US: September sales surge

US retail sales jumped 1.9% in September thanks to robust household finances. However, this strength is not sustainable given employment gains are plateauing and unemployment benefit incomes are being tapered. The uncertain outlook for Covid-19 continues to provide downside risk

Broad sector strength

US retail sales are incredibly strong, rising 1.9% month-on-month versus 0.8% consensus. Car sales (+3.6% MoM) were strong, which we already knew was going to be the case based on data from dealers. Instead the surprise was driven by the ex-autos component, which jumped 1.5% versus 0.4% consensus.

Strength was broad based with 12 out of 13 categories reporting a rise. That said, it does look as though back-to-school played a part with clothing rising 11% MoM and department stores seeing a 9.7% MoM gain. Normally you get a big boost to children clothing/school-related equipment sales in August as school returns, but that didn't happen because so many children are remote learning at home. Therefore, the typical decline in retail sales for these components didn’t happen this September. When combined with seasonal adjustments that would normally smooth this volatility, it appears to have dampened August’s figures and boosted September’s.

Nonetheless, we shouldn’t take too much away from what was a very good report, which saw sporting goods up 5.7%, health spending up 1.7% and eating/drinking out up 2.1%. There was also a sizeable 1.5% increase in gasoline station sales despite prices being flat on the month. This suggests there is more driving happening with the gradual return to more “normal” travel patterns continuing. The only parts of the report that could be described as soft were food sales at grocery stores, which were flat on the month and electronics reporting a 1.6% MoM fall.

Level of retail sales Feb 2020 = 100

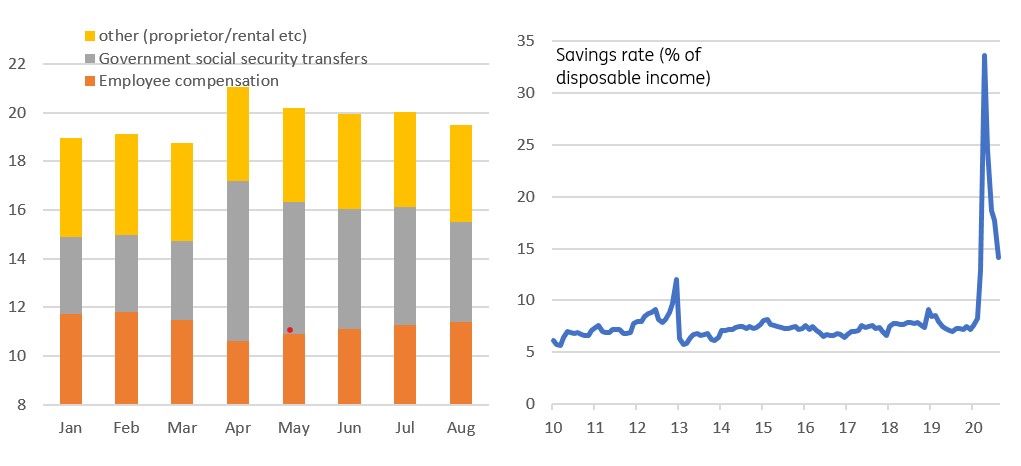

Robust household finances drive spending

The strength reflects the robust income gains that we have seen this year. The government’s response to the crisis was to boost the safety net for households by expanding unemployment benefits, which saw incomes rise sharply. The rise in government social security transfers – the $1,200 check and the additional $600/week Federal unemployment benefit – more than offset the fall in employment income from people losing their jobs. Consequently household finances are in great shape with the savings rate having surged and consumer credit data showing a significant shrinking in credit card balances. There is clearly momentum behind spending.

Personal income (USDtr) and the savings ratio

More challenges to come

That said, there will be more challenges for retailers as the employment picture seems to be softening. High frequency Homebase employment data is flat lining while yesterday’s weekly initial claims data moving up towards 900,000 underscores the strains that continue in the jobs market. This suggests we are likely to see only a limited rise in October payrolls with some forecasters foreseeing the possibility of an outright fall.

We also know unemployment benefits are being tapered and overall incomes are subsiding (see chart above). At least there is a savings buffer and we expect ongoing positive spending readings. However, these challenges and uncertainty about Covid-19, particularly the fear that European-style containment measures could eventually return to parts of the US, may mean fewer upside surprises in coming months.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap