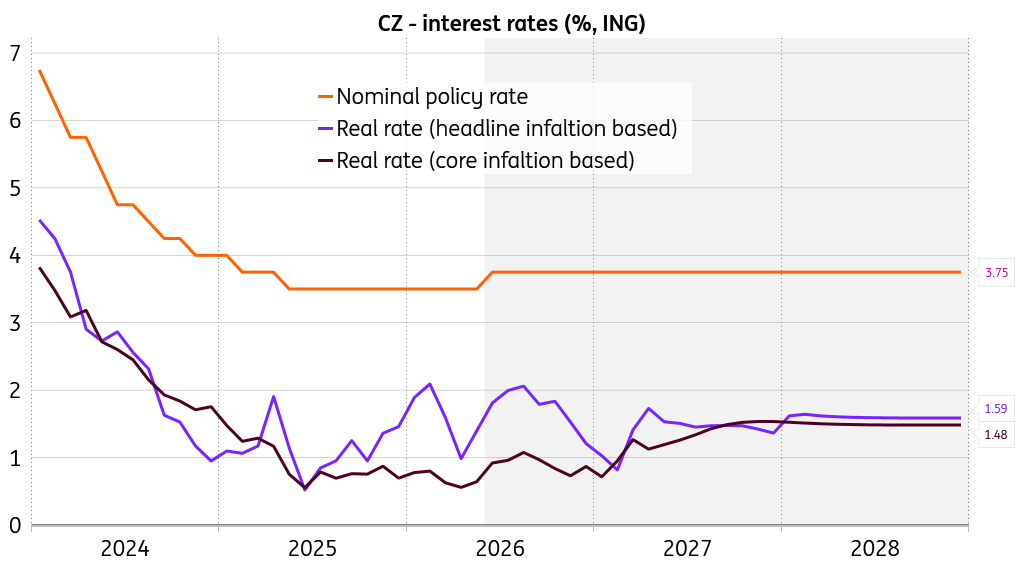

The CNB increased the policy rate by 25bp to 3.75% at its June meeting in a six-to-one vote. The Board assessed the overall risks as pro-inflationary. Governor Ales Michl initially emphasised the need for a hawkish stance to maintain price stability. He sees risks in the development of loans, debt financing of public spending, and the path of core inflation. The minutes clearly state that the reasons for the rate increase are primarily related to the development of the domestic economy.

There was consensus that the Czech economy is in a relatively comfortable situation, with solid economic growth – not overheating, but operating close to full capacity. At the same time, real interest rates are expected to remain positive. It was repeatedly stated that some secondary effects on prices cannot be avoided in light of the Middle Eastern conflict. That said, the task of the central bank is not to react to the primary impacts of the cost shock.

According to Eva Zamrazilova, strong domestic demand is generating inflationary pressures, particularly in the services sector, including housing, construction work and materials. Consumption is being driven by rapid wage growth, which shows little sign of slowing. There were also some signals related to the planned 11% increase in the minimum wage, although this affects only around 2% of employees. Jan Frait also stated that the labour market has shown signs of strong tension over a longer horizon, partly due to structural factors, including demographics. Meanwhile, Jan Prochazka sees wage developments as the most important factor that has limited scope for rate cuts in the past and these are now pointing towards higher rates.

Real interest rates to move above 1%

It was emphasised that the accelerating pace of credit growth is leading to an excessive expansion in the amount of money in circulation. According to Jakub Seidler, current credit activity does not suggest that interest rates are overly restrictive. The current credit boom is seen as a combination of increased lending today and planned future real estate purchases by the private, public and semi-public sectors. The rise in short-term financing costs should send a signal that monetary policy does not favour speculative behaviour in asset markets.

Likely not a genuine hiking cycle

Part of the discussion was devoted to the timing and extent of the interest rate change, with incoming data providing little room to wait, should the monetary policy setup remain restrictive. One hike was deemed an appropriate step in response to the change in the balance of risks and the need to support the degree of monetary restriction. The rise in rates does not herald the beginning of a genuine hiking cycle, but it cannot be said that June’s increase was the last. Several members also mentioned the signalling effect of an increase in interest rates.

