Countries hit most by the coronavirus value chain shock

Even before Covid-19 led to country-wide lockdowns, supply chain shocks and weak foreign demand were already taking a toll. Small open economies, such as Ireland, Luxembourg, and Vietnam now look to be the most vulnerable. In the G10, Canada is hurt most by the hit to foreign suppliers while Germany is hurt by reduced foreign demand

The economic damage that Covid-19 inflicts on a country is not only driven by the government policies to stop the spread and 'flatten the curve' but also by disrupted supply chains and the impact on individual companies. These disruptions started even before countries went into lockdown and will continue after they are over.

Imports

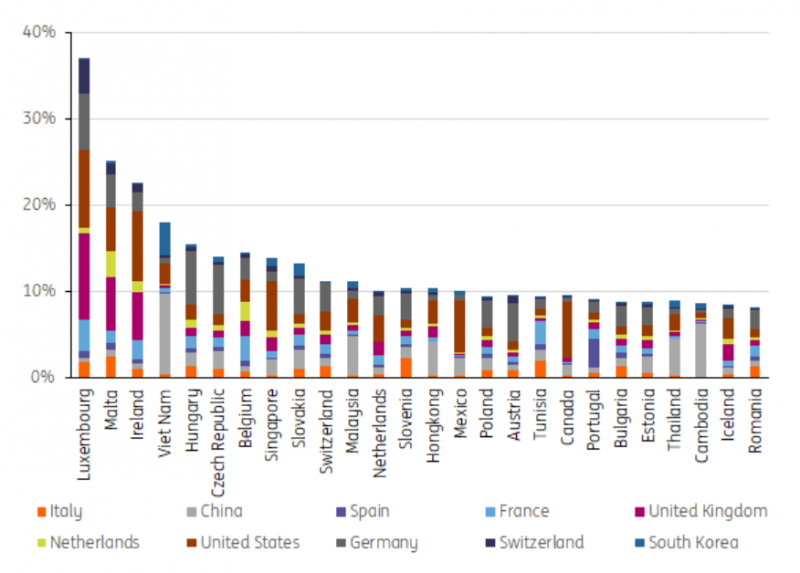

A shortage of intermediates (imported parts and materials to make products) by countries that were hit by the virus early on led to interruptions in the production process of other countries before the virus arrived. The damage will be larger, the more a country depends on the supply of intermediate goods from countries whose working population was hit hard by the virus. Chart 1 shows the dependency of countries on inputs from the top 10 countries with the highest absolute number of deaths due to the coronavirus. Since there are many countries where infections are measured incompletely, we use the number of deaths as an indicator for how much production is likely to have been shuttered in each country. We realise that this is not a completely accurate measure of production capacity that has been shut down. But more accurate indicators, like the utilisation rates for industries are lagging too much to provide useful information at this point in time.

Chart 1 shows that countries like Vietnam and Ireland are among the top five countries that have suffered most from falling production in countries with a lot of casualties. The difference between Asian countries like Vietnam, and European countries like Ireland, is that they have been hit at different moments in time. The coronavirus crisis started in China so Vietnam and other Asian countries that are very dependent on Chinese inputs, like Singapore, Hong Kong, Malaysia, Thailand and Cambodia (see chart), were first to be hit through this value chain effect.

Chart 1: Top 25 countries most dependent on inputs from top 10 countries most hit by COVID19 (#deaths)

Now that the virus has spread to Europe and is increasing in the US, the chart shows that countries like Luxembourg, Ireland, Hungary, the Czech Republic and Belgium are suffering through the input side of their value chains. Currently, 10 out of the 15 countries that are most exposed to shortages of supplies are European.

The US is a relatively closed economy and therefore less hit by the lack of supply of foreign intermediate goods, but the economic fallout in the US due to the quick spread of the disease, generates significant problems for Canada, which is heavily dependent on supplies from the US (see chart 1).

The connectivity of an economy to countries with the most deaths is especially important if the latter are important suppliers of intermediate products to world markets. Chart 2 shows the 10 largest suppliers of world markets. The chart shows that eight out of the 10 largest suppliers of world markets are also in the top 10 countries that have been hit most by the virus (chart 1). By both measures, Luxembourg, Malta, Ireland, Vietnam, Singapore, the Czech Republic, Hungary and Slovakia are in the top 10 countries most affected by interruptions in the supply of intermediates of countries hit most by the virus. Of the 10 largest economies in the world, Canada stands out again as most vulnerable.

