A bigger round of Dutch pension transitions puts curve steepening back in play

- 25 June

- Rates

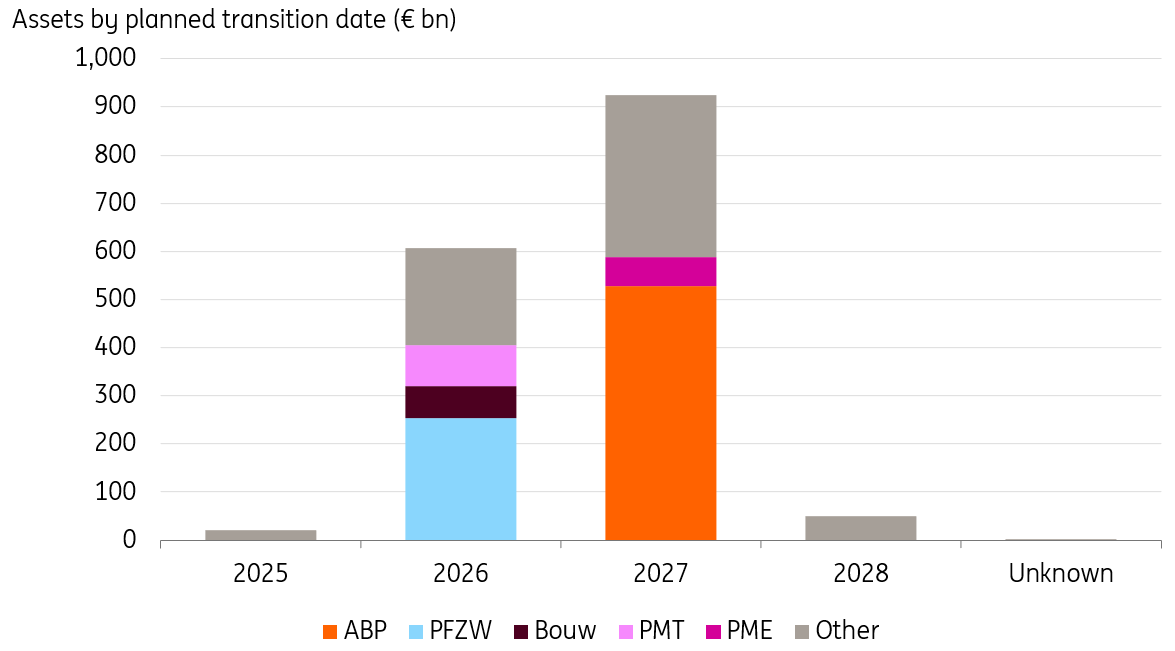

More than €900bn in Dutch pension assets are planning to transition in 2027, significantly more than the €600bn in 2026. Last year’s transition moved the 10s30s EUR swap curve by around 10-20 bp – and markets could start to feel similar pressure again in the months ahead

Markets digested the first batch well, but much more to come

More than €900bn of Dutch pension fund assets should transition in 2027, which could start making a mark on longer-dated rates in the coming months. The transition of €600bn assets in 2026 went remarkably well without triggering market turbulence. But reflecting on last year’s dynamics, we recognise that much of the market impact happened in 2H2025. As such, we think that, going forward, the 10s30s curve may see some 10-20bp of additional upward pressure over the coming months.

To recap, Dutch pension funds are in the midst of massive reforms that broadly aim to transform the system from defined benefits to defined contributions. Under the new framework, pension funds have greater flexibility to tailor portfolios by age cohort. As a result, we anticipate less need for longer-dated receiver swaps of 30Y and beyond. The demand for shorter swaps is likely to stay high or increase. For younger participants, pension funds are likely to allocate more to equities, but for older participants, the demand for fixed income should be stronger.

Significantly more pension assets are scheduled to transition in 2027

When we look at transaction data from the first quarter of the year, we see that bonds were still in high demand, especially when compared to equities. In 1Q26, Dutch pension funds bought around €19bn in debt securities, versus selling some €10bn in equities.

At first glance, this pattern suggests that the increased demand for fixed income for older cohorts exceeds the additional equities for younger participants. Unfortunately, we do not have a breakdown between those funds that have already transitioned and those that are still scheduled to.

