Asia week ahead: Japan’s GDP and central bank meetings

- 13 August 2020

- Asia week ahead

China, Indonesia and the Philippine central bank to meet next week, but all of them will take a pause. And Japan's moment of truth arrives with second-quarter GDP numbers too

Japan's second quarter GDP report card

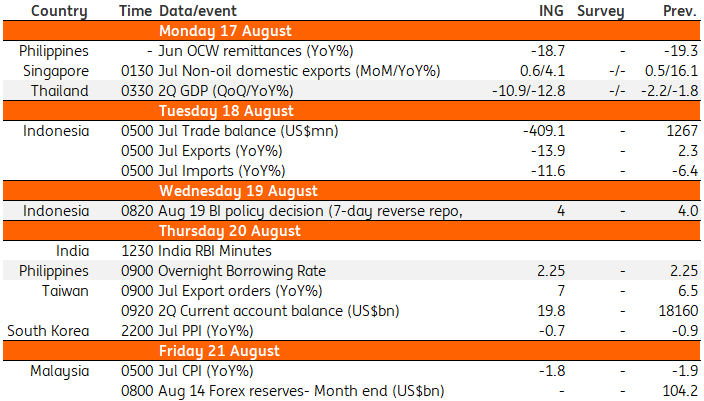

The data calendar for Japan is loaded next week, with the 2Q20 GDP release the main highlight.

2Q20 GDP is expected to contract by more than 20% (saar), much worse than the -2.2% recorded in 1Q. Japan trade data for July will also be released, and will also point to contraction as the global economy continues to run soft due to the pandemic.

Central bank meetings: Hitting the pause button for now

A couple of central banks will be meeting next week, but all of them are expected to take a pause.

The People's Bank of China will likely keep policy unchanged with monetary authorities actually tightening via open market operations for most of July and August.

Indonesia's central bank is scheduled to meet with Governor Warjiyo probably pausing after a recent rate cut to help provide some stability for the IDR.

The Philippine central bank is also widely expected to keep rates steady after Governor Diokno signalled no rate cuts to come in the next two quarters.

Inflation: Subdued as economic engines grind to a halt

CPI inflation will be released for Japan, Malaysia and Hong Kong with all likely to remain subdued as economic activity remains constrained by social distancing, labour market uncertainty and poor consumer sentiment.

Malaysia will likely report another month of negative inflation (July inflation at -1.8%) while Hong Kong and Japan inflation should remain below 1%

Rest of Asia: Thailand in recession, trade data still reflecting global slowdown

Thailand’s 2Q GDP should confirm a recession with the economy forecasted to contract by 12.8% after the -1.8% 1Q GDP report.

Trade data for the region rounds out data releases for the coming week and will likely reflect the ongoing weakness in the global economy. Indonesia’s exports may revert to negative territory after the surprise expansion in June while trade figures out from Japan and the Philippines should remain weak in year-on-year terms due to depressed global demand.

Asia Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 17 August 2020

- This bundle contains 4 Articles