Asia week ahead: China’s growth momentum to pick up despite sluggish exports

- 6 April 2023

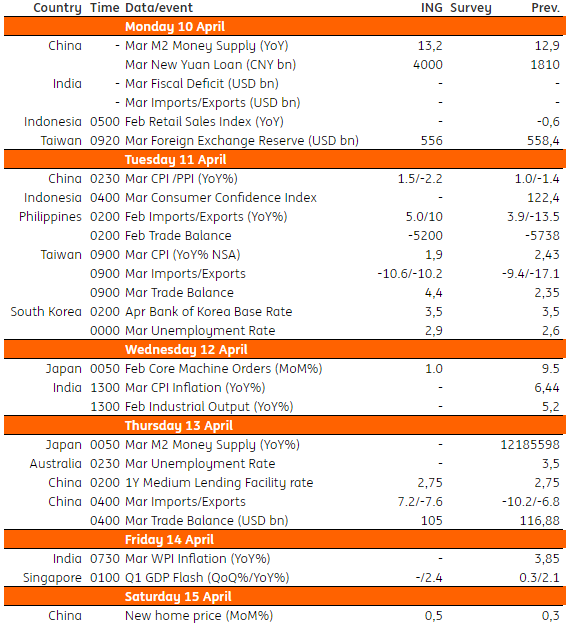

Next week’s data calendar features China's loan data, inflation and trade from China and Taiwan, Singapore GDP, and the Bank of Korea's policy rate decision

China's loan growth will continue while exports is expected to contract

China will announce loan data next week, which should be market-moving. We expect the new yuan loan could increase to CNY4000 billion in March compared to CNY1810 billion in February. This is hinted at by the PBoC RRR cut and a significant amount of liquidity injection in the last two weeks of March. Loan growth in the second quarter should be a lot smaller unless the economy needs extra support.

Inflation in China and Taiwan should be mild. This should be a backdrop for starting to pause policy rate hikes for Taiwan. But the worry of a bigger interest rate differential with the US should continue to be the key factor for the central bank to consider one more hike in the second quarter.

China and Taiwan will release international trade data. Both should show continuous yearly contraction in exports, especially in electronic exports. China's imports should keep their strength from the recovery of domestic demand.

Singapore growth to moderate in 1Q23

Singapore GDP will likely moderate to expand 2.4% YoY, up from the 2.1% posted in the last quarter but much slower than the 4.0% gain recorded in 1Q22. The economy is facing several challenges, namely high domestic inflation and slowing global demand. Both exports and industrial output reported contractions for the quarter, while retail sales were soft.

Bank of Korea watch : Wait and see approach

The Bank of Korea will meet next Tuesday and no action is expected as inflation is slowing while underlying growth conditions remained weak. The uncertainty surrounding the recent oil price pick-up will strengthen hawkish comments though.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles