Asia week ahead: RBA policy meeting plus regional trade data

- 27 April 2023

- Asia week ahead Australia China

Next week we'll get China activity data and regional inflation reports, plus a Reserve Bank of Australia meeting

Upcoming RBA policy meeting

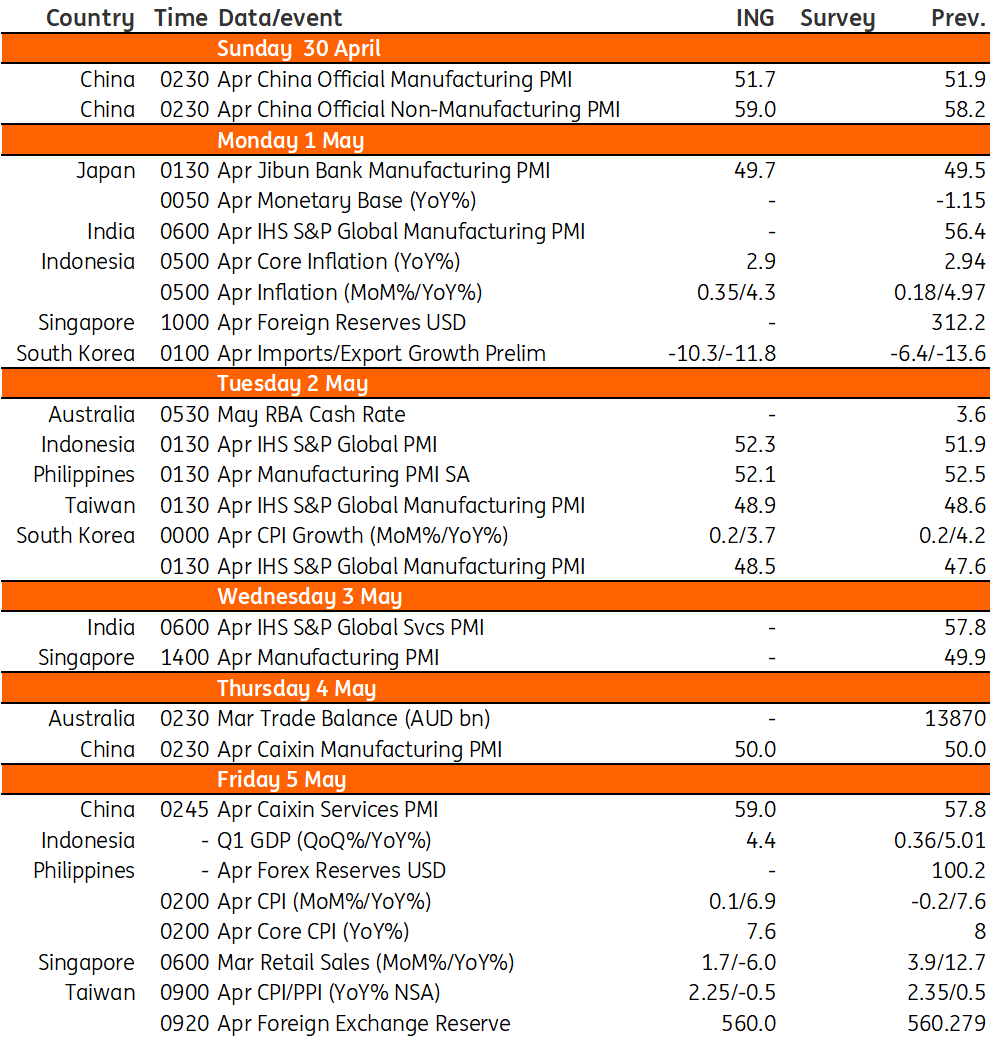

After pausing at its April meeting to gather more information and assess the impact of its tightening so far, the main point of note for the Reserve Bank of Australia (RBA) will have been the much lower inflation numbers in March than in February. Year-on-year inflation in March dropped from 6.8% to 6.3%, while the slower-moving quarterly series for the first quarter fell from 7.8% to 7.0%. Core inflation rates also fell or came in below expectations. These figures not only point to an extension of the pause but could also be viewed as raising the likelihood that 3.6% marked the peak in the cycle for cash rates.

We would also not rule out there being some easing of rates before the end of this year, as by then we believe inflation will have fallen to a level that is only just above the upper bound of the RBA’s 2-3% inflation target.

Trade figures and inflation from Korea

Korea’s exports are expected to continue to decline in April and the downturn in exports will become widespread except for automobiles.

Meanwhile, falling commodity prices and base effects should push down headline inflation.

PMI data from China

China will release its official PMIs on 30 April. We expect slightly slower monthly growth in the manufacturing PMI to 51.7 in April from 51.9 in March. The slight dip can be traced to slower export orders from the US and Europe. The non-manufacturing PMI should continue to improve to 59.0 in the month from 58.2 in March as real estate activities grew while retail sales have been fairly stable ahead of the Golden Week public holiday from 29 April to 3 May.

A similar trend should be recorded in Caixin’s manufacturing PMI and services PMI to be released on 4 and 5 May, respectively.

Taiwan reports price data and economic activity figures

Taiwan’s manufacturing PMI should continue to show a monthly contraction. The latest figure is expected to dip to 48.9 from 48.6. The slower deterioration can be attributed to a slight pickup in orders for new phone models.

Meanwhile, falling industrial production likely put deflationary pressure on wholesale items more than on retail items. This will likely be the trend for Taiwan in the near term. Thus, we expect CPI inflation to moderate to 2.25% in April from 2.35% in March while PPI should start to record a yearly contraction of 0.5% in April from a positive 0.5%YoY a month ago.

Inflation moderating somewhat in Indonesia and the Philippines

Price pressures have been moderating in Indonesia and the Philippines with base effects also helping to push headline inflation lower. Indonesia’s headline inflation could head closer back to the central bank’s target and settle at 4.3%YoY while core inflation could be steady at 2.9%.

Meanwhile, headline inflation in the Philippines is also on the decline and we expect April inflation to dip to 6.9%YoY from 7.6% in the previous month. A slower inflation reading in the Philippines could open the door for the Bangko Sentral ng Pilipinas (BSP) to consider a pause at its May policy meeting.

Indonesia's first quarter GDP report

Indonesia will release first quarter GDP data next week and forecast growth to settle at 4.4%YoY driven by solid household consumption topped off by a relatively strong export performance. PMI manufacturing remained in expansion mode for the first few months while retail sales managed to stabilise after a brief contraction in January with inflation easing.

Singapore retail sales

Retail sales could revert to contraction, down by as much as 6%YoY given still elevated inflation and slowing growth momentum. Singapore recently reported disappointing first-quarter GDP numbers and retail sales likely reflected the downturn in growth.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles