Credit markets status quo confirmed after ECB meeting

- 23 July 2021

- Credit

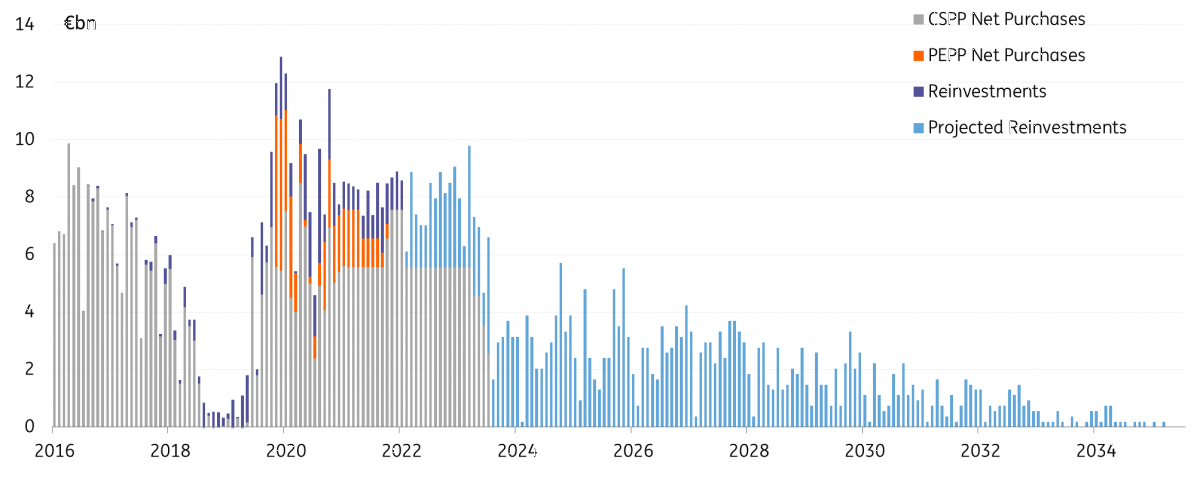

We are even more bullish after yesterday's ECB meeting, as tapering is pushed back, and PEPP will continue to be front-loaded. We show projections of CSPP, PEPP and reinvestments for the coming years, and in any case, we think the central bank will remain notably supportive of credit markets

We are conservatively bullish for credit for the coming year.

Indeed, we expect some weakness in the second half of the year on the back of rising rates, tapering discussions coming to the forefront, and a rise in swap spreads. However, any weakness and widening in credit spreads will be subdued by the significantly strong technical picture. Strong technical include the active ECB offering substantial support via CSPP and PEPP, a notable decrease in net supply and marginal but positive inflows into mutual funds (particularly ESG funds).

Unlike what was expected, the ECB meeting had very few in-depth changes. The report The ECB pours old wine from a barely new bottle, goes into more detail on this, but the main takeaways for a credit perspective are:

- The ECB made a shift towards more dovishness, which as a result means tapering discussions are unlikely for September,

- PEPP will continue to be front-loaded with faster purchases,

- PEPP reinvestments will continue until at least the end of 2023.

This is positive for credit, as the substantial support from PEPP will continue. In which corporate purchases amount to €2bn on average per month. This comes on top of the €5.5bn per month from CSPP net purchases.

Our economists are now expecting a rate hike in 1Q24, which means APP will likely run until the end of 2023 at an average pace of €5.5bn per month. From that point onwards, the ECB will still reinvest any maturing bonds, which we estimate to be around €2.5bn-€3bn per month. This will certainly keep credit markets supported for the coming years.

As we touched on in ECB projections for credit, one potential option for the central bank would be to smoothen the transition by increasing purchases under its Asset Purchase Programme. This could be as significant as €40-50bn per month, up from the current €20bn per month. While most of this will target public assets under the Public Sector Purchase Programme, we feel that the ever-popular Corporate Sector Purchase Programme will also benefit.

Indeed, we wouldn’t be surprised if the net result is zero; in other words, purchases of corporate credit could fully compensate for the end of the PEPP. The central bank has been buying €5.5bn of corporate bonds per month, on average, under its CSPP but could raise this to about €7bn per month. The CSPP runs at 25% of the APP, so even a slight decline would still mean a net rise.

Actuals & Projections of CSPP, PEPP and reinvestments

Monthly net purchases and reinvestments of CSPP and corporate purchases under PEPP, alongside reinvestments

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more