Consumers still fear rising grocery bills, but there’s relief in sight

- 2 February 2026

- Commodities, Food & Agri

Rising food prices remain a key concern for EU consumers. The latest ING Consumer Survey shows that they even expect grocery prices to rise more rapidly in 2026. However, we see signals that price pressure is easing. That’s good news for households, but also for food makers and retailers who’ve been coping with lagging demand and sluggish sales growth

Why increases in food prices are expected to ease in 2026

EU consumers have faced extraordinary price increases on supermarket shelves since 2022, a key factor eroding real wages. The good news is that real wage growth has been turning the corner and is likely to improve at a modest pace in 2026. What helps here is that ECB projections indicate that food inflation will drop from 2.8% in 2025 towards 2.4% in 2026.

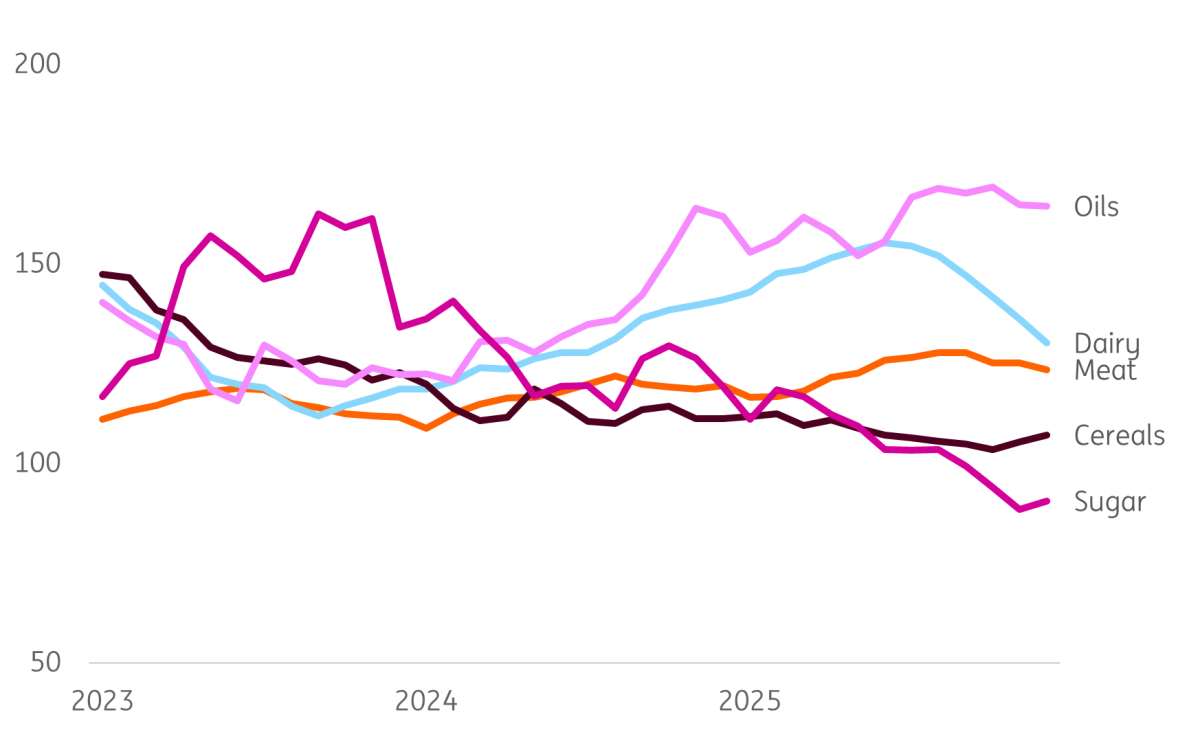

A gradual pass-through of lower market prices for various agricultural commodities such as sugar, dairy and cocoa is a key reason behind the slowdown in food inflation. On top of that, we anticipate lower energy prices, which also helps to keep a lid on price increases along the supply chain. Still, increases in wage costs at food manufacturers, distributors and retailers remain a key reason for inflation to persist. Typically, labour costs account for 10-15% of total costs in food manufacturing.

So, prices of groceries will still go up in 2026. But some products, including staples like milk, butter, sugar and potatoes, are getting a bit cheaper. In these categories, we could see more price reductions on shelves this year. For fruit and vegetables, the recent price trend is also favourable for consumers. Whether that will continue will be largely determined by the weather and growth conditions.

