Czech economy shows strong domestic fundamentals

- 29 May

- Czech Republic

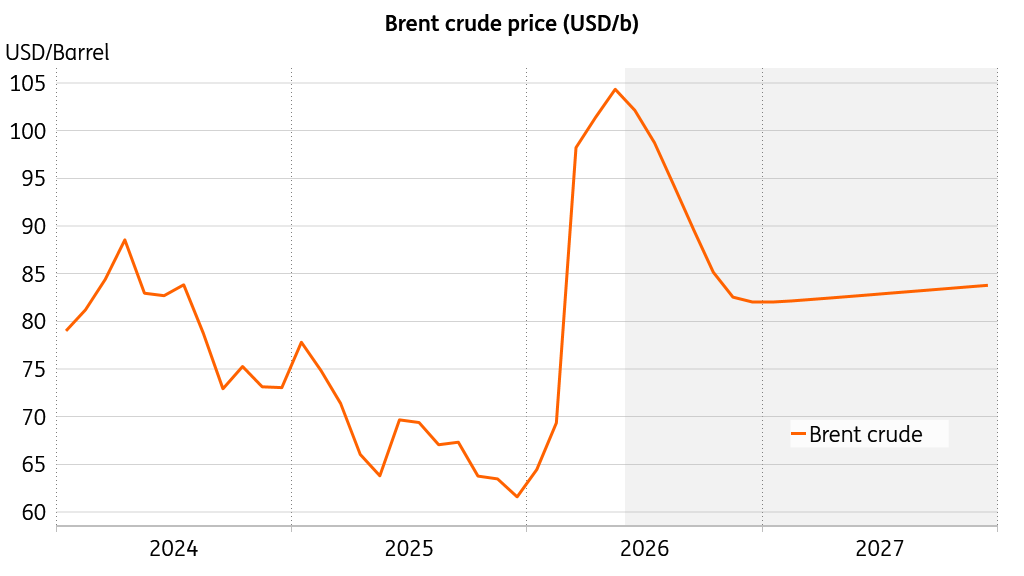

The GDP breakdown brought some upward surprises, especially in fixed investment and foreign trade. Emerging hopes for a resolution to the Middle East war have recently pushed Brent crude prices lower, and with that, we marginally boost our Czech growth outlook. With inflation remaining contained, no change to the policy setup is the most likely outcome

Households and firms still rock

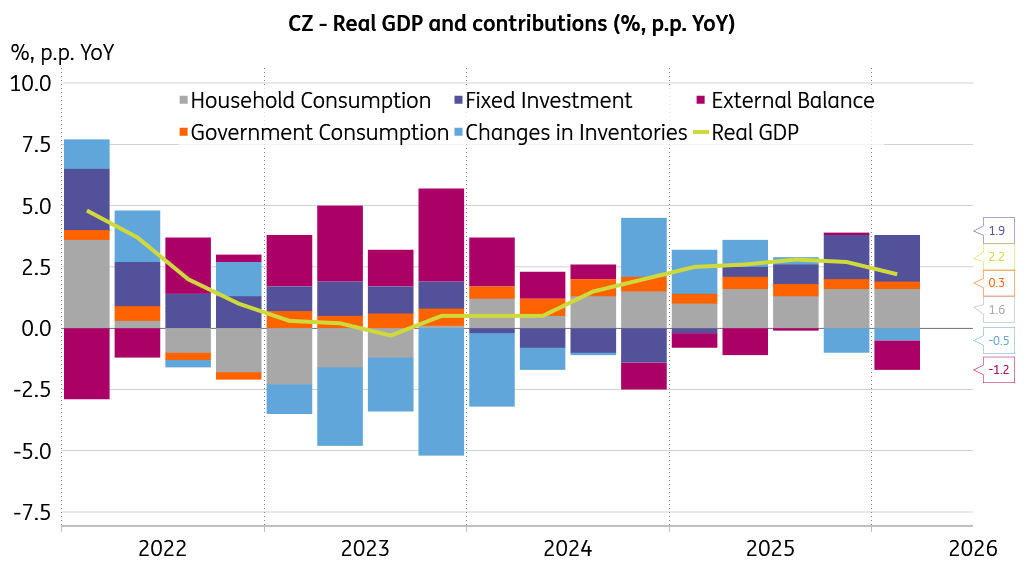

Czech real GDP gained 0.2% quarter-on-quarter and 2.2% year-on-year in the first quarter, according to the revised estimate. Regarding quarterly dynamics, the main growth factors were household consumption, fixed investment, and changes to inventories. Meanwhile, final government consumption and the foreign trade balance had a negative impact.

