Our view on central banks in 2024

Why the major central banks are likely to start cutting from the second quarter of next year

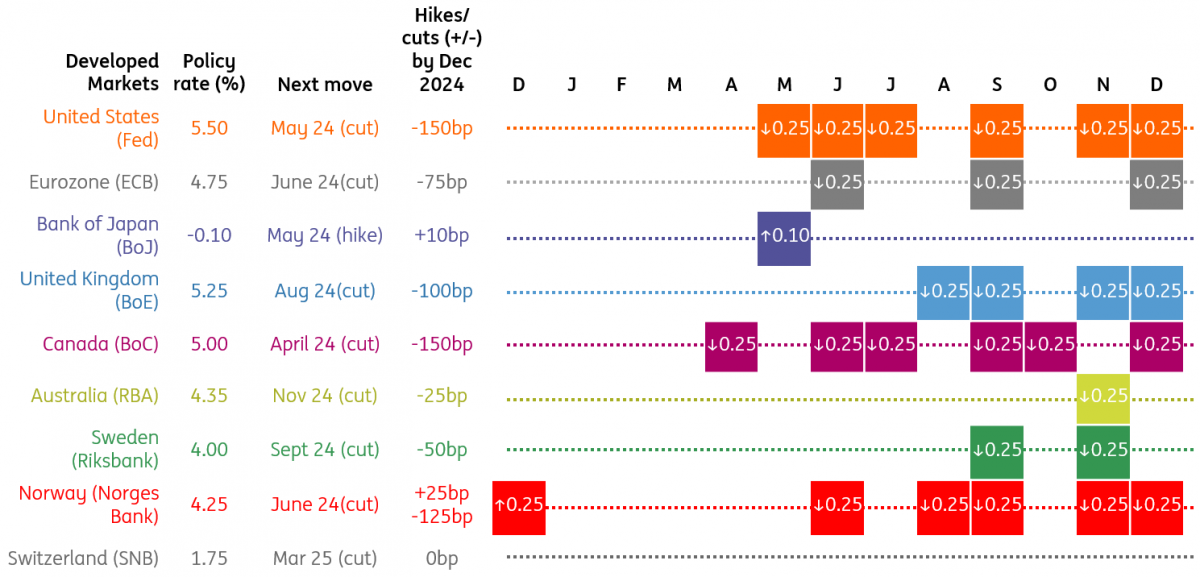

Federal Reserve

The US economy continues to perform well and the jobs market remains tight, but there is growing evidence that the Federal Reserve’s interest rate increases and the associated tightening of credit conditions are starting to have the desired effect. Recent inflation prints look much better behaved and leading economic indicators are weakening, while hiring and hiring intentions appear to be cooling. Significantly, Fed officials are broadly acknowledging that monetary policy is restrictive. We think rates have peaked, and the next move will be a cut.

The consumer is key, and with real household disposable incomes flatlining, credit demand falling, and pandemic-era accrued savings being exhausted for many, we now see a real risk of a recession. Collapsing housing transactions and plunging homebuilder sentiment suggest residential investment will weaken, while softer durable goods orders point to a downturn in capital expenditure. If low gasoline prices are maintained, inflation could be at the 2% target in the second quarter of next year, which could open the door to lower interest rates from the Federal Reserve from May onwards – especially if hiring slows as we expect. We look for 150bp of rate cuts in 2024, with a further 100bp in early 2025.

European Central Bank

As much as the European Central Bank (ECB) had underestimated the strength and pace of surging inflation in 2021 and 2022, it could now be underestimating the pace of disinflation. Headline inflation has already come down back to around 3%, wage growth should plateau in the first months of 2024 and the full impact of the ECB’s monetary tightening this year will continue to unfold in 2024. Disinflation in 2023 was mainly the result of energy and fiscal policy base effects. The disinflation of 2024, on the other hand, is likely to be the result of ECB tightening over the last two years.

While the ECB still banks on a rebound of private consumption next year, we rather see precautionary savings. Disinflation and weaker-than-expected growth will be sufficient for the central bank to take its foot off the monetary policy brakes somewhat, cutting rates by a total of 75bp every quarter starting in June. The first rate cut should coincide with the decision to gradually stop reinvestments of purchases assets under its Pandemic Emergency Purchase Programme (PEPP).

Bank of England

The Bank of England's tightening cycle has almost certainly finished, and policymakers are putting a lot of energy into convincing investors that rate cuts are some way off. That said, they haven’t ruled out easing in 2024, and we think the door is wide open to rate cuts by summer. The impact of rate hikes will continue to build as 4-5% of mortgage holders refinance each quarter and in most cases, off five-year fixes that had much lower rates. Services inflation and private sector wage growth, which – by the Bank’s own admission – are key next year, should both be back to the 4% area next summer (from 6.6% and 7.8% respectively now). Against that backdrop, we think we’ll get 100bp of cuts in 2024 and the same amount of easing in 2025. Markets are increasingly thinking this way too.

Bank of Japan

2024 will be the first year of the Bank of Japan's policy normalisation, ending decades of ultra-easing policy. We expect solid wage growth to support the BoJ’s long-awaited sustainable 2% inflation target and tight labour conditions to support private consumption. Investment in new technologies will also grow further, benefitting from government subsidies and the global supply chain reshuffling trend. Given the strong corporate earnings in 2023, we believe that next year’s wage growth should hit more than 3%.

The BoJ’s first step toward normalisation will be scrapping its yield curve control program, which is likely to happen in the first quarter of 2024 when JGBs trend down to a sub-1% level, following the UST market. Soon after the BoJ confirms the results of the spring salary negotiations, the central bank will likely take a 10bp hike in the second quarter but hold its short-term policy rate at 0.0% until the end of the year.

Developed market central banks in 2024

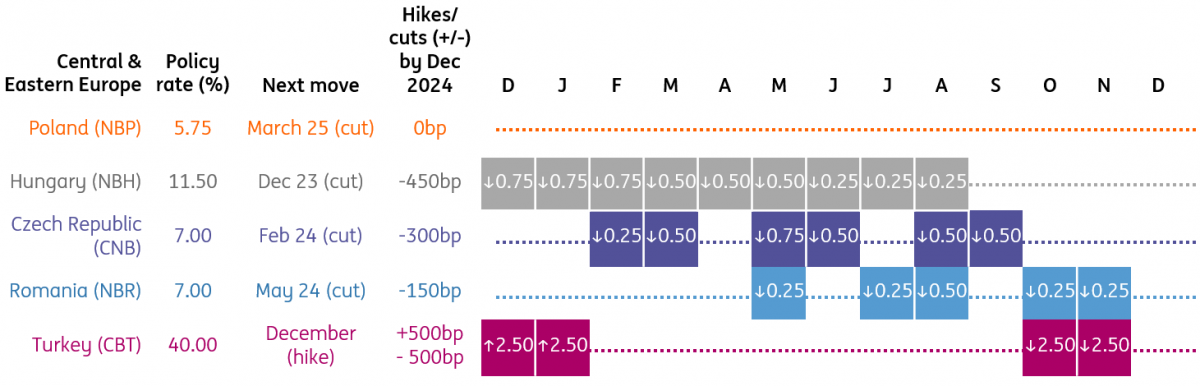

Central and Eastern Europe central banks in 2024

Asian central banks in 2024

Download

Download article

30 November 2023

ING Global Outlook 2024: No magic spell for a brighter world This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more