Asia week ahead: China and India inflation, Taiwan and China trade

- 5 June

- Asia week ahead China India

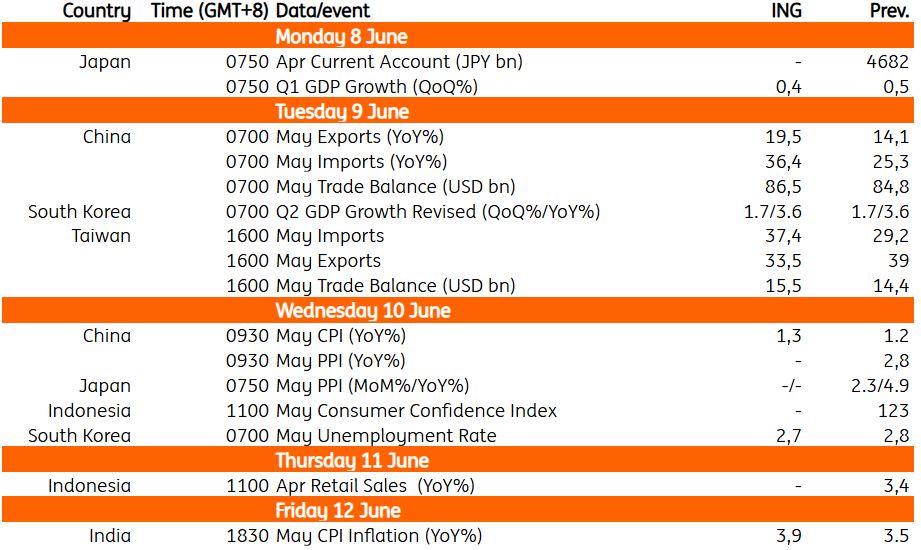

Inflation data from India and China are the highlights of the week. Other releases include trade figures from Taiwan and China

Asia Research highlights of the week

China’s mixed PMI data suggests economy is muddling through

Hotter-than-expected prices put South Korea on track for July rate hike

South Korea trade remains strong, but currency pressures persist

Stronger growth in Japan supports June rate hike despite softer inflation

India: Risks on inflation remain skewed to the upside

India’s CPI inflation is expected to pick up to 3.9% year-on-year in May from 3.48% in April, though it should remain below the Reserve Bank of India’s 4% target. Domestic gasoline prices rose by around 8% over the month. Yet the increase remains modest compared with fuel price trends elsewhere in Asia. The key risk to the outlook lies in potential second-round effects on food inflation. Fertiliser shortages, alongside the rising probability of an El Niño event, could exert upward pressure on food prices in the coming months and warrant close monitoring.

China: Higher tech prices continue to boost China trade

China’s May trade data, out Tuesday, are expected to show exports up 19.5% YoY and imports up 36.4%, for a trade surplus of $86.5bn. Both exports and imports have generally exceeded expectations so far this year. This is thanks in part to higher tech prices, which are boosting both export and import prices. China’s trade profile has increasingly tilted toward tech-related trade. China will also publish its inflation data on Wednesday. We expect the reflation trend to continue in May, with CPI inflation edging higher to 1.3% YoY.

Taiwan: Strong export data amid AI demand

Taiwan releases its May trade data on Tuesday. We’re looking for continued strong growth, with exports rising 33.5% YoY and imports rising 37.4%, resulting in a trade surplus of $15.5bn. Strong export orders from previous months suggest external demand remains robust amid the AI boom.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more