Strong decrease in global dairy and sugar prices

Index 2014-2016 = 100, monthly data up until December 2025

EU countries show great variety in inflation and spending on food

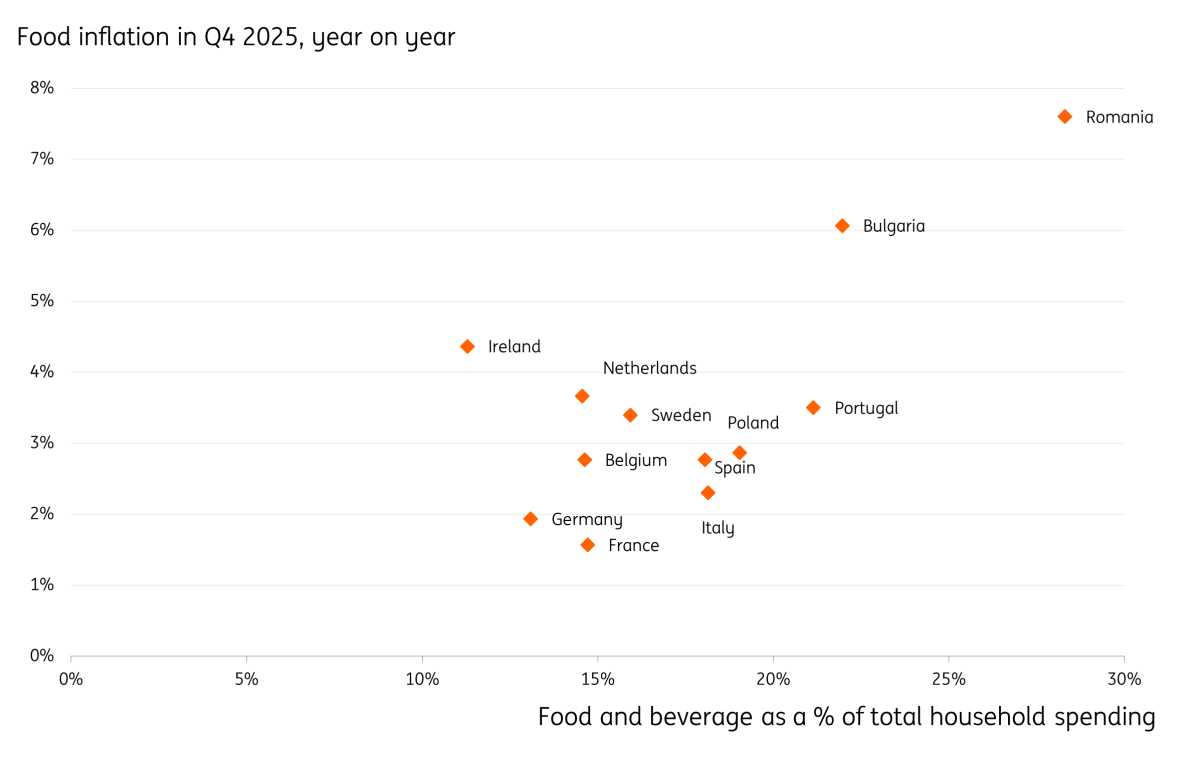

While the ECB projection is reassuring, food companies should keep in mind that inflation levels still vary quite a bit within the EU. Countries like France, Germany and Italy are on the low-end of the spectrum, with price increases between +1.5 to +2.3% in Q4 2025. Romania, Bulgaria and the Baltics are on the other end of the spectrum with increases ranging from +5.0 to +7.5%. Figures for food inflation in Romania are pushed up by a broader VAT increase introduced in August 2025.

On average, Europeans spend almost 16% of their total budget on food and non-alcoholic beverages in retail. This share is higher in Eastern and Southern European countries. Combining inflation and expenditure data shows that households in Romania and Bulgaria are currently much more impacted by rising food prices.

Romania and Bulgaria combine high food inflation with a larger share of household budgets spent on food