Domestic expenditure drives expansion

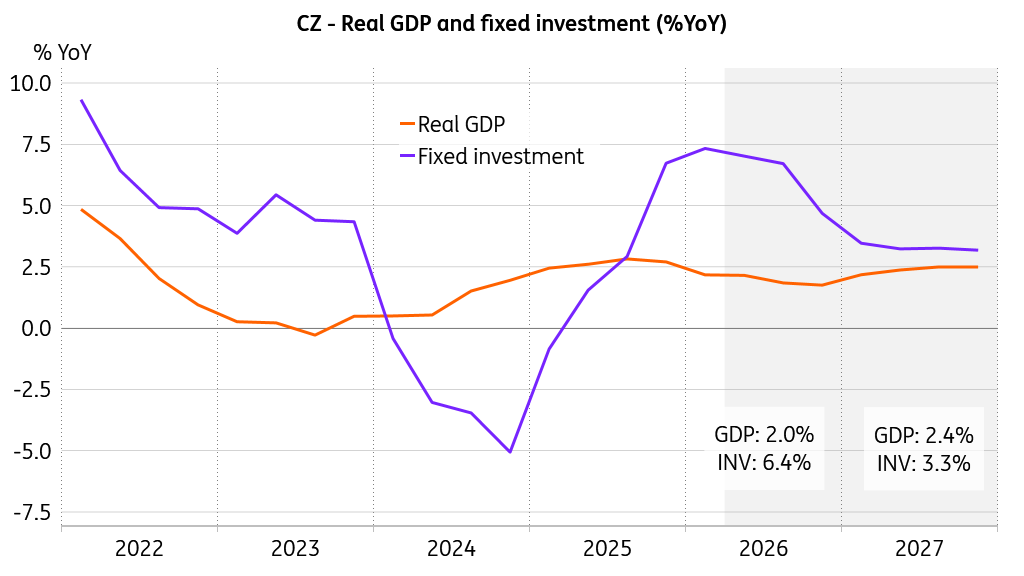

Fixed investment added 2.0% QoQ and 7.3% YoY, mainly via investment in buildings, infrastructure, and means of transport. Real exports gained 3.8% QoQ and 5.8% YoY, while imports grew by 5.8% QoQ and by 8.2% YoY. Still, imports were predominantly in the computers, electronics and optical devices segment, which may be linked to buoyant investment activity. External demand from European trading partners is still subdued, while the onset of the Middle Eastern conflict appears to have already weighed on export performance in the first quarter. The continued economic expansion was tangible in the labour market, as total employment gained 0.4% QoQ and 1.1% YoY in the first quarter. Total hours worked rose by 3.0% from the previous year, with wage volumes advancing by 8.9% YoY in 1Q26.

Fixed investment will drive growth potential

Should the ongoing negotiations between the US and Iran reduce the tension sustainably, delivering relief for global supply chains and energy prices, we would remain in a scenario where the Czech economy feels only limited damage. In such a case, the expansion of around 2% is still perfectly possible, depending mostly on the extent to which the health of the global economy has been hit, and how much pain is in the pipeline for the overseas demand for Czech exports.

De-escalation hopes are in the air

That said, the first quarter expenditure breakdown brought positive surprises to fixed investment, export and import dynamics as compared to our assumptions. We expect foreign trade to come under some pressure in 2Q26 due to the increased uncertainty, yet the investment momentum seems to be enjoying a degree of resiliency. With all that, and with hopes for some easing of the Middle Eastern conflict, we see Czech investments remaining on solid ground, which will lend support to potential and future growth.

Inflation likely not getting out of hand

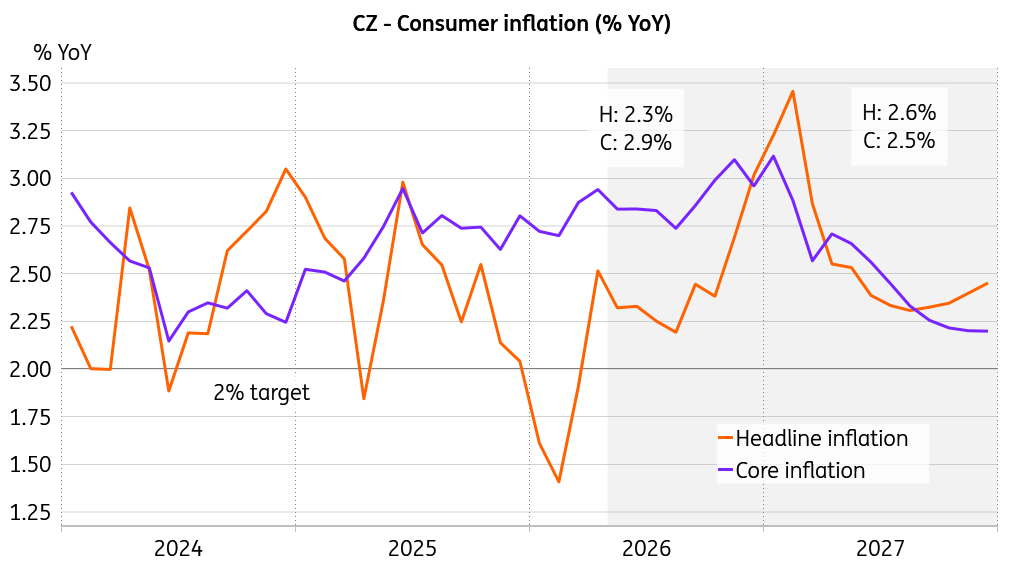

We have also incorporated the latest observations and course of events into our inflation forecast, and it seems that Czech inflation will not get out of hand, at least according to our best guess. Sure, both headline and core inflation are set to cross the 3% threshold of price stability, but when looking beyond 1Q27, this could be considered transitory.

Inflation surge can be deemed transitory

So, the still-decent economic expansion along with manageable inflation should allow the Czech National Bank to sail between the Scylla of rising price levels and the Charybdis of slowing economic growth without much pressure for an adjustment in rates. Indeed, an extensive and protracted global negative supply shock typically unleashes two major beasts. Well, who knows, maybe the end to the rough sailing is on the horizon, and the more painful scenario of forcing the economy to its knees through sharply higher policy rates may ultimately be avoided.

And that’s a very good thing, because businesses go bankrupt during a recession. Their market share could easily be taken by foreign competitors amidst the current unforgiving setup of a global village with ever-tightening foreign competition. And these days, when you lose it, it may be gone forever, as the classic lesson from Trainspotting tells us. Sending an economy into a downturn is not a trivial matter, as you can never be sure that it will recover at your command. With that in mind, we see base rate stability as the appropriate response to the current state of affairs.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more