Cocoa prices under pressure amid supply glut

- 8 December 2025

- Commodities, Food & Agri

Cocoa has been one of the worst-performing commodities this year on the back of easing supply concerns. The market is set for another surplus in 2025/26, which should see stocks continue to recover and put further downward pressure on prices

Tightness concerns ease with surplus expectations

Cocoa prices have collapsed this year as better supply prospects and weaker demand have seen the market return to surplus in the 2024/25 season, while it is also expected that the global market will see another surplus in the 2025/26 marketing year. This has seen London cocoa fall almost 60% this year; however, prices remain well above pre-2023 levels. London cocoa averaged GBP4,121/tonne in November 2025 vs. an average of GBP1,749/tonne between 2018-22.

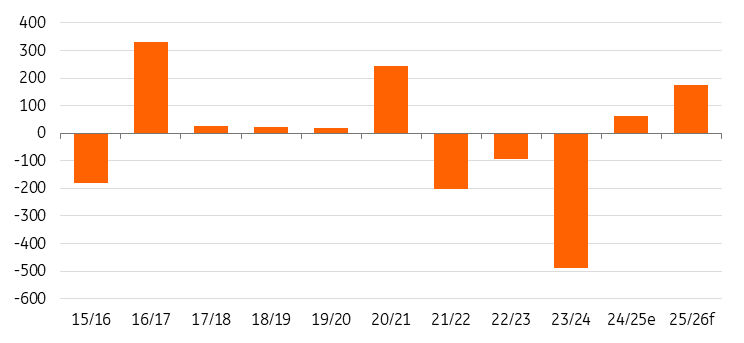

The 2024/25 season finished with a surplus of around 60k tonnes, which would be the first surplus since the 2020/21 marketing year. However, the size of the expected surplus shrank as the marketing year progressed, with West African production coming in lower than initially expected.

Meanwhile, for the 2025/26 season, we are forecasting another surplus of around 175kt. This increase is driven by expectations of stronger output from South America, particularly Ecuador, while Ghana is expected to see some recovery in output. For top producer Ivory Coast, we expect output to remain largely stable.

Demand has also played an important role in shifting the market back to surplus. Higher prices weighed on demand last season, while for 2025/26, demand is likely to still feel the effects of higher prices, even though prices have sold off aggressively through 2025.

A surplus environment should see prices continuing to move lower in 2026, while a rebuilding of global inventories should also help to reduce some of the extreme volatility we have seen in the cocoa market in recent years. We forecast that London cocoa will average a little more than GBP3,400/tonne, down significantly from 2024 and 2025 levels, but still well above historical averages.

In addition, the EU is on track to delay its deforestation regulation (EUDR) by yet another year, which will only add downward pressure to prices, with it delaying some supply concerns for the EU. The EUDR was originally set to come into force at the end of 2024, but was delayed for a year in order to give companies time to meet compliance obligations. And the latest delay will push implementation to the end of 2026.

Cocoa market set for a larger surplus in 2025/26 (k tonnes)

Stronger supply in 2025/26

Better yields and an expansion in plantations are expected to drive an increase in Ecuador’s cocoa production. Ecuador is the third-largest producer and is on track to take the number two spot from Ghana in the coming years. For the 2025/26 season, Ecuador is expected to produce 580k tonnes, up around 4% YoY, continuing its upward trend in output. The higher price environment also means that farmers can invest in more efficient farming practices, and with farmers in Ecuador receiving a larger share of global prices, relative to the Ivory Coast and Ghana, they can invest relatively more back into their plantations. According to the Ecuadorian Association of Cocoa Exporters, farmers in Ecuador receive around 90% of the global price vs. 70% for farmers in Ghana.

For top producer Ivory Coast, we are forecasting that output will remain relatively stable at around 1.8m tonnes for the 2025/26 season. Good weather should be supportive for the crop, although cocoa arrivals at Ivorian ports are lagging behind last season due to a slow start. These arrivals will be watched closely in the months ahead, shedding more light on how the crop is evolving. Clearly, a small change in output from the Ivory Coast could swing the global balance quite significantly.

For Ghana, initial government projections are looking at output totalling around 650k tonnes in 2025/26. However, we expect more moderate growth with output of our 600k tonnes for the season.

