China still focused on its zero-Covid strategy

- 31 March 2022

- China

China's central bank failed to lower interest rates after strong economic data in the first two months of the year. We keep our call for a targeted RRR cut to help smaller businesses hit by Covid. Two big cities have been locked down and that was enough for the yuan to temporarily lose its safe-haven status

Strong data means no interest rate cut

China’s central bank, the PBoC, did not cut interest rates in March, a decision we believe was taken after surprisingly strong economic data that was coming through. But this does not mean the PBoC will not ease again. Several top officials have already suggested that the economy needs a further loosening of monetary policy. It is likely that the PBoC could ease via cuts in the Reserve Requirement Ratio (RRR).

Targeted RRR for inclusive finance is still likely

But this time, any RRR cut may not be so broad-based. That sort of easing would provide a general surge in liquidity for any potential borrower or debtor in the economy, including the high debt-ratio real estate developers that the government would like to avoid boosting. With such limitations in mind, we believe that the coming RRR cut will be a targeted one, similar to those which specified that they'd apply only to 'inclusive finance'. That covers finance for rural and agricultural purposes and small to medium enterprises, SMEs.

It could happen quite soon as many businesses continue to be affected by more Covid-induced lockdowns and social distancing measures. We expect a 50 basis point cut from 8.4% to 7.9%. The lower bound of the PBoC’s RRR is 5%.

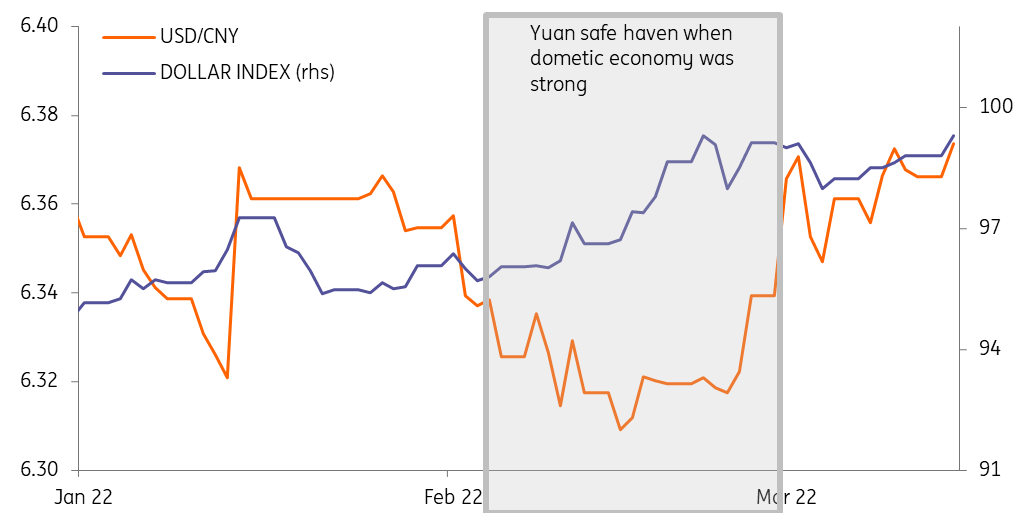

Divergence of yuan and dollar shows its safe-haven nature

Yuan is a safe haven currency when there is no Covid

On the yuan, the safe-haven nature of China’s currency has held up when there has been no negative domestic news. But when this latest wave of Covid in Shenzhen and Shanghai resulted in semi to full lockdowns, the yuan appreciated against the dollar even though the conflict between Russia and Ukraine continues.

Another test for the zero-Covid strategy

Covid in Shenzhen is now almost cleared, and we expect Shanghai to return to near zero-Covid cases in around a week. Between now and then the financial sector will continue to work from home, and big factories will continue to operate with 'closed-loop' operations. If all goes to plan, the negative impacts from this round of lockdowns should not be as big as those we've seen previously.

This is another test for China’s lockdown and zero-Covid strategy; it's called 'dynamic clearing' in China. We expect the yuan to once again adopt safe-haven characteristics when this latest virus surge is cleared. Our forecast for USD/CNY is 6.35 by the first half of the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: There’s nothing normal about the global economy

- This bundle contains 17 Articles