European consumers and food inflation: seeing is believing

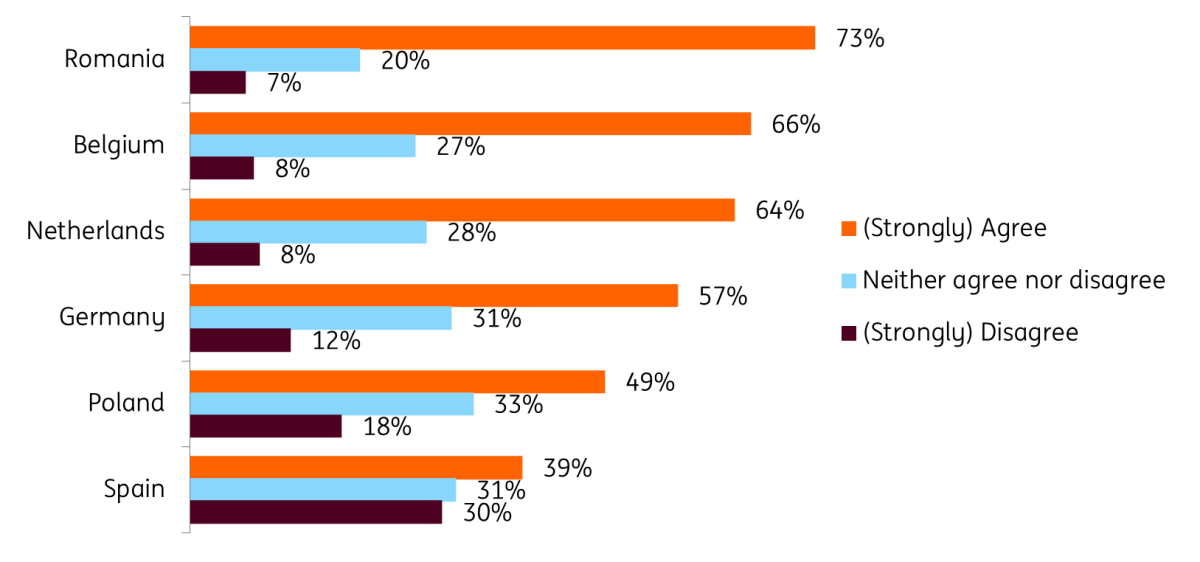

So what about consumers? What are their expectations? They are not reassured yet about a moderation in food inflation. On the contrary, most of the respondents in the latest ING Research Consumer Survey expect grocery prices to rise more rapidly in 2026 compared to last year. This is especially true for Romania (73%), Belgium (66%) and the Netherlands (64%).

Only 14% of respondents across the six countries in our survey expect a slowdown. It’s a sign that many consumers are mentally prepared (or preparing) for even higher inflation. The lessons we take from it: high food inflation still weighs on consumers’ expectations, and consumers need to see that inflation moderates before they believe it.

Many European consumers expect a more rapid increase in grocery prices in 2026

Statement: I expect the price level of groceries in my country to increase more rapidly over the next 12 months

Consumer sentiment on purchasing power is still not great

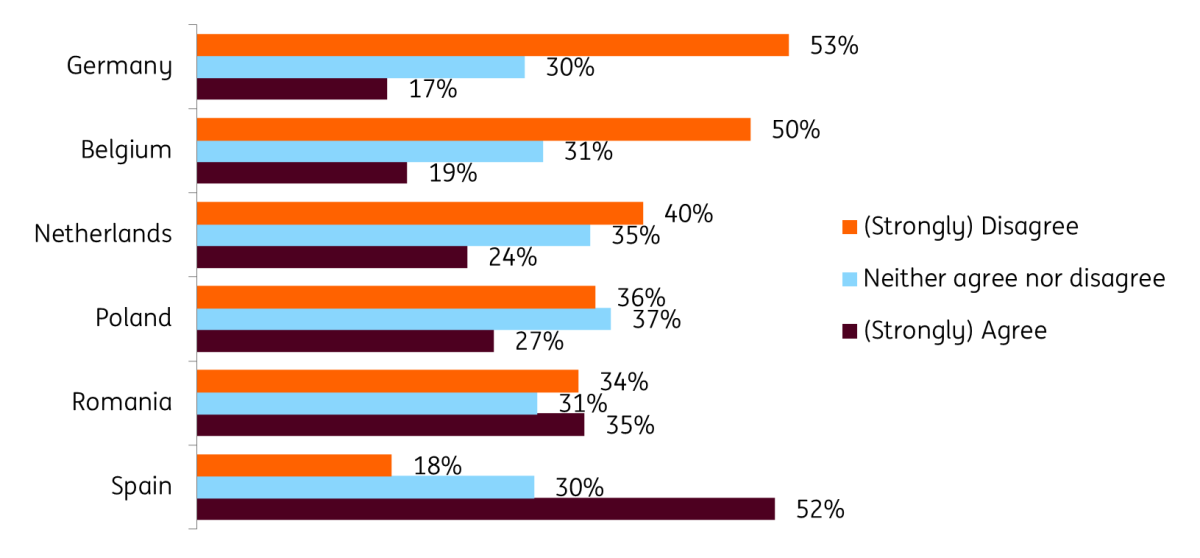

Even with real wages largely recovered, consumers remain downbeat about their purchasing power heading into 2026. Half of all respondents in Germany and Belgium, for instance, don’t expect an improvement in purchasing power. Spanish consumers are much more upbeat, which is likely influenced by the relatively strong improvement in real wages over the past few years.

