Czech industrial prices fall, but oil turmoil transforms outlook

- 16 March

- Czech Republic

Pricing in production sectors has winners and losers. Nevertheless, the current turmoil in the Middle East is likely to generate price pressures across all segments. Our analysis shows two qualitatively different paths for consumer inflation and two possible worlds for the Czech National Bank

Services and construction prices rise

Czech industrial producer prices increased by 0.1% month-on-month but were down 2.9% year-on-year in February. Agricultural producer prices fell by 1.6% MoM and by 8.1% YoY in February. On the other side of the spectrum, construction prices added 0.5% MoM and 2.7% YoY. Prices of market services for businesses picked up by 1.5% MoM and 3.4% YoY.

Two-way dynamics in production segments

On a monthly basis, prices of coke and refined petroleum products saw a notable increase in February, foreshadowing the energy‑price turmoil seen in March. Prices of basic metals increased by 0.8% and other non-metallic mineral products were up by 0.5% from a month earlier. In contrast, prices of food products lost 1.2% MoM in February. However, this could easily reverse in the coming months, with the turmoil in the Middle East making all inputs more expensive, be it energy, transportation, or fertilisers. Any disruption to fertiliser supply, particularly during the sowing period and early stages of crop growth, could undermine this year’s harvest and push food prices higher later in the summer.

Oil price rules them all

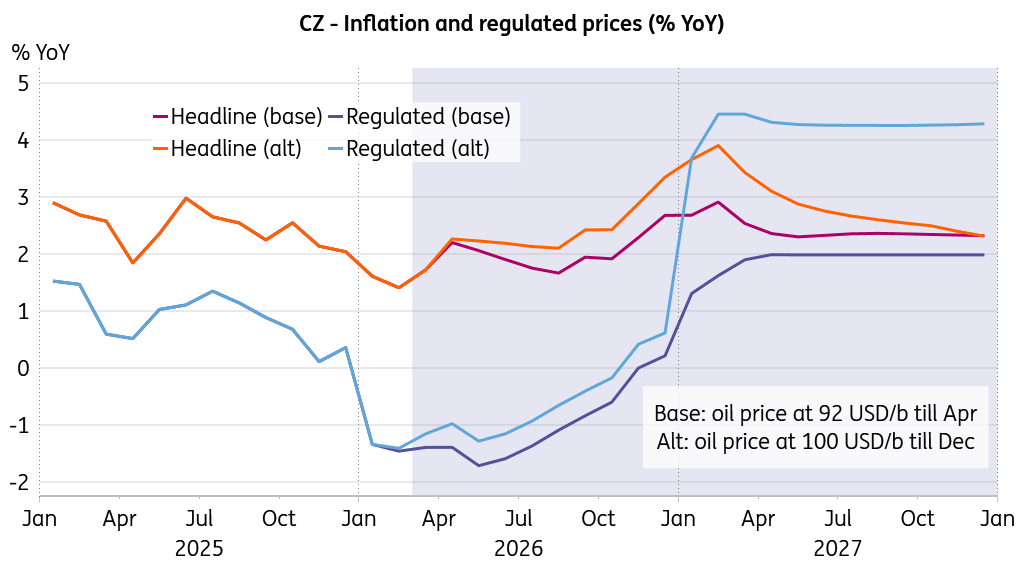

Our headline inflation forecast of 1.9% for this year’s average and 2.7% for core inflation – based on the assumption of the Brent crude price averaging $92/b both in March and April and then gradually receding to a more reasonable level of around $80/b in August – is still defendable. However, should Brent crude prices hover above $100/b until year-end, the outlook would look materially different.

Energy prices affect all price domains

Food and regulated prices, in particular, would become a pressing issue, even beyond 2026, with repercussions for demand, Czech export performance and growth. In such a case, our simulation points to headline inflation at 2.2% this year but 2.9% in 2027, propped up by food and regulated price increases.

Regulated prices will take off if the shock is prolonged

Indeed, this is the classical conundrum of quantitative adjustments transforming into a qualitative shift. Add one grain of sand to another, and eventually, you have a heap. But, as Ovid reminds us, it is impossible to pinpoint exactly when that transformation occurs. That uncertainty gives the CNB scope to kick the can down the road for some time, supported by a comfortable buffer provided by the Czech economy, in terms of both inflation and growth structure.

Two different worlds for the central bank

To be sure, a more extended period of higher oil and natural gas prices will put global economic activity under pressure. The real challenge, once again, lies in the feedback loops. While it is possible to assess the impact at the country or regional level, the cascade of second‑round effects is far harder to gauge. In my experience, most of the global economic models rely on interlinkages that are too weak, meaning they tend to underestimate the true impact relative to what trade‑channel models imply. Indeed, confidence channels and shelving investment projects can have immediate and potentially longer-lasting effects.

When quantitative adjustment turns into transformation in quality

We have argued that monetary institutions in advanced economies are unlikely to allow real interest rates to drift back into negative territory, absent an Armageddon‑type scenario. The question, then, is whether we are moving in that direction. Our base case scenario does not point to an overly challenging environment for the CNB: inflation remains relatively close to target, driven by a negative external supply shock with limited impact on economic activity. In this setting, leaving the policy rate unchanged remains the appropriate response.

Two worlds: Inflation all fine or not really

However, should the alternative scenario materialise, with repercussions for crop yields, food prices and regulated prices, well then, we have inflation well above the target over the forecast horizon. At the same time, the risks of a marked economic slowdown would rise, potentially tipping the economy into recession if conditions were to deteriorate further. The CNB would not face a stagflation scenario, but rather a recession-inflation scenario. Would you increase the cost of capital if the economy were about to contract? Perhaps not. Yet, with inflation approaching 4% in February next year, who knows. In my view, it would hinge on how severely the real economy is hit.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more