The bigger issue with West Africa, and specifically the Ivory Coast and Ghana, has been the impact of ageing trees and swollen shoot disease on production. These are structural issues which are not going to be fixed quickly, and therefore we will need to see prices remaining above their historic norms in order to ensure we see adequate investment in supply in the medium to long term.

Demand still under pressure

The high price environment that we have seen has helped to try to balance the cocoa market through demand destruction. This is needed, given that it takes several years for supply to respond to prices, with the time between planting cocoa trees and the first harvest anywhere from three to five years.

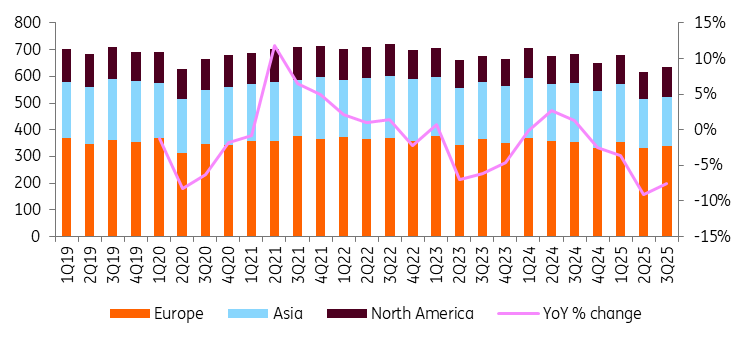

Regional grindings have been under pressure for much of this year. Combined grindings in Europe, North America and Asia are down 6.7% over the first three quarters of 2025, with the bulk of this weakness coming from Asia and Europe.

Looking to 2026, and while prices have come off from their highs, it takes time to work through the supply chain, while prices are still high on a historical basis. Therefore, we are assuming that demand will be largely flat through the 2025/26 marketing year, but certainly risks are skewed to the downside.

Cocoa grindings under pressure (k tonnes)

Speculators turn increasingly bearish towards cocoa

It is no surprise that, with improved supply prospects and an increasingly looser supply/demand balance, speculators have lost interest in the cocoa market, and in fact have become increasingly bearish towards the market.

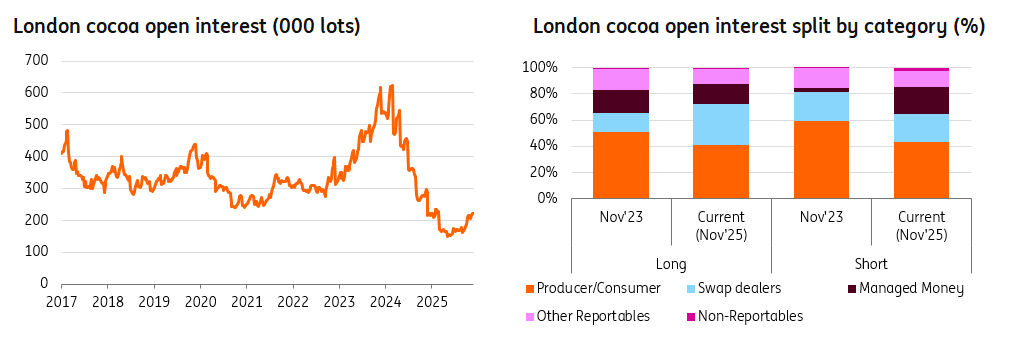

Over the course of the year, speculators have shifted from a net long to holding a net short in the London cocoa market. In fact, speculators have been the most bearish towards the market since August 2021.

The selling in the market has been driven largely by fresh shorts entering the market. While the outlook remains bearish, this large short in the market does pose some positioning risk, if any bullish catalysts were to arise, as it would likely force shorts to run in and cover their position. The managed money short makes up around 26% of total open interest, the highest proportion since 2018. While a growing gross short has played a role in this, aggregate open interest in London cocoa remains well below historic norms. This lower open interest is largely driven by both commercial longs and shorts.

From a consumer point of view, there is reluctance to hedge at the higher prices we have seen in recent years, while from the producer side, uncertainty over the supply outlook and the risk of higher prices would also leave players hesitant to hedge. A producer hedging into a strengthening market leaves them facing larger margin calls on their short futures position.

Having lower commercial participation in the futures market and larger participation of speculators in the market does leave it more volatile.

Speculators build short in London cocoa as open interest remains under pressure

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Commodities Outlook 2026: Energy cools as metals heat up

- This bundle contains 17 Articles