Bonds still in high demand in the first quarter of 2026

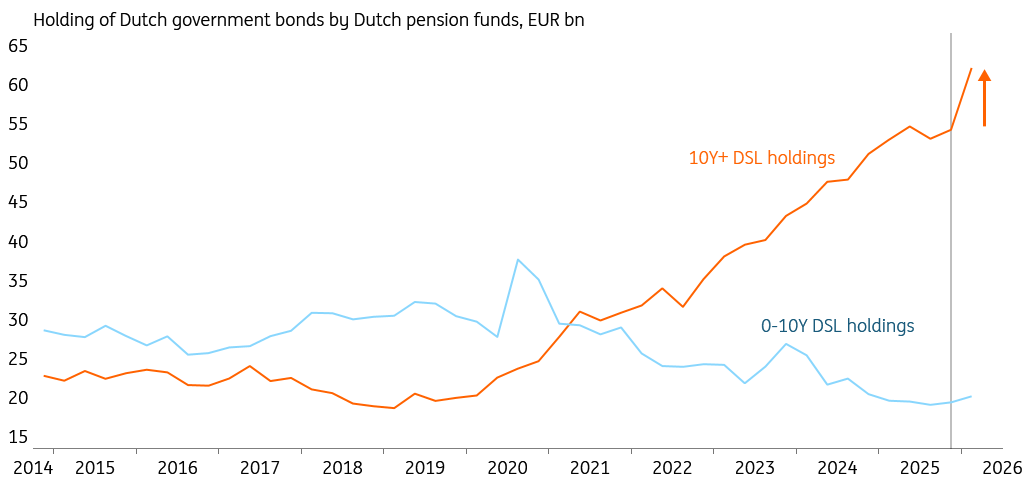

When looking at demand for Dutch government bonds (DSL) specifically, we see a remarkable pickup in 1Q26, reflecting a continuation of a strong home bias. The uptick is most evident in the 10Y+ maturity bucket of DSLs, which is not wholly unsurprising.

We previously estimated that the demand for duration with maturities of 10Y to 20Y will remain strong, if not stronger. In market pricing, we have seen the spread between DSLs and Bunds narrow further. A 10Y DSL trades at just 10bp above Bunds. Going by the healthy demand for DSLs from Dutch pension funds (and increasing issuance in Bunds) we could see this trend extended.

Strong demand for Dutch government bonds in 1Q26

We estimate a 10-20bp steeper EUR swap curve on the back of the reforms

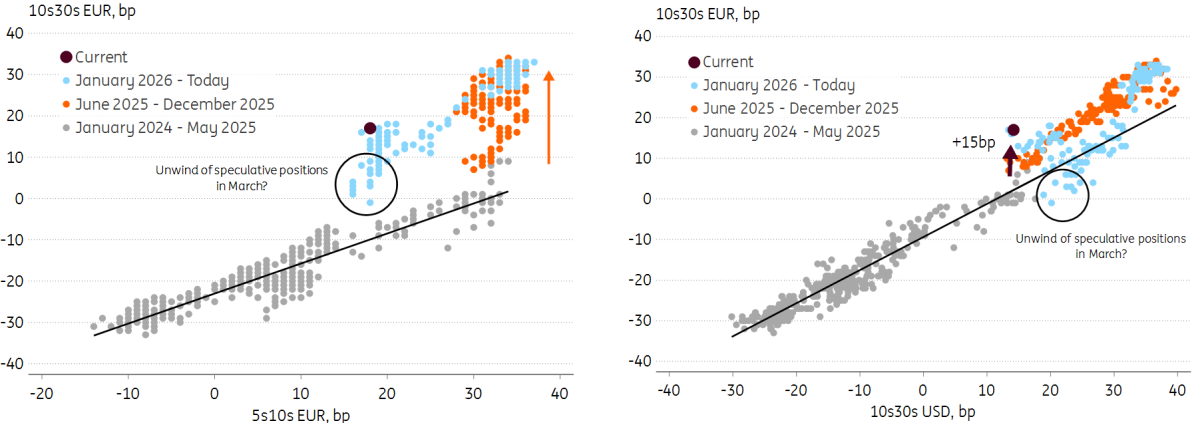

Whilst the market impact from the transition in 2026 may not be immediately obvious, we estimate the 10s30s steepened by an additional 10-20bp. The 10s30s EUR curve steepened significantly during the second half of 2025, much more than the dynamics of the 5s10s would have predicted (left chart). But at least part of this can be retraced to spillovers from the USD 10s30s curve (right chart), which steepened significantly over this period. Even after correcting for both, we still observe a level shift of around 10-20bp.

Also of interest is that the seemingly crowded 10s30s EUR steepener trade faced a painful shakeout in March 2026, resulting in a more aggressive flattening than would otherwise be expected. Nevertheless, markets seem to be stabilising again at a relatively steeper 10s30s than before.

With even more assets scheduled to transition in 2027, we think the curve could see similar steepener pressures as in the second half of 2025. Speculative flows might be more limited this time round, however, as the March sell-off suggested a crowded trade. Meanwhile, we do think many pension funds will likely start preparing for the transition date by already rebalancing their portfolios from longer to shorter maturities in the coming months.

EUR 10s30s curve still seems 10-20bp steeper when correcting for other factors

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more