Czech industrial prices rebound as supply shock takes hold

- 20 May 2026

- Czech Republic

Industrial prices in Czechia have firmed, with rising energy and input costs starting to push up production prices. The negative implications for economic performance are about to become more tangible, somewhat limiting the scope for tighter monetary policy. As conditions worsen, the divide between winners and losers is likely to become more apparent

Prices in industry return to growth

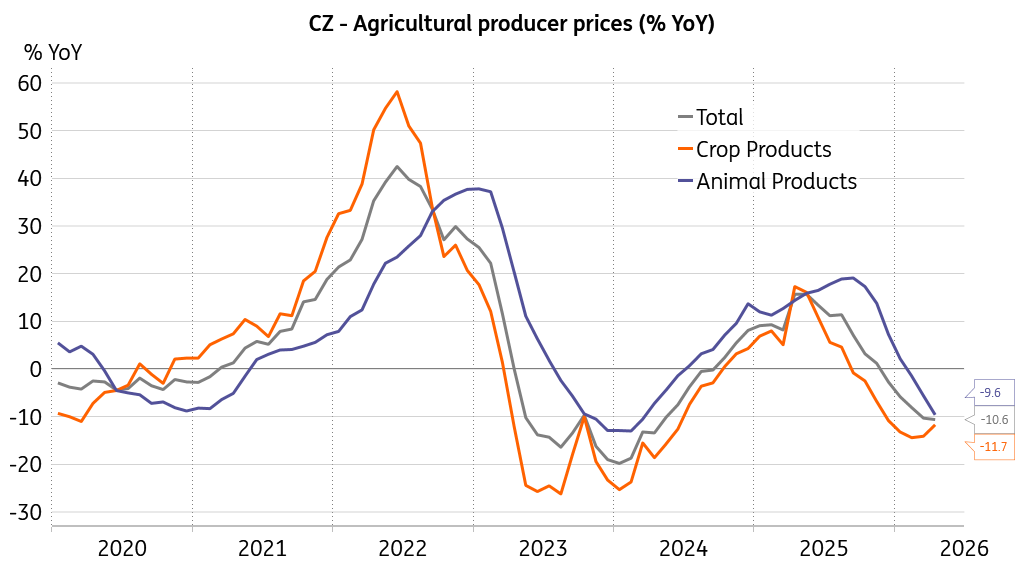

Czech industrial producer prices increased by 1.4% month-on-month in April and flipped to annual growth of 1.0% after more than a year of contraction. The reading came in stronger than market participants had assumed. Agricultural producer prices gained 2.8% MoM, yet their annual downturn deepened to 10.6%. We are more focused on the strong monthly momentum, which exceeded our forecast, and expect upside risks to food prices to materialise in the coming months.

Construction prices remained unchanged from the previous month in April and added 3.2% from a year earlier, but rising energy and material prices may add to upward pressure when looking ahead. Prices of market services for businesses gained 0.6% MoM and 3.2% year-on-year. And yes, we will likely see some trade-off pressure in this segment, as firms are set to face higher energy costs, potentially combined with waning demand, severe competition, compressed margins, and fading profitability.