Purchasing power expectations vary considerably across Europe

Statement: I expect my purchasing power in 2026 to increase compared to this year

Manufacturers struggle with lack of demand

Lack of demand is the key concern for food and beverage manufacturers. According to EU industry surveys, that’s especially true for France, the Netherlands and Belgium. EU products have become less competitive outside the bloc due to a stronger euro and US and Chinese import tariffs on food products. Within the EU, the fear of continued price increases on shelves could help explain why demand disappoints, as it prevents consumers from trading up by either buying more or higher-quality products. Sales volumes in EU food retail have only improved a little since mid-2024.

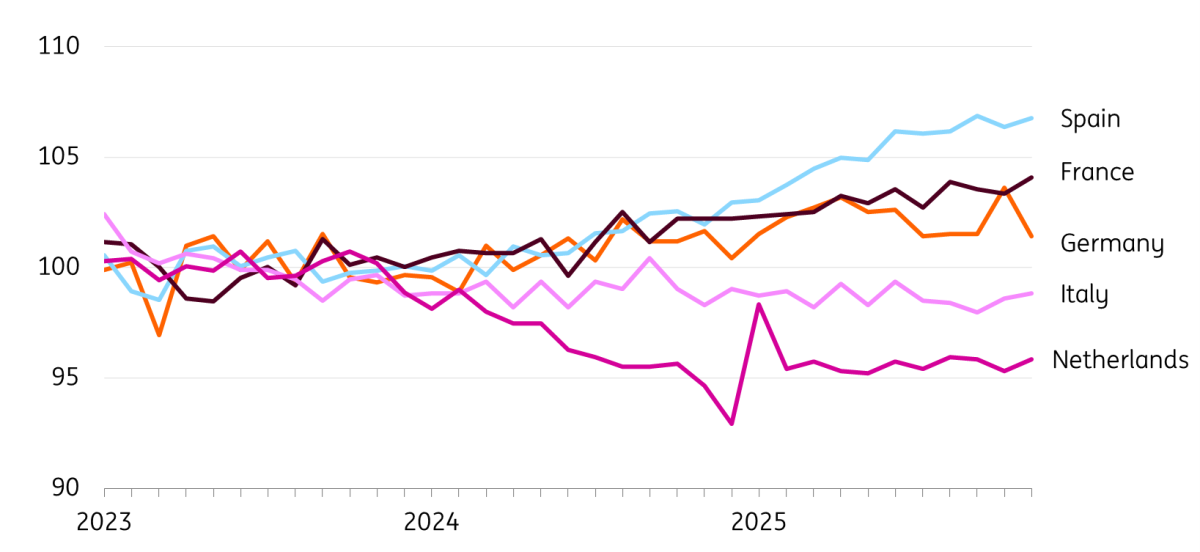

At a country level, Spanish retailers are doing better than their counterparts in other large member states due to stronger domestic spending and an increasing number of tourists. Italy and the Netherlands are doing worse, although Dutch figures for 2024 and 2025 are distorted by a tobacco sales ban in supermarkets. In Dutch food retail, ING debit card transaction data shows that discount supermarkets gained market share in 2025, which is a clear sign that many consumers are still very cost-conscious.

Meanwhile, sales volumes in restaurants and cafés are stagnant at the EU level. Poland is an exception. Among the large EU economies, France is performing better than the average and restaurants and cafés in Germany are doing worse with a continuous drop in sales volumes since early 2024.

Divergence in sales volume growth in food retail: Spain leads and Italy and the Netherlands lag

Index 2023 = 100, monthly data

Economics for food companies look more favourable, but beware of cautious consumers

With food inflation slowing and modest growth in real wages, the outlook for sales volumes of food companies in the EU becomes more positive. Still, we expect marginal gains in sales volumes rather than big improvements.

European consumers tend to be more sceptical than economists about future prices and purchasing power, and recent price hikes for products like beef, coffee and chocolate still resonate in their shopping behaviour. For food companies, it’s good to keep both perspectives in mind when executing strategic plans for 2026.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more