Chart 2: Dependency on inputs of 10 largest suppliers of world markets

Exports

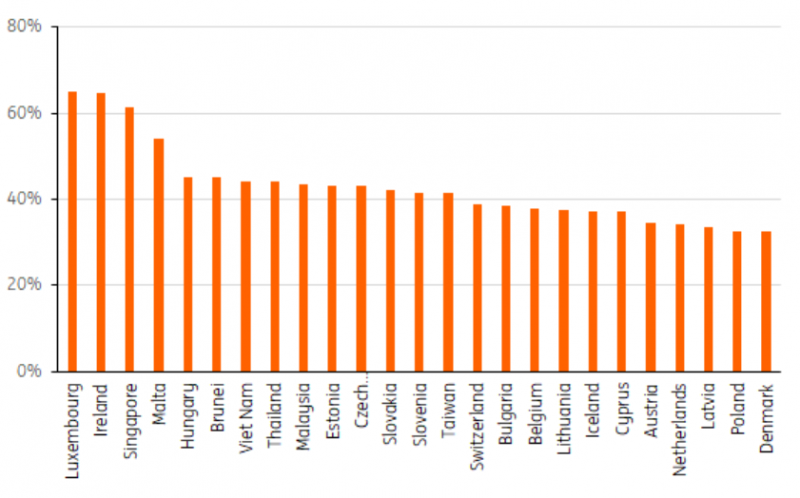

Open economies are not only seriously affected by the virus through their imports of intermediates, but also through their export channels. Even after the virus has been brought under control domestically, an open economy will continue to suffer from the virus because of falling demand in countries that are still struggling with the crisis. Figure 3 shows which countries are most dependent on exports.

Chart 3: Dependency on foreign final demand

Value added of exports as % of total value added in a country*

*Total value added in a country is a proxy of GDP, but it ignores taxes, subsidies, etc

Assuming that the virus supresses spending around the world, countries that rely on exports will be the most heavily affected. Countries that export only a small portion of production (like the US, India and Brazil) will suffer less than countries that are very dependent on foreign demand (like Ireland, Hungary, Singapore and Vietnam). Chart 3 shows that Luxembourg, Malta and Ireland are most dependent on foreign demand, mostly driven by the services sector. For Vietnam and Hungary, the manufacturing industry is hit most by falling external demand. Of the top 10 largest economies in the world, Germany is most affected through this (export) channel of the value chain, followed by Canada.

The recovery phase

Foreign demand is made up of demand from many countries. Those countries that export many goods and services to countries whose demand has been hit a lot and for a longer period of time, will suffer the most damage from the demand (read: export) side of their value chain.

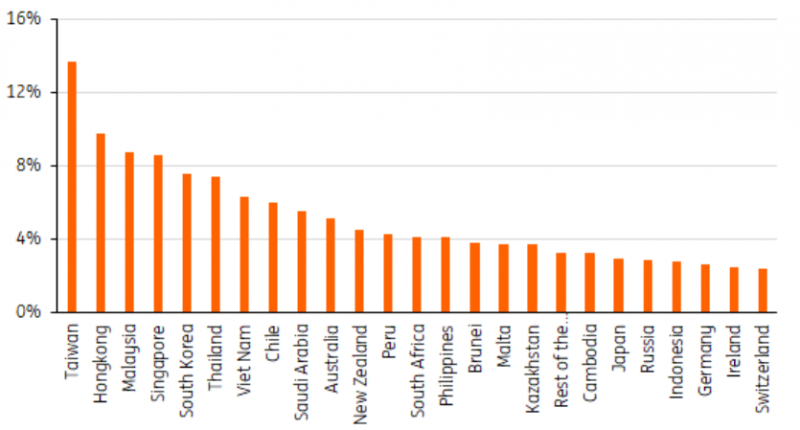

So, to gauge the damage for individual countries through the export channel, it's important to know where the exports are going and at what stage of the recovery those countries are in. Take for example demand from China. We expect that Chinese demand will be one of the first countries to recover because China is ahead of most other countries in containing the virus. This will offer some relief for those countries that are relatively dependent on demand from China.

Chart 4: Countries most dependent on Chinese final demand

Value-added dependent on Chinese final demand as % of total value-added.

Due to their proximity, Asian countries are very dependent on final demand from China and benefit most from the recovery there. Of the non-Asian countries, some commodity exporters such as Saudi Arabia for oil and Chile for metals, are among the largest beneficiaries as well. In Europe, Malta, Germany, Ireland and Switzerland are most dependent on final demand from China.

Conclusion

Countries that use a lot of inputs from other countries hit by the virus early on, suffer from their openness on the input side of the economy as the virus disrupts the supply of intermediate goods that they need for their own production. Countries that produce a lot of exports suffer on the output side, as the virus supresses spending.

Taking these two channels together, the above data shows that open economies are hurt much more through global value chains than less open economies. Open economies will suffer for a longer period of time from the supply and demand effects of the coronavirus. Luxembourg, Ireland, Singapore and Vietnam are among the most vulnerable countries.

Of the world's 10 largest economies, Canada suffers most from the fallout of foreign supplies and Germany suffers most from weaker foreign demand.

The above analysis does not mean that closed economies are better off in this crisis. Whether a country is better off depends to a large extent on the question of how much its production capacity is hit by the virus.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

2 April 2020

Covid-19: A virus-driven ice age This bundle contains 10 Articles