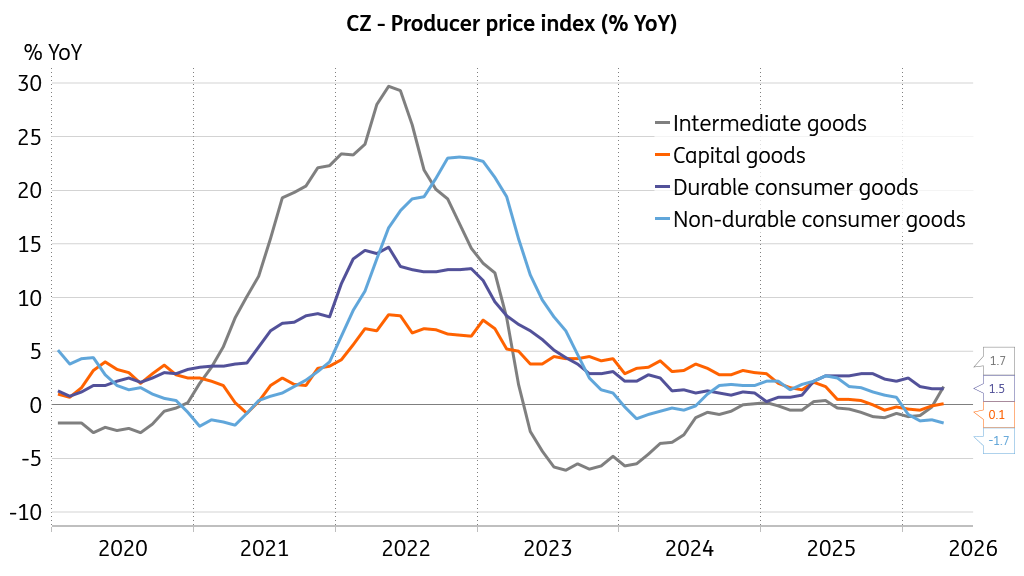

Rising input costs drive intermediate production prices

Indeed, we are seeing the classic response of production prices to a negative global supply shock. Intermediate goods prices have switched firmly to annual and monthly growth, propelled by surging input costs. Meanwhile, prices of non-durable goods posted a more severe annual decline in April, as their monthly increases are being held back by rising uncertainty about future sales performance.

Shock separates the wheat from the chaff

We are likely to see more of this counter-movement. An extensive and protracted negative supply shock typically produces the worst mix: less output at higher prices. However, if consumers lose confidence and rein in spending, be it due to tightening budgets or out of precaution, softer demand would make competition pressures far worse, potentially setting the scene for an unpleasant period of adjustment until the market rebalances.

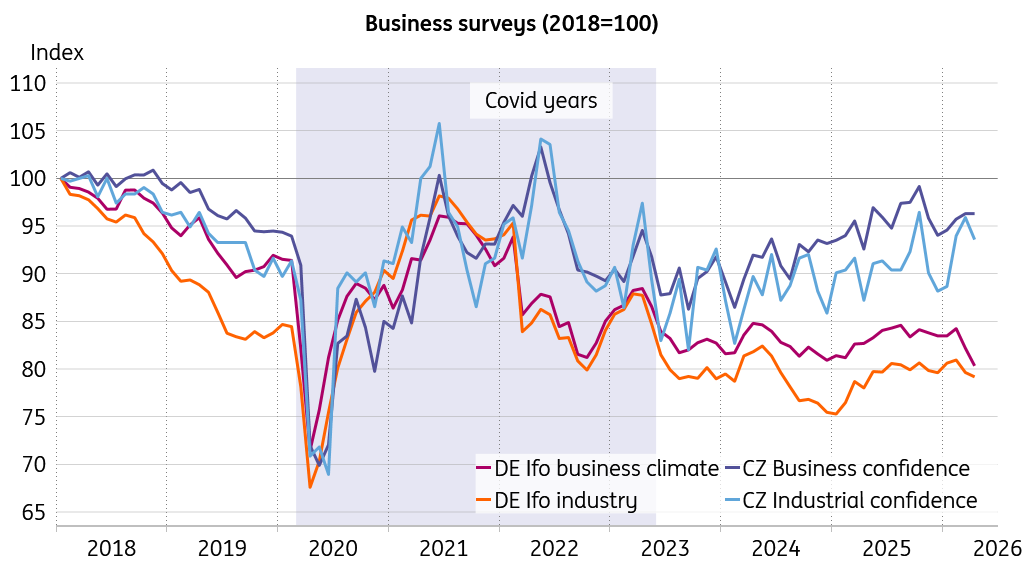

Mood in European industry likely to suffer

We will see who ultimately shares in the gains with the winners and who is left picking up the scraps under the table in conditions of cut‑throat competition in our global village. My guess is that i) a robust energy strategy and ii) the ability to shape the economic landscape in favour of domestic firms are key pieces of the puzzle. And here, I am not sure that Europe has the willingness and the ability to withstand another raw fight, with its mindset still anchored in a softer, slower-moving world that no longer exists.

Adverse effects for real economy will reduce scope for rate hikes

I take the side that the current turmoil will have tangible, harmful effects not only on price levels, but also on economic performance. The fact that the negative impact on the real economy is not here now, doesn’t mean that it will not arrive soon. Therefore, I see less space and propensity for monetary policy tightening than generally proposed. The higher share spent on mandatory items such as energy and foodstuffs due to price increases does not mean higher real consumption. On the contrary, it leaves less room for discretionary spending on durable goods and services, with significant implications for aggregate demand. As prices rise, households’ real purchasing power simply erodes.

Pricing in agriculture set to take a turn soon

The Czech National Bank is likely to remain in a position where it can afford to wait until there is greater clarity on the adverse implications for economic growth. Policymakers can then proceed with a more informed decision and avoid a potential policy mistake, particularly at a time when high capital costs could amplify the global malaise and push the Czech economy to its knees. We expect the output gap to turn negative again soon, leaving the economy operating below potential. As we know, feedback loops are at work – akin to the so‑called Matthew effect, reinforcing both the upswing and the downturn.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more