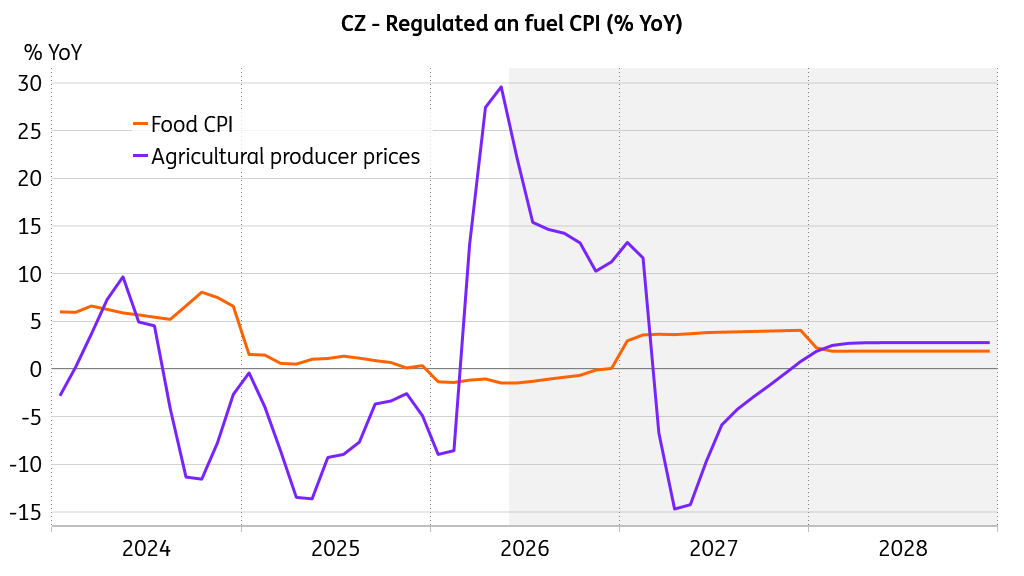

Fuel prices to push headline inflation lower

On the other hand, Karina Kubelkova did not consider the benefit of a preventive increase in rates in today’s dynamic situation to be unambiguous. One of the main pro-inflation risks is beginning to abate along with the easing of tensions in the Middle East. This allows time to wait for new information and link monetary policy tightening to the summer forecast. She considered the risk of a monetary policy error associated with leaving rates unchanged as acceptable given the level of uncertainty. And indeed, Karina Kubelkova was the one who voted for keeping rates on hold in June.

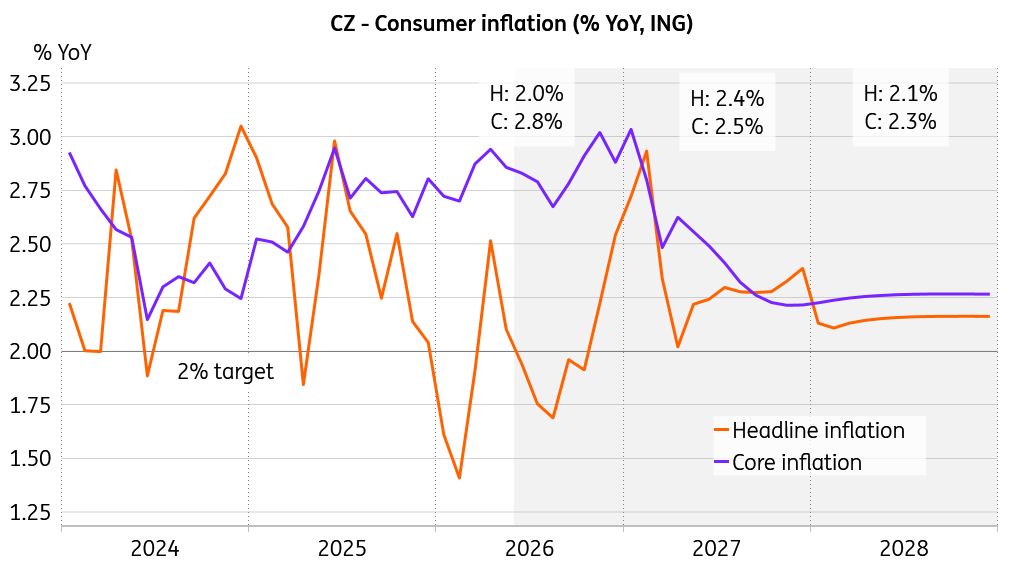

Headline inflation to hover around the target

Plugging in the opening of the Strait of Hormuz and Brent crude prices recently heading toward USD 70/bbl, we get a much milder profile for fuel prices, which brings this year’s headline inflation to 2% on average. In agriculture, while part of the sharp 4.3% month-on-month fall in May producer prices – the steepest decline since the end of 2023 – is likely to reverse in the coming months, the drop was large enough to keep prices in annual decline into early next year, posing continued downside risks to food inflation.

Headline and core rates go their own way

Core inflation is set to remain elevated up to the first quarter of the coming year according to our forecast, driven by robust nominal and real wage growth along with a continued willingness to spend. We still assume some dampening effect on economic activity from the Middle Eastern conflict, which will imply some easing in wage growth when looking ahead. Along with expected softer growth in house prices on the forecast horizon, we expect core inflation to gradually recede from 2Q27 onward. Yet indeed, we must acknowledge that there is a risk that the economy will prove perfectly resilient, and the housing boom, as well as lofty rent increases and punchy core inflation will prevail. We could see this scenario evolving if the economy were to expand by 2.5% or more.

Producer prices in agriculture remain in decline

For next year, we assume headline inflation to average at 2.4%, partially reflecting solid figures from the onset of the year that are driven by this year’s low comparison base. At the same time, we still take on board the 3.8% average growth rate of regulated prices, which might be somewhat less, should global energy prices remain benign.

With all that said, we see the June hike as an insurance move to protect the CNB’s credibility should we witness an extraordinarily resilient economy and wage dynamics. Issues related to independence and the government’s pressure for less tight monetary policy perhaps also played a role. With the relatively favourable inflation outlook, we take it as one and done, especially if we see some deceleration in core inflation. Nevertheless, should core inflation increase, another hike in August would become increasingly likely.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more